Samantha Delouya of CNN reports that President Trump proposed a 50-year mortgage aimed at cutting monthly payments by a few hundred dollars. Still, housing experts warn it could sharply raise the overall cost of homeownership. USC professor Richard Green notes that payment savings would be minimal while borrowers take far longer to build equity and pay dramatically more interest. Experts also caution that stretching loans to 50 years could fuel higher home prices, leaving buyers with lower monthly payments but significantly higher long-term debt.

Bill Chappell of NPR explains that President Trump’s proposal for a federally backed 50-year mortgage has sparked intense debate. Supporters argue it could help priced-out buyers enter the market, while critics, including Fox News’ Laura Ingraham, warn it’s a gift to banks that dramatically slows the path to ownership. The plan arrives amid stalled home sales driven by high prices and elevated mortgage rates, and it would keep borrowers in debt 20 extra years while front-loading even more interest than a 30-year loan. As NBKC Bank’s Chris Hendrix notes, buyers already pay mostly interest for the first decade of a 30-year mortgage.

Joel Berner of Realtor.com explains that the proposed 50-year mortgage aims to lower monthly payments, saving buyers at most $250 per month on a $400,000 home at 6.25%, but comes with steep long-term costs. A 50-year loan would accumulate $816,396 in total interest, compared to $438,156 for a 30-year mortgage, representing an 86% increase or $378,240 more. After 10 years, borrowers would also hold $42,308 more in remaining principal (a 10.6% gap), which would slow equity growth. Berner warns that boosting demand without increasing supply could raise home prices and erase any savings, arguing that reducing tariff-driven inflation and expanding homebuilding would provide far better affordability solutions.

Ryan Mancini of The Hill reports that Treasury official Joe Lavorgna cast doubt on President Trump’s newly floated 50-year mortgage idea, saying feedback suggests it’s “probably not an optimal approach” for improving affordability. Lavorgna noted that high interest rates and restrictive monetary policy remain major hurdles, and the administration is exploring all options to lower costs. Trump promoted the plan as a way to reduce monthly payments, but it has drawn pushback: FHFA Director Bill Pulte called it a “game changer.”.

Ben Carlson of AWOCS breaks down the math behind Trump’s proposed 50-year mortgage and shows why personal finance experts strongly dislike it. On a $500,000 loan at 6%, monthly payments fall only slightly, but the lifetime interest costs skyrocket. A 30-year mortgage starts with 83% of payments going to interest, while a 50-year mortgage starts at 95% interest, making equity buildup painfully slow. After 10 years, a borrower would have just $21,636 in equity on a 50-year loan versus $81,571 on a 30-year term. And if 50-year rates run even 0.40% higher, monthly savings drop to just $217.

Foreclosures and delinquencies

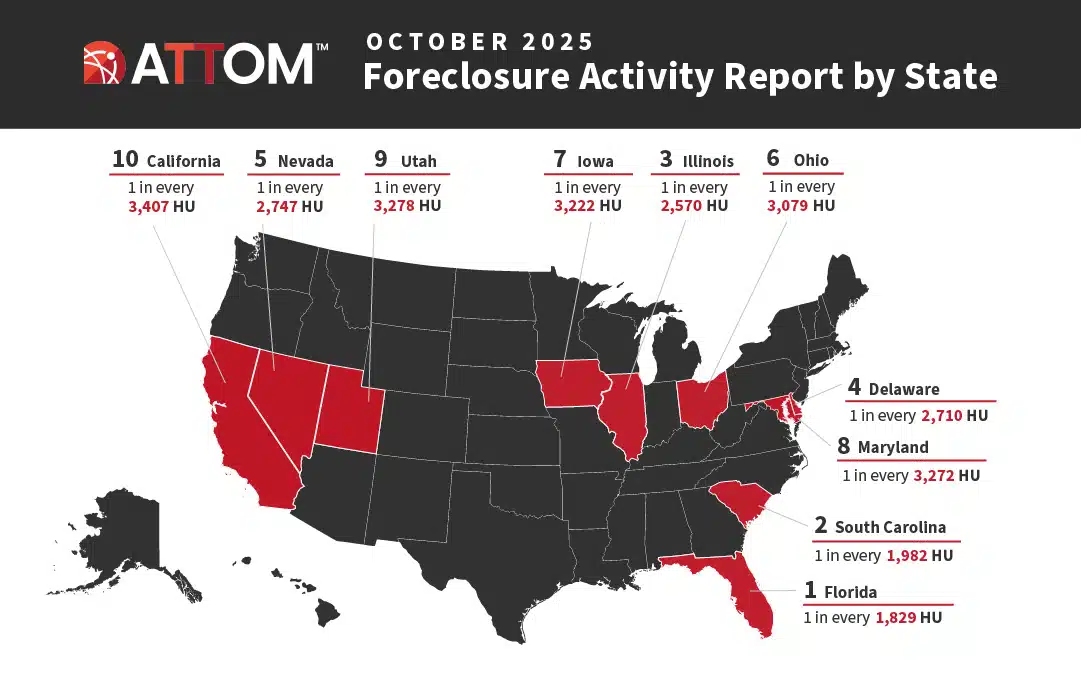

Megan Hunt of ATTOM reports that foreclosure activity rose again in October 2025, with 36,766 total filings, up 3% month-over-month and 19% year-over-year, translating to one filing per 3,871 housing units. Foreclosure starts climbed to 25,129 (up 6% from September and 20% annually), while lender repossessions reached 3,872, a 32% jump from last year. Florida posted the nation’s worst foreclosure rate at 1 in every 1,829 homes, followed by South Carolina and Illinois, highlighting broad affordability stress across multiple regions.

Source: ATTOM (November 2025)

ATTOM also reports that foreclosure activity rose for the eighth straight year-over-year increase in October 2025 as higher housing and borrowing costs pressure more homeowners. Nationwide, one in every 3,871 homes faced a foreclosure filing, with the highest state rates in Florida (1 in 1,829), followed by South Carolina, Illinois, Delaware, and Nevada. Major metros like Tampa saw elevated rates due to a temporary backlog, and the most foreclosure starts came from Florida, Texas, and California, even as some large MSAs logged declines. Despite the increases, ATTOM says activity remains below historic highs, reflecting a gradual market normalization.

Rob Barber, CEO at ATTOM, comments: “Foreclosure activity continued its steady upward trend in October, the eighth straight month of year-over-year increases. Starts rose nearly 20 percent, while completed foreclosures were up 32 percent from last year…Even with these increases, activity remains well below historic highs. The current trend appears to reflect a gradual normalization in foreclosure volumes as market conditions adjust and some homeowners continue to navigate higher housing and borrowing costs.”

Diana Olick of CNBC highlights that rising foreclosures are beginning to intersect with broader economic stressors, suggesting early pressure points rather than an imminent crisis. Despite 36,766 filings in October and eight straight months of annual increases, overall foreclosure levels remain far below Great Recession peaks (under 0.5% of mortgages, compared with 4% at the prior peak). However, Rick Sharga of CJ Patrick Co. flags emerging vulnerabilities: FHA loans now account for 52% of all seriously delinquent mortgages, with FHA delinquencies exceeding 11%, indicating likely increases in 2026. States hit by falling home prices and soaring insurance costs (particularly Florida and Texas) are seeing more defaults. At the same time, stubbornly high mortgage rates, record consumer debt, rising delinquencies across other credit types, and a softening job market all set the stage for potential upticks in distress, even if demand remains strong enough to quickly absorb distressed inventory.

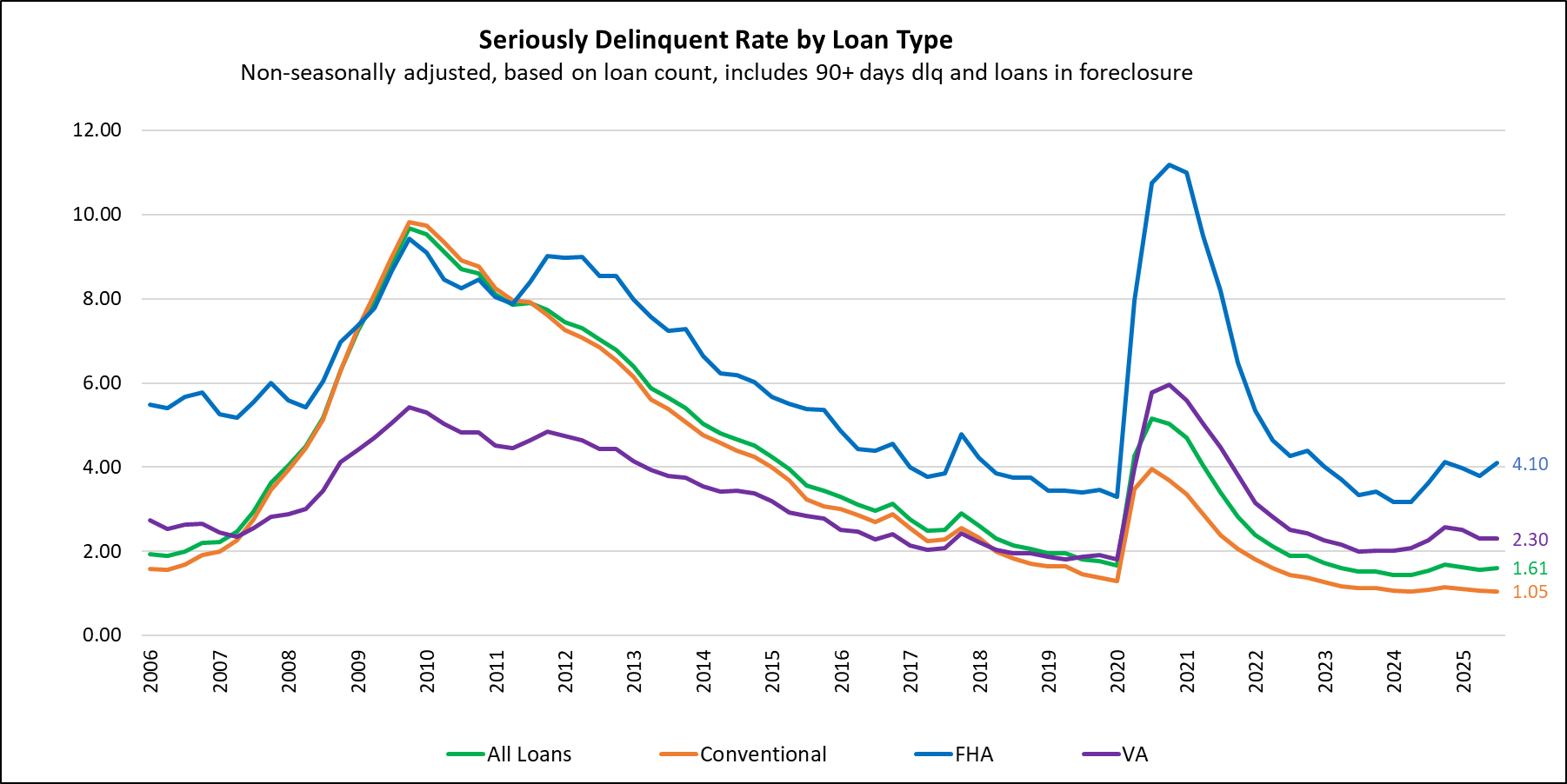

The Mortgage Bankers Association (MBA) reports that mortgage delinquencies ticked higher in Q3 2025, rising to 3.99% of all loans, up 6 basis points from Q2 and 7 basis points year-over-year. Foreclosure starts edged up to 0.20%. MBA’s Marina Walsh says the deterioration is being driven almost entirely by FHA borrowers, whose seriously delinquent rate has climbed nearly 50 basis points over the past year, unlike the relatively stable conventional and VA segments. She cites a softer labor market, rising taxes and insurance, heavier household debt, and localized home price declines as key pressure points that are straining affordability and limiting refinancing or sale options.

Source: MBA (November 2025)

Policy updates

Flávia Furlan Nunes of HousingWire reports that the FHFA is actively exploring whether Fannie Mae and Freddie Mac could offer assumable or portable mortgages as part of the Trump administration’s push to improve affordability. Assumable loans (where a buyer takes over the seller’s existing rate and balance) are getting cautious industry support, especially given today’s high-rate environment.

However, Nunes reports that portable mortgages, which would allow borrowers to transfer their current mortgage from one home to another, are drawing far more skepticism, as the product is rare in the U.S. and raises significant operational and risk-management challenges. The discussion comes on the heels of Trump floating a 50-year mortgage proposal, which critics say would do little to solve affordability due to dramatically higher lifetime interest costs.

Jake Krimmel of Realtor.com argues that portable mortgages would primarily benefit current homeowners with “golden ticket” pandemic-era rates, while potentially pushing home prices even higher. Because only low-rate borrowers could port cheap financing into a 6% market, their added purchasing power would inflate prices for everyone else, widening the divide between owners and renters. Krimmel also stresses that portability simply doesn’t fit the U.S. securitization system: mortgages are priced around the specific property backing them, and allowing loans to move would disrupt collateral risk, break existing contracts, and likely force rates higher to compensate, making the idea both inequitable and impractical.

Brian Slodysko of AP News reports that senior Fannie Mae officials were ousted after raising alarms over a “very problematic” incident in which Lauren Smith, acting at FHFA Director Bill Pulte’s request, shared confidential mortgage-pricing data with Freddie Mac, a direct competitor. Internal emails show executives warned the disclosure could expose Fannie Mae to accusations of collusion and sought legal guidance, only for those sounding the alarm (and internal ethics investigators probing Pulte) to be forced out weeks later.

Jennifer Ludden of NPR reports that the Trump administration is overhauling federal homelessness policy by sharply cutting long-term, permanent housing programs and redirecting funding toward transitional housing that is tied to work and addiction treatment requirements. While HUD says the shift boosts total homelessness funding from $3.6B to $3.9B and aims to promote “self-sufficiency,” critics warn that 170,000 people could lose stable housing, especially since funding notices are late and may leave months-long gaps before new money arrives.