Diana Olick of CNBC noted that the 30-year fixed hit 6.53% on March 20, just 18 basis points shy of year-ago levels. Active inventory rose 5.6% year-over-year for the week ending March 14, with Las Vegas, Seattle, Cincinnati, and DC all up more than 20% YoY. Price growth slowed to near 0% in January, and 69% of leading metro markets are considered overvalued. New home inventory sat at 9.7 months in January.

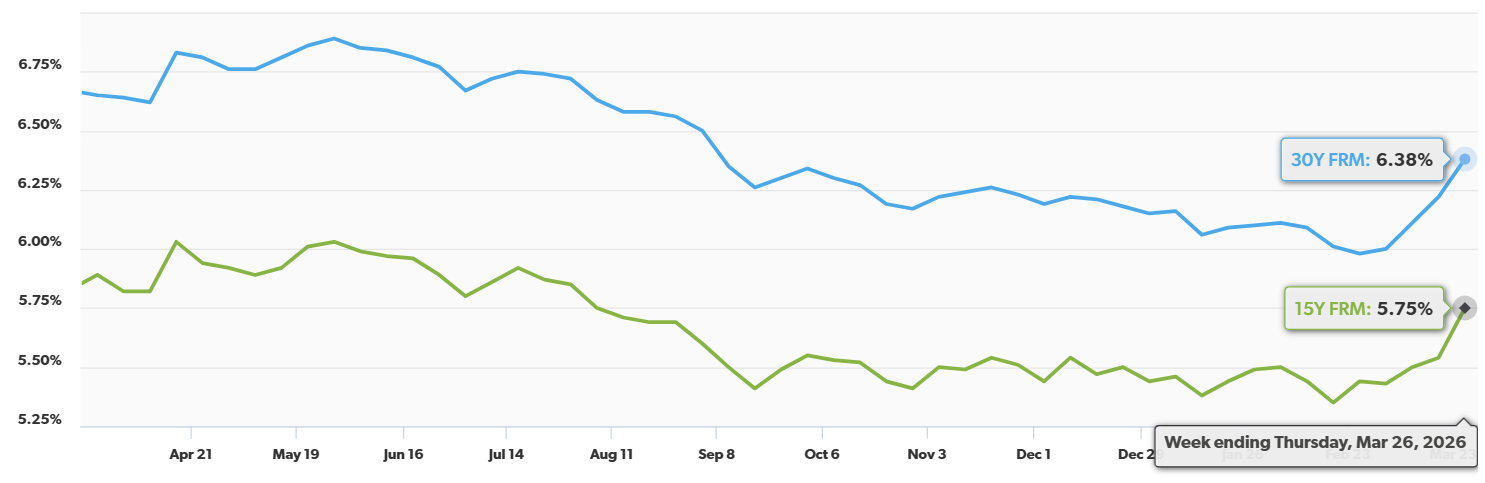

Source: Freddie Mac (April 2026)

Wolf Richter of Wolf Street reported that the average weekly 30-year fixed mortgage rate rose to 6.43%, the highest since October 2025. Purchase mortgage applications are down 35% from the same period in 2019, and annual home resales have plunged 23% from 2019 levels for each of the past three years. Supply of resale single-family homes surged to its highest in nine years, while inventories of new completed single-family homes reached their highest since 2009.

Joy Dumandan of Realtor.com found that mortgage applications decreased 10.5% for the week ending March 20, the second straight weekly decline. The Purchase Index fell 5%, and the Refinance Index dropped 15%, with the 30-year fixed more than 30 basis points higher than at the end of February. ARM share increased to 8.1% of applications as borrowers sought lower payments.

Daniel Banta of Scotsman Guide highlighted that the national median mortgage payment was $2,061 in February, down from the record $2,070 in January and $144 lower than a year ago. However, rising rates (the 30-year fixed averaged 6.38% for the 7-day period ending in late March, a gain of 27 bps over two weeks) triggered the sharp 10.5% drop in application volumes. The MBA Purchase Applications Payment Index (PAPI) fell to 150 from 166.2 a year ago.

Andrea Riquier of USA Today observed that rates are expected to remain elevated as long as hostilities in Iran continue. Adjustable-rate mortgages are gaining traction; ARMs account for 31% of originations in California and 8.1% of applications nationwide, as buyers seek to lower monthly payments while awaiting rate relief.

Edward Seiler, The Mortgage Banker Association’s (MBA) Associate Vice President of Housing Economics, comments:

“Homebuyer affordability saw a modest improvement in February, as slightly lower mortgage rates helped ease monthly payment burdens despite a small uptick in loan sizes. The February PAPI declined over the month and is nearly 10 percent lower than a year ago, reflecting both reduced payments and steady income growth…While affordability conditions remain challenging in many markets, these incremental gains — felt across more than half of states — are an encouraging sign for prospective buyers, particularly those seeking lower-payment options. Unfortunately, this month’s turmoil in the Middle East has put upward pressure on mortgage rates, which in turn could impact overall affordability in the months ahead.”

Market cooling

Cotality released a report showing that 78% of home purchases closed below asking price in February 2026, up 3 percentage points from a year earlier and nearly double the 44% seen in February 2022. Months of supply reached 4.5 nationally. In Florida, over 90% of homes sold below asking, and in Texas, 88%. January price growth was just 0.7%, with 34% of the 100 largest markets showing yearly price declines.

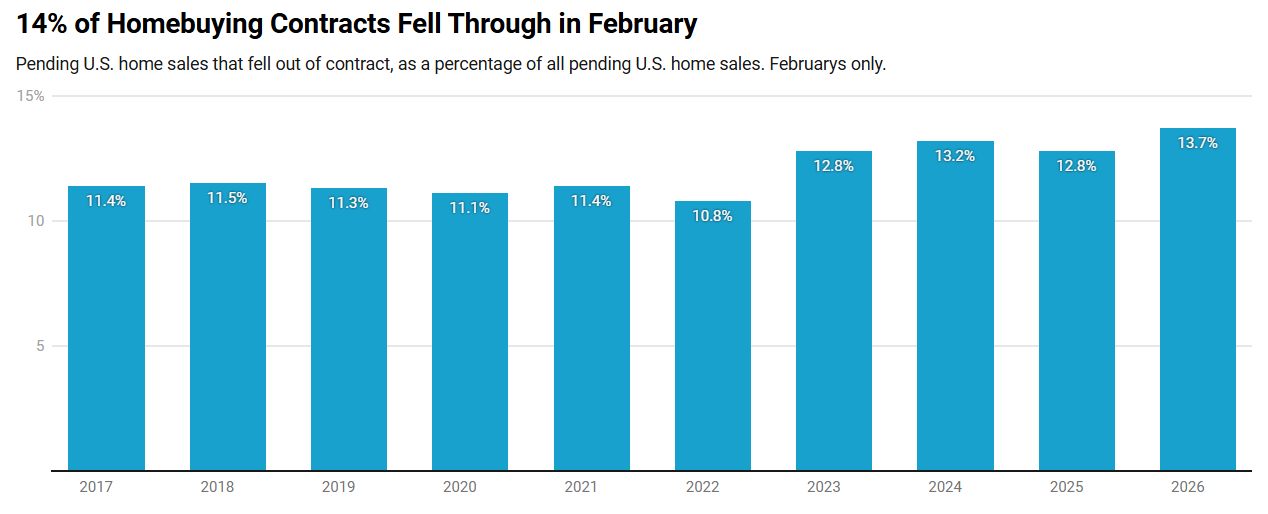

Dana Anderson of Redfin reports that roughly 42,000 U.S. home-sale agreements fell through in February 2026, pushing the cancellation rate to 13.7% of all pending sales, the highest February figure since Redfin began tracking in 2017 and up from 12.8% a year earlier. The driving force is a historic buyer-seller imbalance: with hundreds of thousands more sellers than buyers nationwide (a near-record gap), house hunters feel comfortable walking away from offers over inspection issues, price concerns, or simply finding something better. Markets like Tampa and San Antonio are feeling it most acutely, where sellers outnumber buyers by roughly two to one. In short, nearly one in seven deals is dying on the vine because today’s buyers know they have options and aren’t afraid to use them.

Source: Redfin (April 2026)

Diana Olick of CNBC wrote that sellers are increasingly inclined to reduce asking prices as homes take longer to sell. Active inventory rose 5.6% year-over-year, with major metros like Las Vegas, Seattle, Cincinnati, and DC each up more than 20%. New home inventory reached 9.7 months in January. The Northeast and Midwest are seeing the strongest remaining price appreciation.

Lance Lambert of ResiClub reports that national active listings rose 7.9% year-over-year from February 2025 to February 2026, reaching 914,860 homes, still 17% below February 2019 levels. Nine states (AZ, CO, FL, ID, NE, TN, TX, UT, WA) are now at or above pre-pandemic inventory levels, while the Midwest and Northeast remain tight. Florida inventory edged slightly lower year over year despite overall national gains.

Rachel Bader of HousingWire highlights that regional housing demand is proving surprisingly durable even as mortgage rates creep toward 6.64%. Weekly pending sales nationally hit 71,230 (up from 68,726 a year ago), with Texas leading the charge at 8,223 new pendings, including 2,227 in Dallas-Fort Worth and 2,025 in Houston. California is holding its own, too, with just 26.5% of listings seeing price cuts, well below national norms, while Midwest affordability is keeping Chicago (1,525 new pendings, up 2.3% week over week) and Detroit (994 pendings) humming along. Purchase applications still show 12% year-over-year growth, and nationally, only 33.8% of listings have been reduced, nearly identical to this time last year.

Commercial real estate

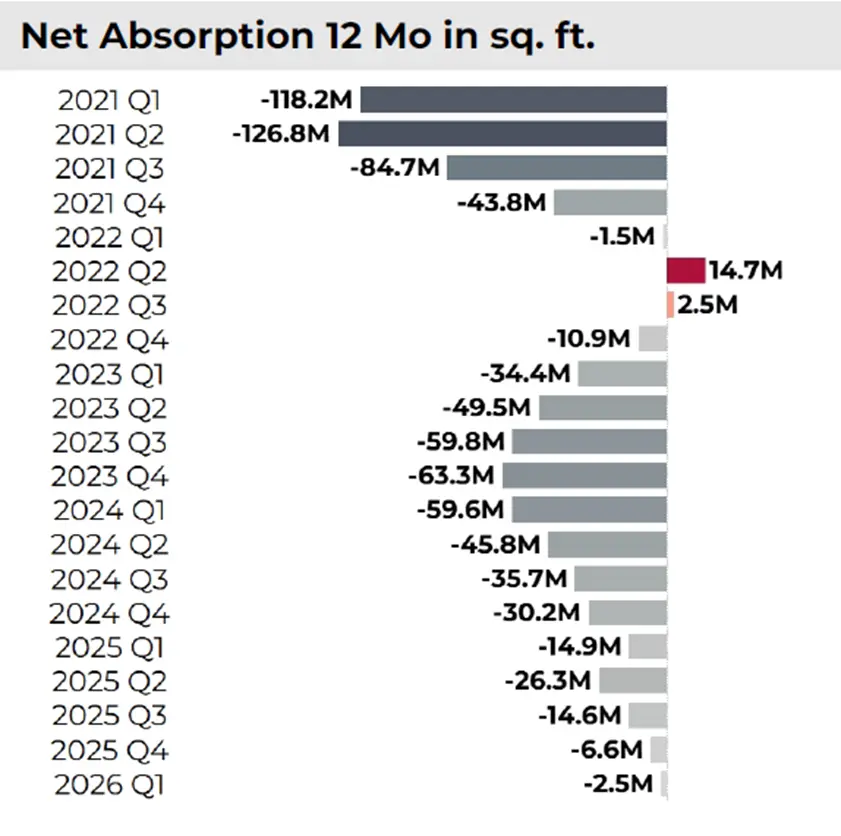

Erik Sherman of GlobeSt reported that national office vacancy averaged 17.6% in February 2026, a 2-percentage-point improvement from a year earlier. Only 28 million square feet remains under construction (an unusually slim pipeline) as demolitions and conversions shrink total supply. High-vacancy markets include Seattle, Austin, and San Francisco (above 24%), while Miami leads with just 12.8% vacancy, and Manhattan is close behind.

The National Association of Realtors’ (NAR) March 2026 Commercial Real Estate Market Insights report paints a picture of an economy losing steam, with February job numbers declining month over month, inflation holding at 2.4% (still driven largely by shelter costs), and the Fed sitting on its hands after late-2025 rate cuts while long-term yields stay stubbornly above 4%. On the commercial real estate side, the office market tells a nuanced story of slow stabilization: Class A space is attracting the most leasing activity but paradoxically carries the highest vacancy, Class B is seeing softer demand but holds healthier fundamentals overall, and Class C keeps bleeding tenants despite maintaining the tightest vacancy rates and relatively stronger rent performance.

Source: NAR (April 2026)

The broader signal is that easing rent trends could eventually take pressure off the shelter component of inflation, but for now, tight financial conditions and fading economic momentum from Q4 2025 are keeping the commercial sector in a holding pattern rather than a recovery.

“Retail remains the tightest sector in commercial real estate. Demand remains slightly negative and new supply is adding modest pressure, but vacancy rates are still relatively low, At the same time, rent growth continues to outperform other property types, helping maintain pricing power. General retail stands out as the most resilient segment, with the lowest vacancy, while neighborhood centers and malls face weaker demand despite selective rent strength in certain formats.”

Falen Taylor of MBA reports that total commercial mortgage origination volume will increase 27% to $805.5 billion in 2026, up from $633.7 billion in 2025; the most loan production since 2022’s record $815.6 billion. Multifamily originations are expected to rise 21% to $399.2 billion. Approximately 17% ($875 billion) of the $5 trillion in outstanding commercial mortgages are scheduled to mature in 2026, and the 10-year Treasury yield is expected to average 4.2% for the year.

“The U.S. economy continues to grow, but unevenly. The job market is softening, driven primarily by a slowdown in hiring, while the pace of layoffs is beginning to pick up. Inflation is likely to rise further, at least in part due to the pass-through of tariffs to consumers,” said Fratantoni. “MBA forecasts that GDP grew 2.3 percent in 2025, but will slow in the next two years, with growth projections of 1.9 percent this year and 1.7 percent in 2027. The unemployment rate will average 4.5 percent in 2026, up from 4.3 percent in 2025.”

Finally, Mark Heschmeyer of CoStar reports that commercial and multifamily mortgage originations surged 30% year over year in Q4, with office property loans leading the way at a striking 95% increase in loan volume over the same period, signaling that lenders are regaining confidence in the commercial real estate recovery heading into 2026.