Jonathan Delozier of HousingWire reports that the Housing for the 21st Century Act is a sweeping federal reform aimed at tackling the nation’s roughly 5 million–home shortage by pushing states and localities to loosen zoning barriers, including allowing duplexes and triplexes in single-family zones, legalizing ADUs, eliminating parking minimums, reducing lot sizes and streamlining permits, while also raising FHA loan limits, reforming manufactured housing policy and expanding HOME program eligibility. With first-time buyers now entering the market at a median age of 40 and 85% of voters still viewing homeownership as part of the American Dream, the bill directs HUD to issue best-practice guidance and offers technical support and pilot grants to states that adopt supply-boosting reforms

Emma Waters of the Bipartisan Policy Center explains that the Housing for the 21st Century Act represents the first comprehensive bipartisan housing markup in nearly a decade, clearing the House Financial Services Committee 50–1 on December 17, 2025, before passing the full House 390–9 on February 9, 2026. The package weaves together elements from at least 43 separate housing bills (27 with bipartisan sponsorship) spanning regulatory streamlining, modernization of existing federal housing programs, expanded affordable housing finance tools, and stronger oversight of housing providers.

Michael Rauber of the National Association of Realtors (NAR) highlights the unusually broad political coalition behind the Housing for the 21st Century Act, led by House Financial Services Chair French Hill and Ranking Member Maxine Waters alongside Subcommittee leaders Mike Flood and Emanuel Cleaver, with the bill clearing committee 50–1 before passing the full House 390–9. The legislation reflects heavy industry engagement, including advocacy from the NAR, which issued a targeted call to action and formal letters to House leadership urging support. Framed as a generational wealth and credit-access issue as much as a supply challenge, the bill now shifts to the Senate, where continued bipartisan coordination will determine whether this rare cross-party housing push ultimately reaches the President’s desk.

“The National Association of REALTORS® applauds the House for passing the Housing for the 21st Century Act, a meaningful and bipartisan step toward addressing America’s housing affordability crisis. With the nation facing a shortage of roughly 5 million homes and first-time buyers now entering the market at a median age of 40, bold action to expand supply and remove barriers to homeownership has never been more urgent,”

Tristan Navera of Realtor.com reports that the 199-page Housing for the 21st Century Act, comprising roughly two dozen provisions, is advancing under a potential suspension-of-the-rules vote, a fast-track procedure that limits debate, bars amendments, and requires a two-thirds majority, underscoring leadership’s push to move quickly amid widespread housing pessimism. Beyond supply themes, the bill expands financing channels for manufactured, affordable, and multifamily housing, reforms housing counseling and financial literacy programs, mandates deeper reporting on the barriers faced by elderly and disabled Americans, and increases oversight of HUD and public housing agencies.

Inflation and jobs data

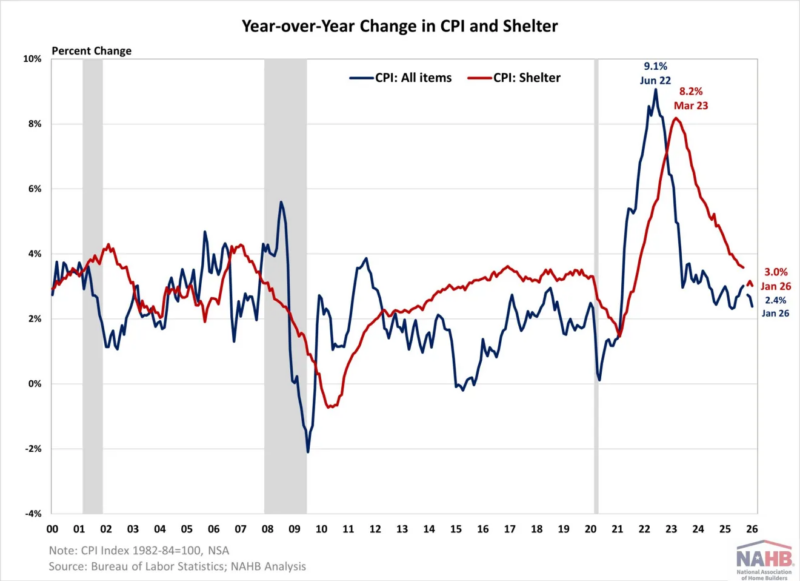

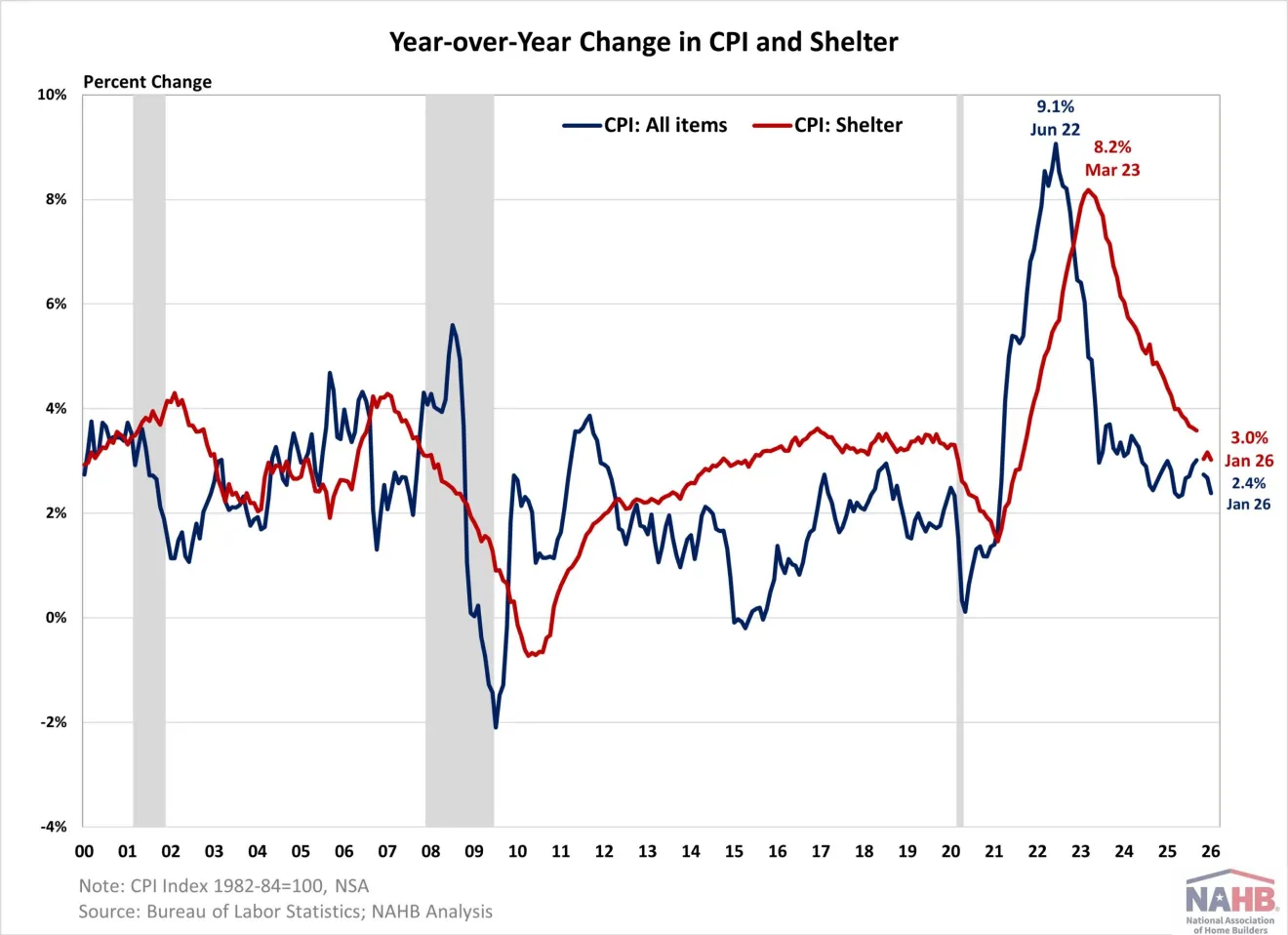

Fan-Yu Kuo of the National Association of Homebuilders (NAHB) reports that inflation cooled to an eight-month low in January, with headline CPI rising 2.4% year over year, the slowest pace since May 2025, while core CPI edged up 2.5%. The housing shelter index, a major driver of core inflation, increased 3.0% annually and is expected to show larger gains through April due to measurement effects, even as broader price pressures ease.

Source: NAHB (February 2026)

Food prices rose 2.9% and energy dipped 0.1%, but underlying cost pressures remain, as the average U.S. tariff rate climbed from 2.6% to 13% in 2025, and a New York Fed study found 94% of tariff costs were passed through to businesses and consumers, keeping household goods prices elevated despite moderating inflation.

Jake Krimmel of Realtor.com reports that January’s CPI came in broadly in line with expectations, marking core inflation’s lowest level since March 2021 and reinforcing a gradual disinflation trend, particularly with shelter rising just 0.2% month over month. The data strengthens the case for the Federal Reserve to hold steady at its March meeting, as inflation cools and the labor market remains stable, with markets still pricing in two potential rate cuts later this year. For housing, steady mortgage rates around 6.1% and improving real income growth offer a constructive backdrop heading into spring, but soft existing-home sales and lingering affordability fatigue suggest that a durable rebound will depend on several more months of stable prices and labor-market certainty.

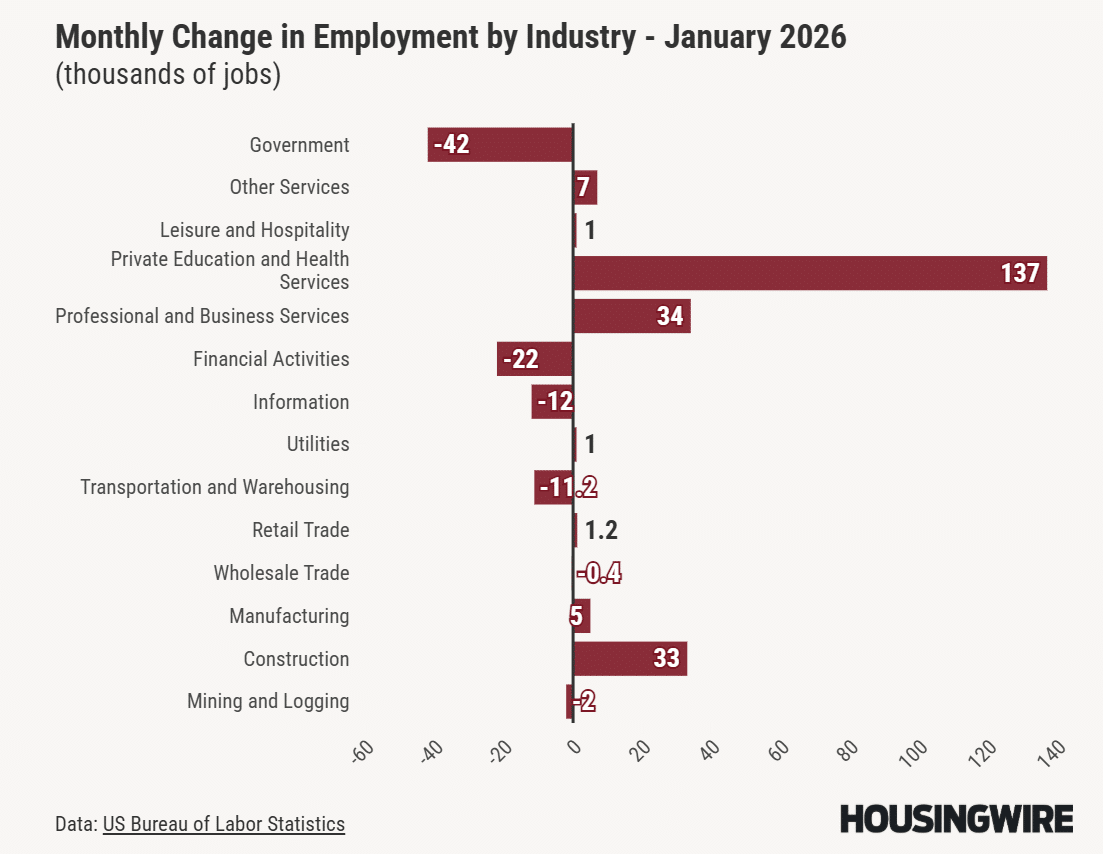

Logan Mohtashami of HousingWire reports that January added 130,000 jobs (beating estimates and keeping unemployment at 4.3%), but the headline strength looks different after revisions showed only 181,000 total jobs were created in all of 2025. Gains were concentrated in healthcare and social assistance, masking ongoing weakness elsewhere, particularly in residential construction employment, which remains in a negative trend. Bond yields initially jumped, with the 10-year rising before easing later in the day, leaving mortgage rates largely unchanged at roughly 6.14%, underscoring how even a “strong” jobs print hasn’t been enough to materially shift rate expectations.

Source: HousingWire (February 2026)

Orphe Divounguy of Zillow notes that while January added jobs, major benchmark revisions reveal 2025 job growth was far weaker than first reported. There was a cut from 584,000 to just 181,000, with payroll levels revised down by 898,000, while wage growth cooled to 3.7% year over year. For housing, that softer labor-market backdrop tempers optimism: although Zillow expects modest gains in 2026 as affordability improves and incomes outpace price and rent growth, weaker job momentum and declining confidence could suppress mobility, especially among first-time and payment-sensitive buyers.

Home sales

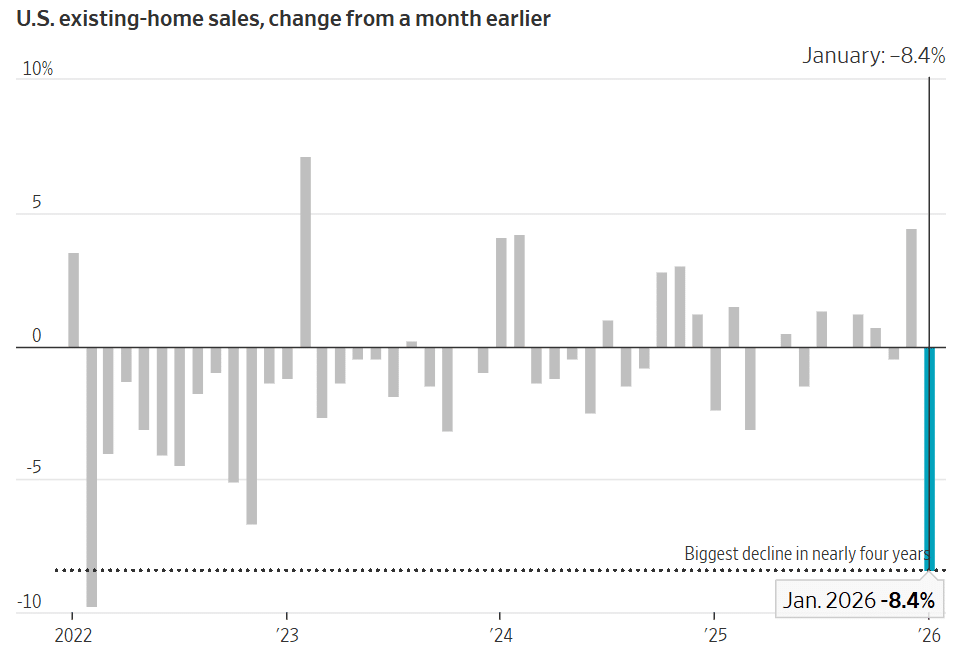

Nicole Friedman of the Wall Street Journal reports that U.S. existing-home sales fell 8.4% in January (the steepest monthly drop since February 2022) to a seasonally adjusted annual rate of 3.91 million, reversing momentum that had begun to build in recent months. Freezing temperatures, snowstorms, and still-elevated home prices, combined with weak consumer confidence, undercut activity and highlight how fragile the housing recovery remains despite earlier signs of stabilization.

Source: WSJ (February 2026)

Orphe Divounguy of Zillow reports that January existing-home sales fell 4.4% from a year earlier, even as inventory rose 3.4% annually to 1.22 million homes and the median price held nearly flat at $396,800 (+0.9%). The slowdown reflects late-2025 contracts signed amid a weakening labor backdrop and sharp downward revisions to job numbers, despite mortgage rates trending lower and incomes outpacing housing costs last year. Zillow expects only a modest rebound in 2026 to 4.2 million sales, with prices projected to rise 7.7%, pushing total transaction value above $2 trillion (up 10.9%) with roughly two-thirds of that gain driven by higher prices rather than stronger sales volume.

Lawrence Yun, NAR Chief Economist, comments:

“The decrease in sales is disappointing. The below-normal temperatures and above-normal precipitation this January make it harder than usual to assess the underlying driver of the decrease and determine if this month’s numbers are an aberration…Affordability conditions are improving, with NAR’s Housing Affordability Index showing that housing is the most affordable it’s been since March 2022. This is due to wage gains outpacing home price growth and mortgage rates being lower than a year ago. However, supply has not kept pace and remains quite low.”

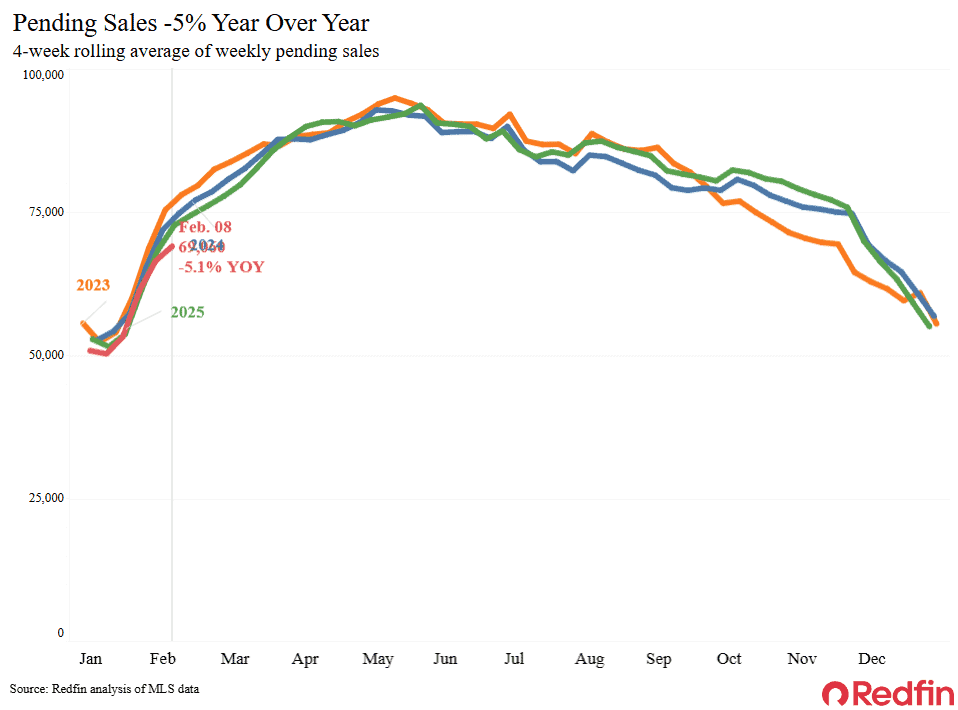

Dana Anderson of Redfin reports that the housing market is tilting further toward buyers, with pending home sales down 5.1% year over year and declines in 45 of the 50 largest U.S. metros, the broadest pullback in over two years. Inventory dynamics are shifting as homes now take a median 66 days to go under contract, the longest span in seven years, and supply has climbed to 5.5 months, signaling the strongest buyer leverage since 2019. While new listings dipped 1.8% and total inventory slipped about 1% (the first drop since 2023), there are still far more sellers than buyers, allowing some purchasers to negotiate below the asking price.

Source: Redfin (February 2026)

Diana Olick of CNBC reports that January existing-home sales fell wider than expected, even as the median price hit a record $396,800, up 0.9% year over year. Inventory stood at 1.22 million homes, a 3.7-month supply (still well below the six months considered balanced), helping keep prices firm despite weaker demand. Homes took 46 days to sell, up from 41 a year ago, and activity remained skewed toward the high end, with $1 million-plus properties the only segment posting annual gains, while sub-$250,000 sales fell the most. Experts note that while affordability metrics have improved and homeowners have gained roughly $130,500 in housing wealth since 2020, limited supply and stalled mobility are leaving many Americans effectively stuck.