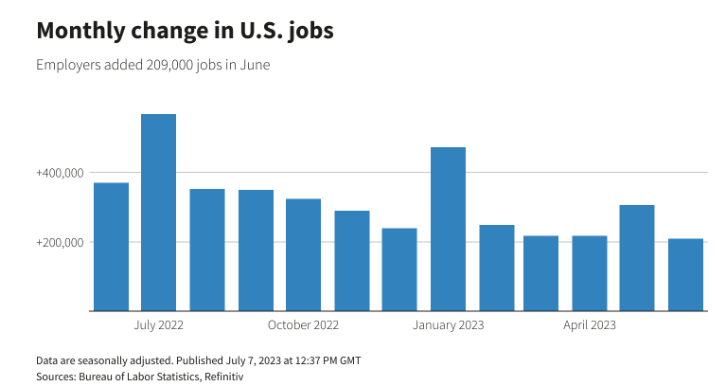

Lucia Mutikani of Reuters reports on the jobs data released last week showing that the U.S. added the fewest jobs in 2.5 years in June; however, wage growth points to a still-tight labor market. The unemployment rate fell to 3.6% from 3.7% in May, and hourly earnings increased 0.4%, up 4.4% year-on-year. Mutikani notes that this will “most certainly ensure the Federal Reserve will resume raising interest rates later this month.”

Source: Reuters (July 2023)

Sarah Marx of Housing Wire (subscription required) comments on the data, highlighting that although economic conditions are moderating, it’s not enough for the Fed, who will likely raise rates at the next meeting. Although wage and job growth are slowing, it is not fast enough for the Fed’s 2% inflation target. Marx quotes Lisa Sturtevant, chief economist at Bright MLS:

“The Federal Reserve has raised interest rates 10 times and it is possible that we are finally seeing the intended slowdown in the economy… Today’s employment report does not provide a clear indication as to what the Federal Reserve will do at its next meeting but the expectation is still for a rate increase when the Federal Open Market Committee convenes again. The modest slowdown in the labor market could give the Fed renewed confidence in its ability to bring the economy in for a soft landing.”

Orphe Divounguy of Zillow reports that this data shows the U.S. economy is still on solid ground. This is a double-edged sword as a strong economy means home buying activity will be more robust, but higher interest rates will put downward pressure on sales volume and home prices. Despite the latter, we saw an increase in construction employment, reflecting higher builder sentiment, particularly in residential. More supply could help alleviate the price pressures coming from higher rates, Divounguy notes.

Christopher Rugaber of Fortune jumps into the conversation on jobs data, highlighting that the slower growth seen in the latest data could indicate a more sustained growth. This means that a ‘soft landing’ regarding a recession is more likely now than ever.

Highest rates in 2023

Given the strong jobs report, Matthew Graham of Mortgage News Daily reports that there’s little hope for lower rates throughout 2023. Strong economic data puts upward pressure on interest rates, and the recent jobs report, business activity data, and jobless claims all point to a still robust economic picture.

Filip De Mott of Markets Insider reports a similar sentiment, noting that although Freddie Mac showed a 6.81% average, another index showed 7.22%. Increasing mortgage rates have overturned a streak of strong lending demand, which decreased by 5% last week.

Indeed, according to Freddie Mac, the 30-year fixed rate now sits at 6.81%, the highlight level seen in 2023 and a significant jump from 6.71% the week early.

Source: Freddie Mac (July 2023)

Margaret Heidenry of Realtor.com reports on the high rates, commenting, “[a]s if record-high mortgage rates weren’t enough bad news, in another housing gut punch, the number of homes for sale dipped below last year’s level by 2% for the week ending July 1. That’s the first significant drop in inventory in over a year, at 60 weeks. Sellers’ reluctance to list is directly tied to today’s high rates, with 1 in 7 homeowners choosing not to sell this year because they feel “locked in” to their current lower interest rate loan.”

Melissa Dittmann Tracey of the National Association of Realtors (NAR) jumps in, reporting that the average loan size for a home purchase dropped to $423,500 in June, its lowest level since January. This may highlight that buyers are adjusting to the new interest rate normal.

Debt maturities

As interest rates remain elevated, those who have debt maturing that will require some form of renewal will start feeling more pain. According to Ashley Fahey of Business Journal (subscription required), a new Morgan Stanley report shows that about $1.5 trillion in commercial real estate debt is maturing by the end of 2025. The real estate markets with the most commercial debt maturity risk are as follows:

Source: Business Journal (July 2023)

The sectors that are the most at risk, according to Fahey, include:

“Retail and hospitality assets continue to see the highest delinquency rates among properties carrying CMBS debt, with retail properties at 6.48% and lodging at 5.35% in June, Trepp found. But the gap between those delinquency rates and the office delinquency rate is quickly narrowing.”

Jennifer Sor of Markets Insider reports on a Capital Economics report showing the cities most vulnerable to the forthcoming commercial real estate pain. These include San Francisco, Chicago, New York City, Los Angeles, Boston, and Washington, DC, with the Bay Area expected to decline the most. The report highlights that San Francisco commercial property values dropped 40%-45% from 2023-2025.

Jack LaForge of Trepp comments on commercial debt maturity, highlighting that the sectors with the most commercial loans maturing for the remainder of 2023 are hotels, offices, and industrial. We may see more “extend and pretend” type strategies as these loans come up for maturity, as owners will take on more expensive short-term debt in the hopes that over the coming years, rates will moderate more before locking in longer-term debt.

“For property types like multifamily, industrial, and student housing, there may be more buyers’ regret than distress. For other property types, the dire narrative is much more accurate. The story could get worse for shopping malls and central business district’s (CBD) hotels before it gets better. For office, the predictions of higher defaults and big losses are probably spot on.”

Because of the rising interest rate environment, government regulators have even stepped in, asking banks to work more closely with borrowers, according to Reuters. Specifically to commercial real estate lenders, the regulators are asking them “to work with credit-worthy borrowers that are facing stress in the commercial real estate market. Financial institutions should work “prudently and constructively” with good borrowers during times of financial stress,” the agencies said in a statement.