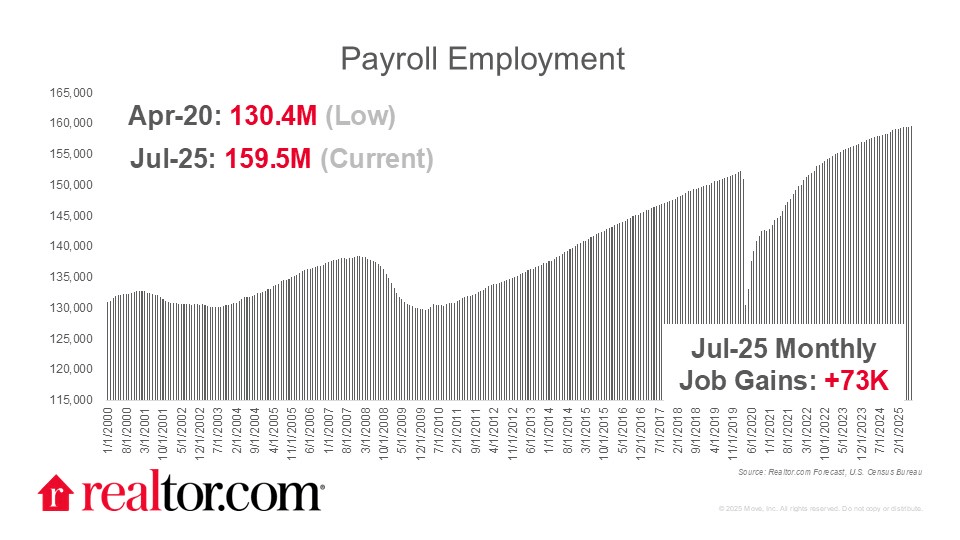

Danielle Hale of Realtor.com reports on the July jobs data showing a moderating labor market, with payrolls up a net 73,000 and unemployment edging to 4.2% (after the prior month was revised sharply lower, making today’s figure a modest increase). Health care and social assistance led gains while government payrolls fell. Fed Chair Powell’s point holds: slower labor demand has been met by slower labor supply, keeping conditions relatively balanced. Earnings also rose 3.9%, slightly above recent readings.

Source: Realtor.com (August 2025)

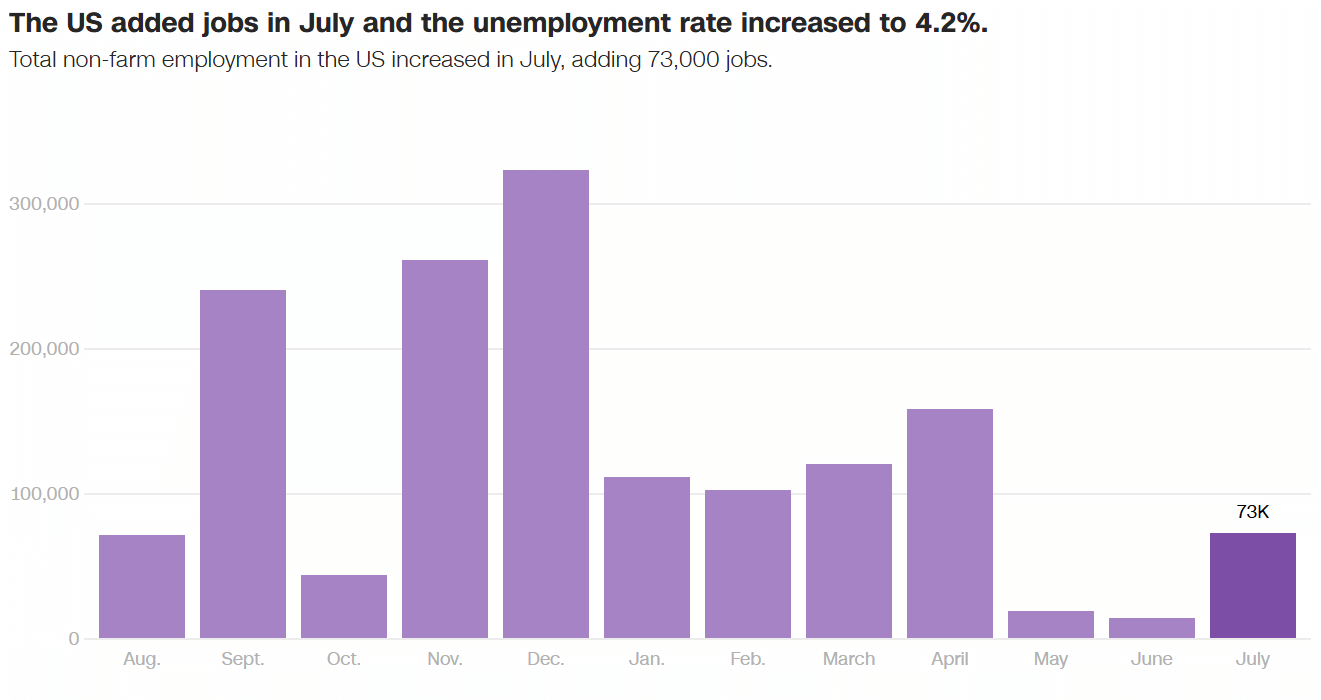

Alicia Wallace of CNN reports on the same data, highlighting that the added jobs were far below the expected 115,000, with prior months’ totals revised down by a combined 258,000, the weakest monthly performance since December 2020. Economists called the downward revisions “stunning,” with KPMG’s Diane Swonk warning the labor market is “stalling out” and RSM’s Joe Brusuelas labeling it “the worst major economic report since the end of the pandemic era.” The pace of job creation this year is now the weakest in decades outside of recessions.

Source: CNN (August 2025)

Ben Casselman and Tony Romm of the New York Times report that President Trump fired Erika McEntarfer, the Senate-confirmed commissioner of the Bureau of Labor Statistics, claiming that July’s weaker-than-expected jobs report and large downward revisions to prior months’ hiring data were “rigged.” McEntarfer, appointed in 2023 by President Biden, was replaced by deputy commissioner William Wiatrowski. Economists warned the move could undermine trust in government economic data.

The Mortgage Bankers Association’s (MBA) Deputy Chief Economist Joel Kan reacted to the report on employment conditions in July:

“This morning’s release showed significant labor market weakening over the past three months, as indicated by job growth down to a gain of 73,000 jobs in July and significant downward revisions to the totals for May and June. Notably, goods-producing industries saw contraction for the third straight month. Service industries involved in trade also saw declines in job growth, potentially a result of the uncertain tariff environment, as businesses either put their activity on pause or pulled back altogether. The downward revisions were larger than usual, totaling 258,000 fewer jobs estimated for the prior two months, which dropped the year-to-date average to 85,000 jobs, around half of the monthly average in 2024.”

September cut?

Markets now place the likelihood of a September rate cut at 90%, according to CME FedWatch. Logan Mohtashami of HousingWire reports that July’s weak data sparked a major bond market rally, pushing the 10-year yield down to 4.26% and signaling lower mortgage rates ahead. The report increases pressure on Fed Chair Jerome Powell, who has maintained a restrictive stance despite earlier warnings about labor market softness, and could put a 0.50% rate cut on the table for September.

Flávia Furlan Nunes, also of HousingWire, reports that while a rate cut in September is widely anticipated, mortgage industry professionals doubt it will meaningfully boost the housing market. Loan officers advise borrowers to proceed with applications, as sellers and builders are already offering concessions to lower effective rates, and lenders are providing flexible rate locks. The Fed kept its benchmark rate at 4.25%–4.5% last week, with Chair Jerome Powell noting that maximum employment has been reached and inflation is easing, though higher tariffs are pushing up prices for certain goods.

Eleanor Pringle of Fortune reports that July’s sharply weaker jobs data has fueled investor expectations of an interest rate cut at the Fed’s September meeting. The three-month average job gain has fallen to just 35,000, signaling a softer labor market than previously believed and strengthening the case for monetary easing. The resignation of FOMC member Adriana Kugler also paves the way for a potentially more dovish Fed stance, aligning with White House pressure for lower rates.

Further, Sarah Qureshi of Reuters reports that gold prices climbed for a third consecutive session, with spot gold up 0.3% to $3,372.15 per ounce and U.S. futures up 0.8% to $3,426.40, the highest since July 24, as weak economic data boosted expectations for a Fed rate cut in September and potentially another soon after.

Finally, Rebecca Falconer of Axios reports that President Trump plans to announce a new Federal Reserve governor and BLS commissioner this week, following the resignation of Fed governor Adriana Kugler and his firing of BLS commissioner Erika McEntarfer. The appointments give Trump a chance to install officials aligned with his policies and increase pressure on Fed Chair Jerome Powell, whom he has criticized for resisting rate cuts. Trump, citing disappointing July and prior-month jobs data, said he has “a couple of people in mind” for the Fed role and will name both replacements within the next few days.

#LocalNews

Treh Manhertz of Zillow reports that 26.6% of home listings saw a price cut in June, the highest June share in Zillow data since 2018, with pandemic boomtowns like Denver (38.3%), Raleigh (36.4%), Dallas (35.5%), Nashville (35.5%), and Phoenix (35.5%) leading the nation. These markets, which surged during the remote-work migration, are now cooling as affordability pressures and slower population growth weigh on demand. Inventory remains 20.6% below pre-pandemic levels nationally but has already surpassed those norms in most of the top price-cut metros. Kansas City saw the sharpest monthly jump in cuts (+5 points), signaling a rapidly cooling market.

Dana Anderson of Redfin reports on similar data showing that that home prices fell year-over-year in 14 of the 50 largest U.S. metros, led by Oakland (-6.8%), West Palm Beach (-4.9%), Jacksonville (-3.1%), Austin (-2.9%), and Houston (-2.8%), as supply outpaces demand amid high costs and economic uncertainty. Homes are taking longer to sell in every major metro area; West Palm Beach, for instance, averaged 93 days to go under contract, up 18 days from last year.

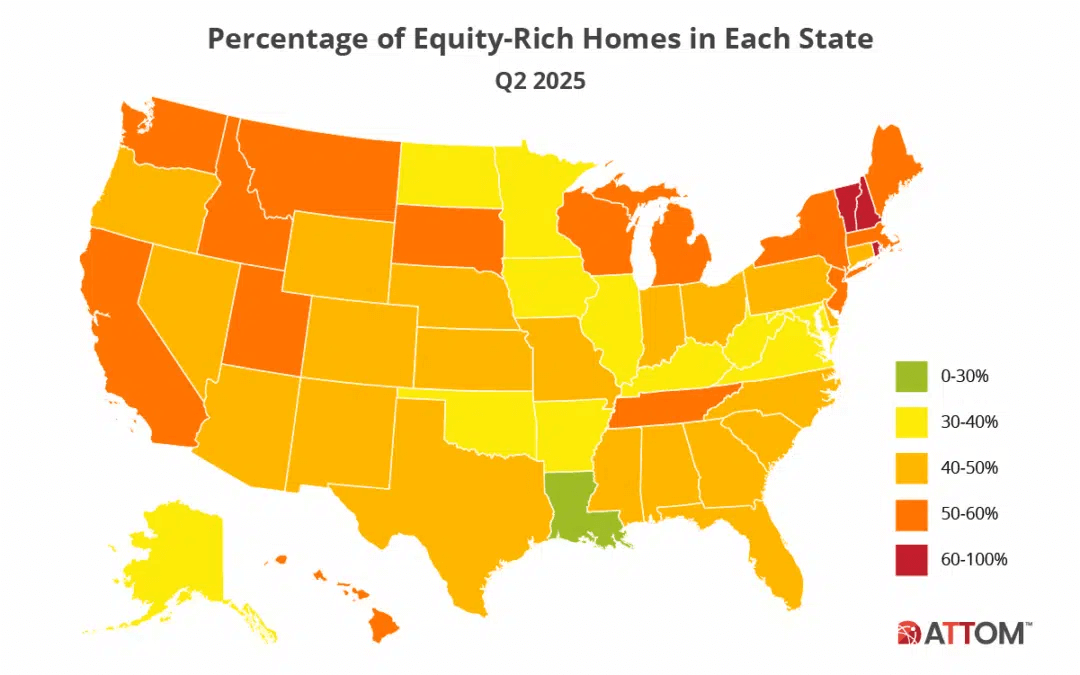

Megan Hunt of ATTOM Data Solutions reports that 47.4% of mortgaged U.S. residential properties were equity-rich in Q2 2025, up from 46.2% in Q1 and ending three consecutive quarterly declines, though still below the 49.2% peak in Q2 2024. Vermont led the nation at 84.9%, followed by New Hampshire (60.3%), Rhode Island (60.3%), Montana (59.2%), and Hawaii (59.2%). An equity-rich mortgage means the combined loan balance is no more than half the property’s estimated market value, underscoring continued homeowner equity strength despite shifting market conditions.

Source: ATTOM (August 2025)

Dana Anderson of Redfin reports in another article that Washington, D.C.’s housing inventory jumped 22.7% year over year in June, the third-largest increase since records began in 201, driven partly by former federal workers selling their homes after layoffs, buyouts, or early retirements. Pending sales fell 0.3%, homes took a median of 36 days to go under contract (up from 26 days a year ago), and only 35.7% sold above asking, down from 47.8%. Rising supply, stale listings, and uncertainty about the local economy are cooling buyer demand in the nation’s capital.

Source: Redfin (August 2025)