Interest rates are rising, and many experts and industry organizations are predicting we are heading for higher rates long-term. Whether or not the experts are right, investors should be preparing themselves and their portfolios to withstand a rising interest rate environment.

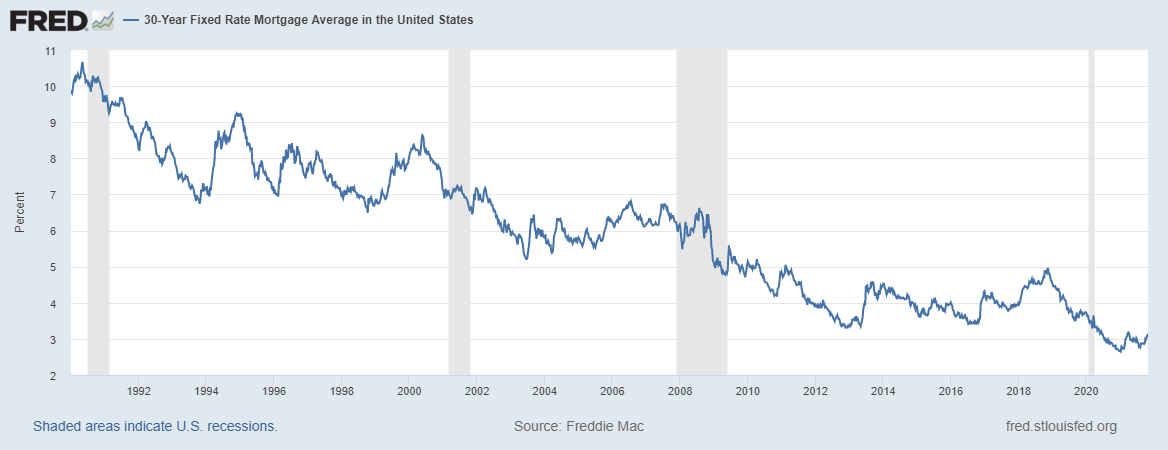

The good news for investors is that we are still sitting at historically low-interest rates, particularly at the 30-year benchmark rate.

Source: Freddie Mac. Primary Mortgage Market Survey, November 2021.

Let’s take a closer look at what interest rates are doing and how investors should position themselves as we are potentially entering a rising interest rate environment in the coming years.

What are interest rates doing?

In a recent survey of federal bank policymakers, half expect to begin raising interest rates in 2022 and believe that borrowing costs will jump at least 1% before the end of 2023. Similarly, due to inflationary pressures, Fannie Mae in its October Economic Outlook noted that mortgage interest rates will average at 3.3% throughout 2022. This is an increase from September’s projection for the same time period of 3.1%.

Doug Duncan, Fannie Mae Senior Vice President and Chief Economist commented on this new reality: “Combined with our expectation that inflation will run above-target over the forecast horizon, we foresee growing clamor from market participants for the Fed to begin tightening monetary policy: first by tapering asset purchases and then, in the fourth quarter of 2022, by raising the federal funds rate target range for the first time since December 2018.”

In its annual forecast, the Mortgage Bankers Association (MBA) believes that the 30-year benchmark fixed rate will finish this year at 3.1% before rising to 4% by the end of 2022. As such, MBA believes that mortgage originations will total $2.59 trillion next year, representing a 33% decline from 2021. In 2023, MBA believes originations will further decrease to $2.53 trillion.

It appears that most stakeholders are predicting some sort of rise in mortgage rates, meaning investors should take notice and prepare their portfolios.

Pro Tip: Check out current mortgage rates directly with Stessa (available only in eligible states)

Should I refinance? A checklist

The debt you put on your rental properties has a dramatic impact on the short and long term returns of your investments. A difference of just 1% can have a dramatic impact on your cash flow. For example, 3% on a $200,000 mortgage roughly puts monthly payments at $850. If you increase that to 4%, your payments will jump approximately $100 a month to $950. If you increase the loan amount, that payment number gets even bigger.

So mortgages rates matter, a lot. Here are a few key points to ask yourself as we head into a rising interest rate environment over the coming years.

Have I locked in low-interest rates for the long term? Locking in low-interest rates is likely the best option for investors in the current environment. That is, if the terms, fees, and potential penalties mean that long-term you will earn better returns with a lower interest rate. Be sure to add up all of these important downsides to breaking or re-negotiating your current loans to ensure you’re not creating unnecessary expenses that will render a lower interest rate a cost negative.

Have I explored fixed-rate products to lock in a lower interest rate for the long term? Fixed-rate mortgages are generally higher than variable, but they can offer long-term security as investors know exactly what their rate will be moving forward.

Are adjustable rates worthwhile as interest rates rise? Generally speaking, an adjustable rate mortgage (ARM) offers a fixed interest rate for a specific time, but then adjusts periodically over the term of the loan. As interest rates are predicted to rise, this could create a risk to your portfolio if interest rates increase in the future.

Can you shorten the mortgage term? As discussed, inflation has been predicted which erodes the value of your current and future cash holdings. Locking in a mortgage today, at today’s dollar value will mean that your future dollars will go further as you pay down your loans where the value was set back when inflation wasn’t as high. Considering shortening your mortgage term by putting more cash in today at today’s values could be considered as a hedge against future inflationary pressures.