If you own a portfolio of single-family homes (SFHs), demographic and economic trends are in your favor. SFHs comprise 16 million rental housing units in the U.S., according to Joe Bousquin of Builder. This represents a growth of 18% from 2008 to 2018, and accounts now for a third of all rental units nationally.

Source: WSJ

According to Ryan Dezember of the Wall Street Journal (subscription required), real estate investors are betting big on the idea that Americans are moving to more spacious suburb living. According to Dezember:

There haven’t been so many single-family homes under construction in the U.S. since 2007, yet many of these new houses won’t be for sale. Investors are building tens of thousands of houses expressly to rent in a bet that Americans will keep flocking to spacious suburban living even if they can’t afford to buy homes…and home prices have surged to records. The gains have outpaced wage growth, straining affordability despite historically low borrowing costs.

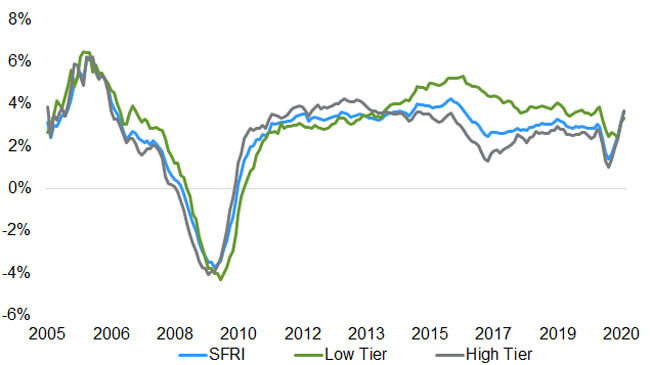

Rents for SFHs are also on the rise, according to CoreLogic:

Source: CoreLogic

Kathy Orton of The Washington Post last week reported that because of the pandemic, many renters are looking to leave multifamily buildings for more space in SFHs. Orton also reports on the prediction from Realtor.com that SFH starts will grow 9% in 2021. SFH starts were already up 11% compared to 2019, and the expectation is that this growth will be amplified in the suburbs and exurbs in medium-sized cities.

Contractor Magazine reported on some interesting SFH construction data, noting that “Pent-up demand during the shutdown, along with historically low interest rates, were the prime movers in the uptick in single-family homes.”

That said, many may be moving from renters to owners in the coming few years, with President-elect Biden’s plans to increase homeownership with incentives and tax credits.

The Real Deal ran a similar story last week, reporting that “High demand and low supply has driven house prices up, and ownership is unaffordable for average earners in 55 percent of U.S. counties, up from 43 percent a year earlier.”

Indeed, when viewing recent Federal Housing Finance Agency (FHFA) data, the recent annualized quarterly SFH price change has been staggering.

Source: FHFA

In addition to the above, Joe Bousquin of Builder reports that after dropping to $300,000 in 2019, the median sales price of a new SFH now sits around $340,000. Meeting the traditional 20% down payment requirements means families need $68,000 in liquid capital. This is why we are seeing a move more to rentals, and don’t expect this to change into 2021 as supply strains continue to characterize the SFH rental market.

According to Rodrigo Sermeño of Kiplinger, “with inventories still very low, house prices have risen steadily through the year as surging home demand has put upward pressure on home values.”

Big players entering SFH market (again)

It’s no wonder that the big players are entering the market. Institutional investors have been interested in SFHs since the great recession, and haven’t stopped piling up these assets. According to Bloomberg, as of September 2020, the SFH sector had seen $5.8 billion of commercial mortgage-backed securities, $2 billion more than in all of 2019. So why are big investors still bullish on SFHs? According to Bloomberg,

Data increasingly points to single-family rental’s maturation as an asset class, proving itself through tough times to be a stable, profitable, and expanding investment for some of the biggest pools of money in the world.

The biggest REITs in the space reported record-high occupancy rates throughout 2020, with Invitation Homes seeing 97.8%, in 2020 Q3, and American Homes 4 Rent at 97.2% occupancy in October 2020.

The new SFH push has driven up demand for expertise in the SFH market as well, as the Commercial Observer reports.

Conventional brokerages, such as JLL and Marcus & Millichap, have reacted to client demand and opportunity, and recently started navigating the SFR market, too….A confluence of trends was already supercharging single-family well before the pandemic drew in big investors: a housing shortage with no end in sight, a demographic wave of older millennials looking to settle down with more space, and dramatically improved technology and operations enabling easier management of often-scattered portfolios.

Patrick Clark of Bloomberg reported recently that the homebuilder Lennar Corp is making a big push into single-family rentals. Lennar is currently “laying the groundwork to develop thousands of rental houses, according to people with knowledge of the matter. The firm is seeking to raise $2 billion for the initiative, said one of the people, who asked not to be named because the matter is private.”

Matthew Rothstein of Bisnow reports that JLL is entering the fray, launching a division specifically for advising single-family rental investment. Unsurprisingly, “JLL’s move reflects the big business that owning single-family homes has become over the past few years. Single-family REITs outperformed REITs overall in 2020 by 23% and institutional owners control only about 3% of the market.”

Alex Nicoll and Daniel Geiger of Bloomberg report on these big institutional landlords, such as Blackstone who recently added $240 million to back SFH player Tricon Residential. Similarly, “institutional money including Nuveen, Brookfield, and JP Morgan, have invested more than $1 billion into the sector in 2020…[and] Invitation Homes hinting at a sale-leaseback program and many large operators partnering with home builders to build new rental homes.”

It’s worth concluding on the fact that retail investors (such as ourselves) still make up the biggest share of SFH rental owners. While the bigger players are focusing on primary markets and larger city centers, us retail folk have been pushing to smaller markets with lower acquisition costs and higher yields. Secondary and tertiary markets will see outweighed gains in the coming years, and it’s a good time for investors to begin exploring these relatively untapped markets.