Diana Olick of CNBC reported that homebuilder sentiment dropped again in June as the NAHB/Wells Fargo Housing Market Index slipped two points to 35, marking the 14th straight month below the break-even level of 50. All three index components weakened, with present sales conditions, buyer traffic, and six-month sales expectations all moving lower. Builders cited persistent affordability pressure, elevated mortgage rates, and softening demand heading into the summer selling season.

That said, Robert Dietz of NAHB reported that 35% of builders cut prices in June, up from 32% in May, with the average price reduction holding at 6%. The share of builders using sales incentives climbed to 62%, the 15th straight month above 60%. Regional HMI readings remained uneven, with the Northeast at 44, the Midwest at 43, the South at 33, and the West at 27. A major driver of this is rising interest rates, according to NAHB.

Source: NAHB (June 2026)

Further, Kristin Schwab of Marketplace reported that incentives now account for roughly 7% of asking prices, about twice the pre-pandemic norm, as builders work to keep buyers off the sidelines. Rate buydowns, closing-cost credits, and design-center upgrades have replaced sticker price cuts as the preferred tool. The outlet noted that incentive-heavy pricing makes it harder for resale sellers to compete with new construction in the same submarket.

However, Eli Knaap of Fast Company reported that Lennar disclosed an average incentive of about $55,000 per home on its June 12 earnings call, the highest level the builder has ever reported. Co-CEO Stuart Miller told analysts that affordability is the most stretched it has been in years and that the company is leaning on volume over margin to keep its production machine running. Lennar shares slipped after the print as gross margin guidance came in below Street estimates.

Finally, Dave Gallagher of RealEstateNews.com reported that the recent plunge in construction starts may overstate the slowdown because builders are still working through a deep backlog of homes already under construction. For investors, the combination of falling starts and rising incentives points to thinner builder margins ahead, as well as a smaller new-supply pipeline into 2027, which could support rents and resale pricing in undersupplied metros.

Housing bill nears the finish line

Tristan Navera of Realtor.com reported that House and Senate leaders reached a compromise on the 21st Century ROAD to Housing Act after months of gridlock, with the Senate voting 87-8 on a procedural motion to advance the House-amended version. The final bill packages 45 provisions across roughly 380 pages, covering everything from limits on institutional investors to small-bank deregulation. Senate Banking Chair Tim Scott and Ranking Member Elizabeth Warren announced the deal alongside House Financial Services counterparts French Hill and Maxine Waters.

That said, Diana Olick of CNBC reported that the bill caps single-family purchases by large institutional investors at 350 homes per entity, while dropping a contested Senate provision that would have forced build-to-rent operators to sell newly built single-family rentals after seven years. Senator Warren told the network the restriction is the first federal limit ever placed on private equity expansion into a U.S. industry. Existing holdings above the cap are grandfathered, but additional purchases trigger civil penalties of up to $1 million or three times the purchase price.

Further, Realtor.com reported that the compromise package could also reshape mortgage lending by easing rules on community banks and lowering barriers to de novo bank charters. The bill includes a small-dollar mortgage pilot for loans under $100,000, raises the bank public-welfare investment cap from 15% to 20% of capital, and modernizes the HOME Investment Partnerships Program by lifting income eligibility to 100% of area median income. The 30-year fixed averaged 6.47% the week the deal was announced.

However, Rebecca Picciotto of The Wall Street Journal reported that the agreed text includes a ban on investor purchases of existing single-family homes for portfolios above the 350-home threshold, a measure President Trump pushed earlier this year. Exceptions remain for new construction, distressed properties bought for renovation, planned rental communities, and 55-and-older housing. The cap sunsets 15 years after enactment unless Congress acts to extend it.

Finally, Meghan Roos of RealEstateNews.com reported that industry advocates believe the package is ready to become law within two to three weeks, with Senator Scott telling CNBC on June 18 that the bill could reach the president’s desk in that window. The House is expected to take up the Senate-cleared version when it returns from recess on June 23. For real estate investors, the 350-home cap sets a clear ceiling on institutional single-family rental growth while the BTR carve-out preserves the build-to-rent development pipeline.

CRE deal value keeps climbing

S&P Global Market Intelligence reported that U.S. commercial real estate deal value continued to grow in the 12 months ended March 31, with office transaction value jumping 44.4% year over year to $81.79 billion and trading at an average 6.3% cap rate. Industrial volume rose 16.8% to $111.45 billion, the largest sector by dollar volume, while retail climbed 29.8% to $63.65 billion. Manhattan led the office market with $11.85 billion in trades, up 34.2% year over year.

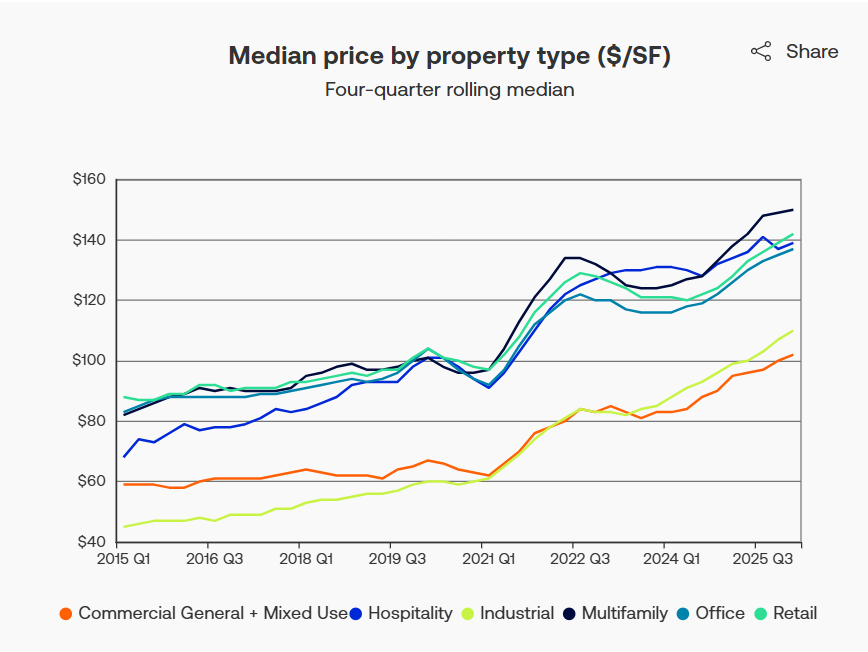

That said, Ciaran Brennan of Bisnow reported that the pricing spread between this cycle’s winners and laggards is the widest on record. Industrial pricing is up 88.5% since the quarter before the pandemic, while office is up just 36.6% over the same stretch, according to Altus Group. Multifamily now trades at a median of $150 per square foot, office at $137, retail at $142, hospitality at $138, and industrial at $110.

Further, Altus Group reported that the Q1 2026 median transaction price hit a record high of $129 per square foot across all property types, marking the twelfth straight quarter of gains. Year-over-year price growth has cooled from a peak of 11.7% in Q3 2025 to 8.7% in Q1 2026. Median per-square-foot prices have more than doubled in the 16 years since the 2009 cycle low of $56 per square foot.

Source: Altus Group (June 2026)

However, Arnie Aurellano of Scotsman Guide reported that multifamily led every sector in Q1 2026 transaction activity, accounting for 29.2% of single-property transaction value and 29.6% of properties traded. Industrial captured 22.4% of dollar volume on only 14.8% of properties, the widest value-to-count gap of any sector. Deals between $1 million and $10 million made up 38.6% of single-property transaction value, while sub-$1 million deals accounted for just 11%.

Finally, PwC reported that U.S. real estate deal activity is no longer defined by a traditional cyclical recovery, with capital rotating toward digital infrastructure, logistics, senior housing, and residential-oriented housing while moving away from legacy property types facing refinancing pressure. U.S. equity REITs entered 2026 trading at a median 16.2% discount to net asset value, a public-private gap PwC expects to drive consolidation and take-private activity. For investors, the takeaway is that headline transaction growth is real but concentrated, with industrial and multifamily continuing to outperform office on both pricing and absorption.