Dave Gallagher of RealEstateNews.com reported that the average 30-year mortgage rate climbed to 6.51% in the past week, according to Freddie Mac, with Mortgage News Daily clocking 6.65% on May 21 (up from 6.52% a week earlier) as the 10-year Treasury yield pushed to 4.66% by May 18 versus below 4% in March. Redfin’s weekly read showed pending sales down 1.1% for the week ending May 17, and the MBA purchase index slipped 4% on the week. Bright MLS cut its 2026 existing-home sales forecast to +3.8% from +9% in December and now expects the median price to fall 0.5% on the year, versus a prior call for a 0.9% gain.

Falen Pitts of the Mortgage Bankers Association (MBA) reports that mortgage demand softened last week, with total applications falling 2.3% as higher borrowing costs continued to pressure buyers. Purchase applications dropped 4% week over week, though they still came in 8% higher than the same period a year ago, suggesting some resilience in homebuying activity despite affordability challenges. Refinancing activity was nearly flat, slipping just 0.1% from the prior week, but remained 35% above year-ago levels as more homeowners continue to react to rate shifts and opportunities to lower monthly payments.

Joel Kan, MBA’s Vice President and Deputy Chief Economist, comments:

“Ongoing concerns around inflation from higher fuel costs, combined with rising concerns over global public debt, pushed Treasury yields higher in the U.S. and abroad last week. This resulted in higher mortgage rates across the board, with the 30-year fixed rate increasing to 6.56 percent, its highest level in seven weeks…Overall applications were down to the lowest level in five weeks as purchase borrowers pulled back across conventional and government loan types. Refinance applications were essentially unchanged, with a decline in government refinances and an increase in conventional refinancing, likely as the increase in rates came late in the week.”

That said, Jeff Cox of CNBC reported that incoming Fed Chair Kevin Warsh may need to advocate for rate increases to build credibility, according to Ed Yardeni of Yardeni Research, after the 30-year Treasury yield broke above 5% on May 15 for the first time in nearly a year. CME Group’s FedWatch tool puts the probability of a year-end rate hike at 42%, but Yardeni sees a quarter-point move as soon as July, with the Fed scrapping forward guidance at the June meeting to clear the way. Markets that expected the Trump pick to deliver cuts are increasingly pricing in the opposite, a sharp pivot from earlier-year expectations.

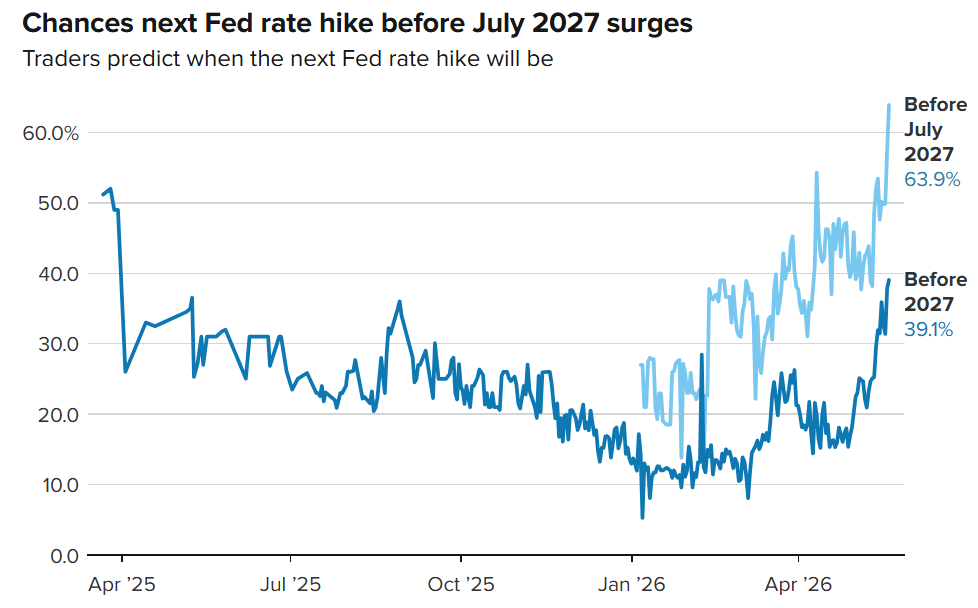

Further, Davis Giangiulio, also of CNBC, noted that prediction-market traders on Kalshi now estimate a 64% probability that the next Fed rate hike will arrive by July 2027 and a 43% chance of tighter monetary policy this year, while Polymarket assigns a 35% probability of a 2026 hike. The rate-hike odds surged in the past 24 hours on rising Treasury yields, persistent inflation, and no relief in oil prices amid the Iran conflict. Previously, traders had assigned equal odds of a hike landing in the first half of 2027.

Source: CNBC (May 2026)

However, Yahoo Finance covered the May 22 swearing-in of Kevin Warsh as Fed Chair, who inherits an inflation backdrop that has run above the 2% target for more than five years. Senate confirmation on May 13 was 54-45, and the new chair faces an April PPI that surged 6% on the year (driven by energy) plus an April CPI reading of 3.8% headline (up from 3.3% in March) with core at 2.8% (up from 2.6%). CME FedWatch traders now price a 57% probability of at least one hike by December, and Evercore ISI’s Krishna Guha said the data support the hawkish minority’s view that the next move could be up rather than down.

April housing starts

The U.S. Census Bureau reported on May 21 that privately-owned housing starts in April fell 2.8% to a seasonally adjusted annual rate of 1.465 million, with single-family starts tumbling 9.0% from the revised March figure of 1.022 million to 930,000. Multifamily starts in buildings with 5+ units came in at 529,000. On the permits side, total authorizations rose 5.8% to 1.442 million but remain 0.2% below the April 2025 level, with single-family permits down 2.6% to 872,000 and 5+ unit permits at 514,000. The release highlights a softening single-family pipeline alongside a rebound in multifamily activity.

That said, Lance Murray of The MortgagePoint noted that the headline starts drop undershot the consensus estimate of -3.5%, with single-family permits sliding back to their lowest level since summer 2025 and single-family completions declining for the sixth consecutive month. The six-month moving average for single-family permits has effectively flattened after a long stretch of declines, while the multifamily-driven permits masked underlying caution in for-sale construction. Construction activity remains active enough to avoid signaling outright weakness but cautious enough to reflect ongoing affordability and financing pressures.

Further, the National Association of Home Builders (NAHB) released the May NAHB/Wells Fargo Housing Market Index, which rose by three points to 37 (any reading below 50 indicates more builders see conditions as poor than good). Current sales conditions climbed three points to 40, future sales gained three points to 45, and the index charting buyer traffic rose three points to 25. By region (three-month moving average), the Midwest registered 43, the Northeast 42, the South held at 35, and the West slipped one point to 28. The modest improvement comes despite rising mortgage rates and persistent affordability constraints, with builders still grappling with elevated land, labor, and construction costs.

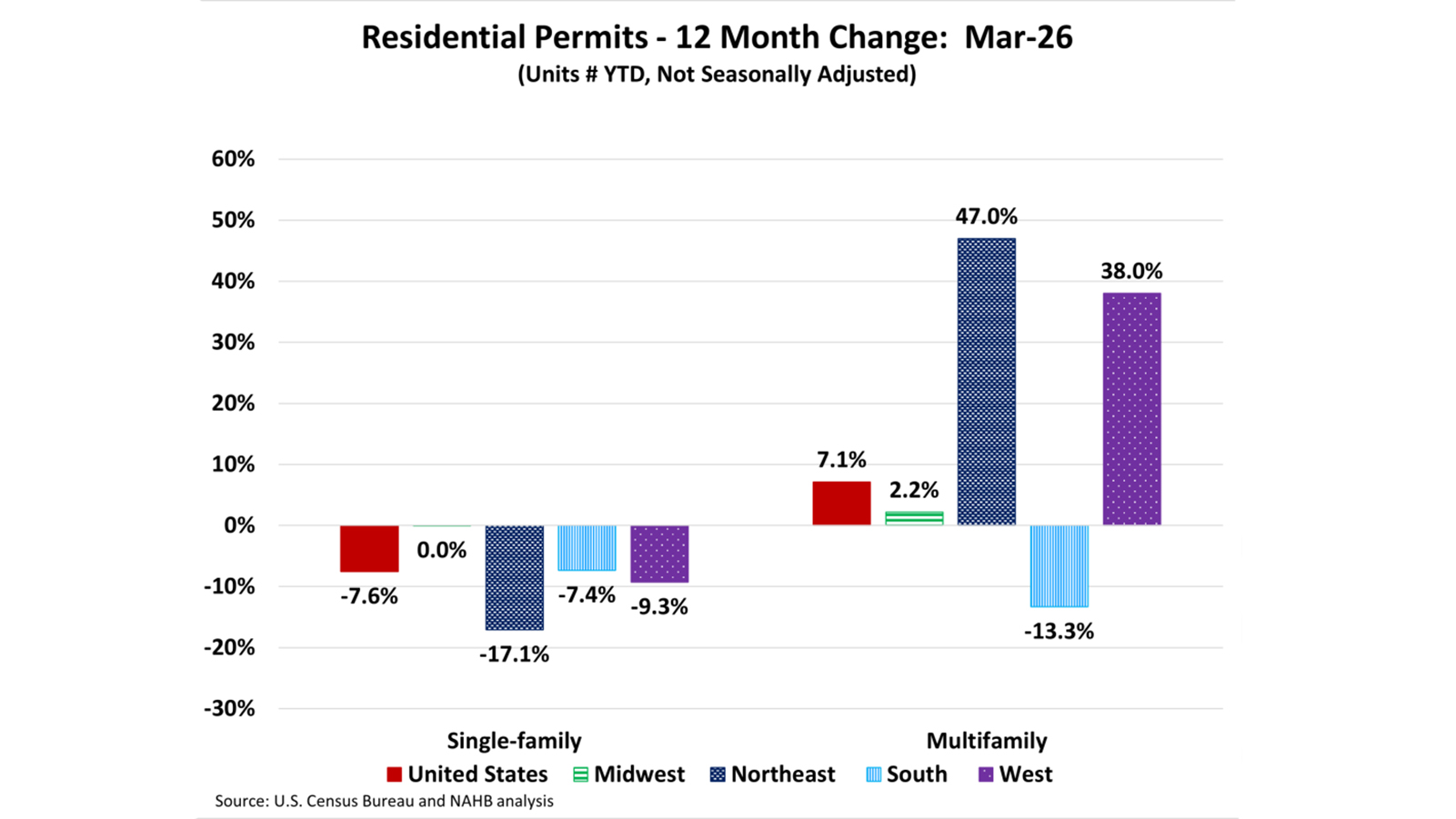

However, NAHB Eye on Housing showed that the first-quarter picture is weaker than the May sentiment bounce suggests, with Q1 2026 single-family permits dropping 7.6% year over year to 214,655 units while multifamily permits rose 7.1% to 121,404. Just 12 states recorded year-over-year increases in single-family permits in March (Maryland posted the steepest decline at -25.4%), and Texas (-8.3%), Florida (-6.7%), and North Carolina (-15.4%) all retrenched from prior-year levels. The data underscore a broad-based pullback in single-family pipeline activity even as multifamily permits stay supported by rental demand.

Source: NAHB (May 2026)

Finally, TD Economics wrote that homebuilding activity fell at the start of the second quarter, as softer single-family starts weighed on the aggregate, while the more volatile multifamily segment notched a three-year high in starts and sustained its gradual recovery. With single-family permitting declining for a second consecutive month and builder sentiment remaining subdued in May, the firm sees starts likely softening further in the coming months. For investors, a thinner for-sale pipeline plus elevated rates could keep existing-home inventories tight and support rental demand into the back half of the year.

Commercial real estate

David Nusbaum of the LA Times comments on the a new report highlighting a shift across Southern California, where companies are acquiring office and industrial properties rather than renewing leases amid waning institutional confidence. The State Compensation Insurance Fund bought a 158,785-square-foot Class A office at 35 N. Lake Ave. in Pasadena, Capital Group acquired Bank of America Plaza in downtown LA from Brookfield for roughly $210 million ($150 per square foot), and Future Foam paid $145 million in Orange County for two buildings (417,000 sq ft) it had previously leased from Principal Real Estate Investors. Robinson Pharma added $40.7 million in Santa Ana and Jiaherb paid $53.7 million in Brea, while LA office vacancy declined to 15.7% and Orange County office sales jumped 76% year over year.

“We are seeing a meaningful shift from renting to owning in Downtown L.A., and that’s one of the strongest signals that market confidence is returning. Owner-user acquisitions do not happen in declining markets; they happen when users believe the bottom is in.”

That said, Janus Henderson Investors argued that CMBS outcomes are increasingly bifurcated across the office sector, with delinquency rates climbing from 1.6% in 2022 to more than 12% in 2026, but the stress is concentrated in older, commodity-like buildings rather than trophy assets. Trophy assets show roughly 6.3% vacancy versus 15.7% for Class B, and Midtown Manhattan prime vacancy fell to just 2.9% in Q1 2026, according to CBRE Research. Top-tier NYC buildings are now tracking 70%+ pre-COVID attendance norms, supporting leasing and rent trends in the best assets. Despite negative office headlines, CMBS broadly has returned 5.66% annualized over the past three years versus 5.06% for investment-grade credit, with shorter duration (3.46 years vs. 6.69) and higher average credit quality (Aa1 vs. Baa1).

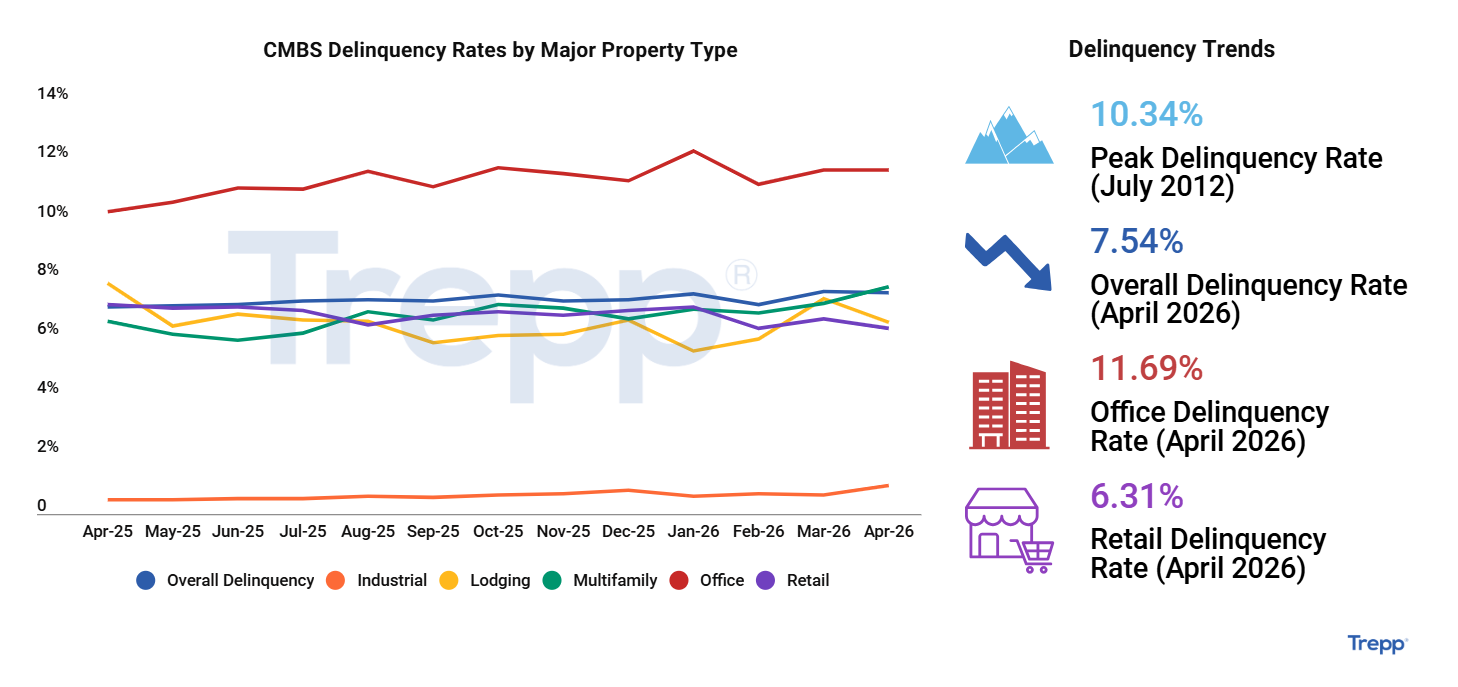

Further, Trepp noted that the Trepp CMBS Delinquency Rate climbed 17 basis points in January 2026 to 7.47%, with a net increase of nearly $1.6 billion in delinquent loans driven primarily by the office sector. Office alone accounted for more than half of the reappraised balance. The data reinforce the message from weekly servicer commentary: stress is concentrating in commodity office collateral with near-term maturities, and selective opportunities remain in better-positioned office credits where occupancy and rent fundamentals hold up.

Source: Trepp (May 2026)

However, Connect CRE reported that price growth across CRE property types diverged in April, with CBD office leading at +4.1% year over year, while apartment prices declined annually. The data are consistent with the bifurcation story: top-tier urban office is regaining pricing power as occupiers return and absorb prime supply, while broader CRE remains uneven. For investors, the combination of selective office price gains alongside rising office CMBS delinquency points to a market where asset-level underwriting matters more than sector-level calls.

Finally, JLL Capital Markets announced that it arranged a $69 million recapitalization of Piatt Companies’ Tower Two-Sixty, a trophy mixed-use asset in downtown Pittsburgh featuring 130,000 sq ft of Class A+ office, 14,000 sq ft of ground-floor retail, a 197-key Hilton Garden Inn, and a 321-space parking garage. The transaction involved a ground-lease bifurcation sale of the land to Woodbranch Investments Corp and leasehold financing through Dollar Bank. The deal is a concrete example of capital still flowing to trophy product in secondary CBDs, even as commodity offices face accelerating distress.