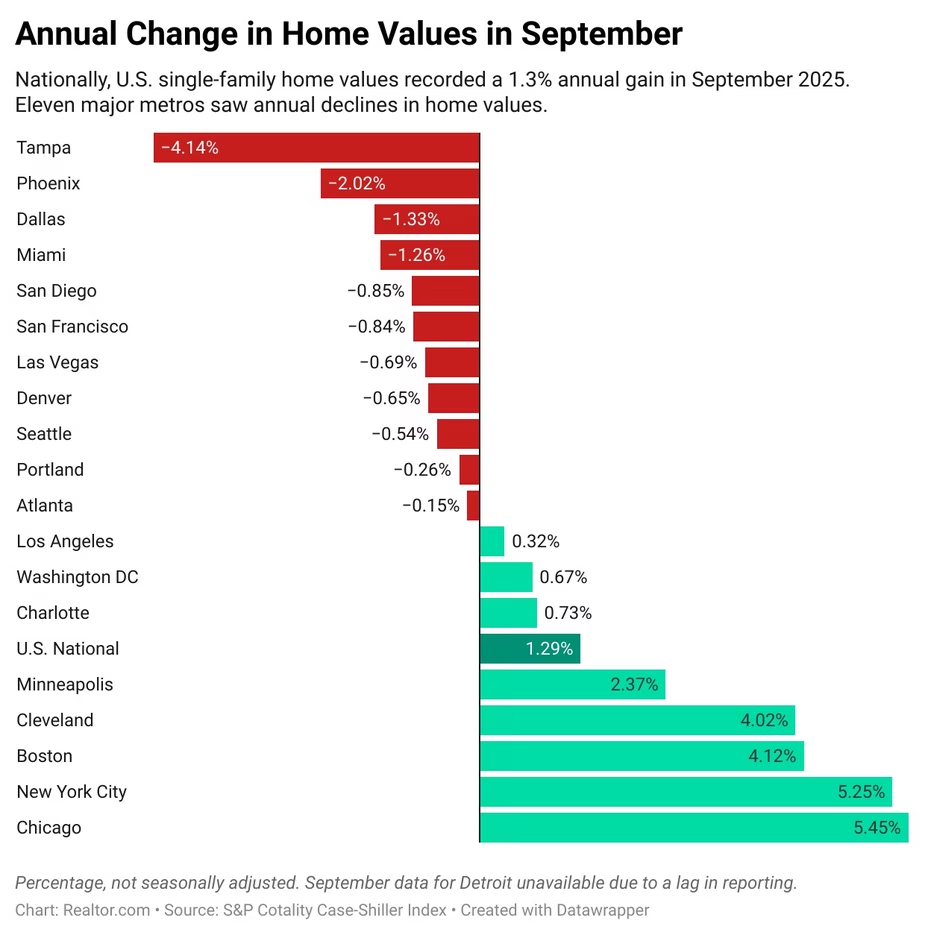

Keith Griffith of Realtor.com reports that U.S. home values are losing momentum, with the S&P CoreLogic Case-Shiller Index showing just a 1.3% annual gain in September (the weakest since mid-2023) and prices falling year-over-year in 11 of the 20 major metropolitan areas tracked, all of which are located in the South and West. Tampa (-4.14%) and Phoenix (-2.02%) posted the sharpest declines, while Chicago (+5.45%) and New York (+5.25%) led price growth. All 20 metros experienced month-over-month declines before seasonal adjustment, highlighting a broad affordability-driven weakness amid mortgage rates averaging 6.35%.

Source: Realtor.com (December 2025)

National price growth has now trailed inflation for four consecutive months, resulting in real prices being slightly negative. Yet, even declining markets remain far above pre-pandemic levels, Tampa’s values are still up 55% over the past five years. Analysts say the market is settling into a state of fragmented price growth as high borrowing costs continue to suppress demand.

Further, the U.S. Federal Housing (FHFA) reports that home prices rose 2.2% year over year in Q3 2025 and 0.2% quarter over quarter, with September’s monthly index flat. Prices increased in 44 states, led by Illinois (+6.9%) and New York (+6.8%), while Florida saw the steepest decline at –2.3%. Among the 100 largest metros, 76 posted annual gains, with Allentown-Bethlehem-Easton up 9.7% and Cape Coral–Fort Myers plunging 10.8%. Every census division except the Pacific (+0.1% decline) saw annual growth, underscoring continued (though uneven) national appreciation.

Jesse Wade of the National Association of Home Builders (NAHB) reports that residential building material costs accelerated in September, with the PPI for inputs to new residential construction rising 0.2% month over month and 3.1% year over year, the fastest pace since early 2023. Goods inputs, which make up about 60% of construction costs, increased 0.1% on the month and 3.5% annually, driven by a 1.0% jump in energy inputs and a 3.5% rise in building materials. Significant annual spikes were observed in parts for construction machinery (+41.3%) and metal molding and trim (+31%), while ready-mix concrete increased by just 0.4% and softwood lumber declined by 2.3% amid oversupply.

Niccolò Conte of Visual Capitalist highlights that the U.S. remains a central focal point of global housing bubble risk in 2025, with Miami ranking #1 worldwide on the UBS Bubble Index at 1.73, firmly in bubble territory and supported by rising real prices (+1.9%). Los Angeles also appears prominently, scoring 1.11, placing it in the “overvalued” zone with modest price growth (+0.9%). While bubble risk eased in many global markets, several U.S. cities, including San Francisco, saw price declines as high borrowing costs suppressed demand. Overall, the U.S. presents a mixed picture: Miami’s overheating contrasts sharply with cooling, correction-phase markets in other major metros.

Megan Hunt of ATTOM reports that while overall purchase mortgage activity fell in Q3 2025, down 4.8% from the prior quarter and 6.6% year over year, several metros bucked the trend with significant spikes in purchase originations. Leading the nation were South Bend (+51.7%), Indianapolis (+51.4%), and Honolulu (+45.9%), followed by Buffalo (+38.3%) and Tucson (+28.8%). Nationally, lenders issued 1.77 million mortgages across all product types, representing a 1.9% annual increase in volume. However, purchase loans declined to 43.2% of originations, as refinance and HELOC volumes increased.

Rents

Jiayi Xu and Danielle Hale of Realtor.com report that rents fell for the 27th consecutive year-over-year month in October 2025, with median asking rents for 0–2 bedroom units down 1.7% (-$29) to $1,696 across the 50 largest metros. Rents remain $63 (-3.6%) below their August 2022 peak but are still $245 (16.9%) above pre-pandemic levels, despite a decline in real rents over the past six years. All unit sizes experienced annual declines: studios (-2.1%), one-bedroom units (-1.9%), and two-bedroom units (-1.7%).

Source: Realtor.com

The report highlights a significant shift in demand toward lower-cost metros, as 20 of the 50 largest markets now have more out-of-market renters than local ones. Detroit, Philadelphia, and Sacramento show the most significant swings. In Q3, New York had the highest share of local renters (74.8%), while Raleigh-Cary drew the most out-of-market demand (69.6%).

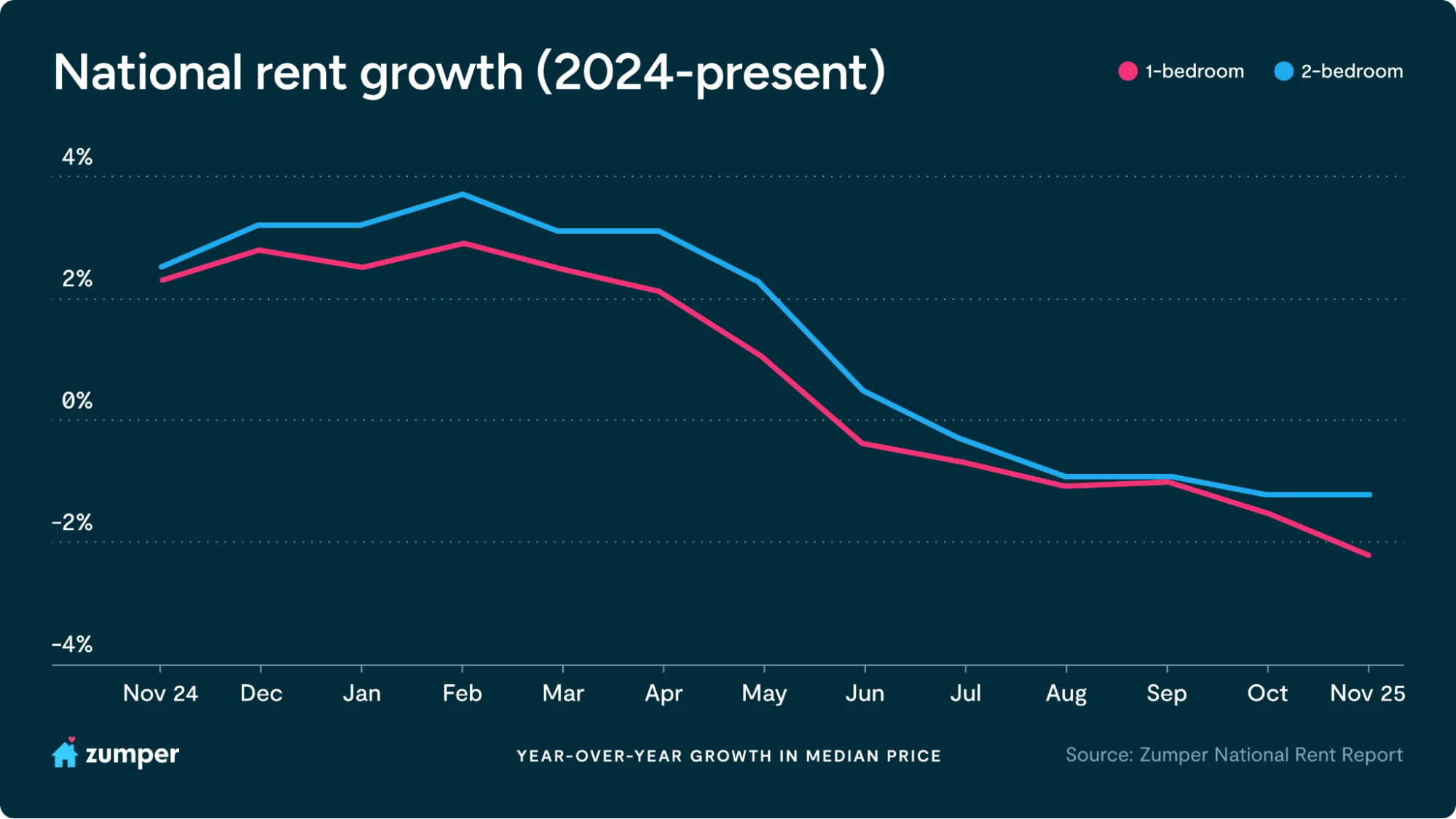

Crystal Chen and Quentin Proctor of Zumper report that rents continued to cool in November, with Zumper’s National Rent Index showing its fifth straight month of flat or declining prices: one-bedroom rents fell 0.7% to $1,501, and two-bedrooms slipped 0.4% to $1,880, down 2.2% and 1.2% annually, the sharpest yearly drop for one-bedrooms on record. Markets diverged sharply, with San Francisco posting the nation’s fastest rent growth (one-bedroom: +15.9%, two-bedroom: +14.8%), while Arizona metros such as Phoenix, Glendale, and Mesa saw declines of 7–10% due to record supply.

Source: Zumper (December 2025)

Anthemos Georgiades, CEO of Zumper, comments:

“Our National Rent Index shows one-bedroom rent down more than 2% year-over-year, the steepest decline we’ve recorded since we started tracking national rent data…It’s a clear signal that the cooling we’re seeing isn’t just seasonal. This pattern is playing out across most of the country, with only a few outliers, like San Francisco, moving in the opposite direction. It reflects a two-tiered economy and rental landscape: many markets are slowing under softer labor conditions, while a small number of high-wage hubs continue to accelerate.”

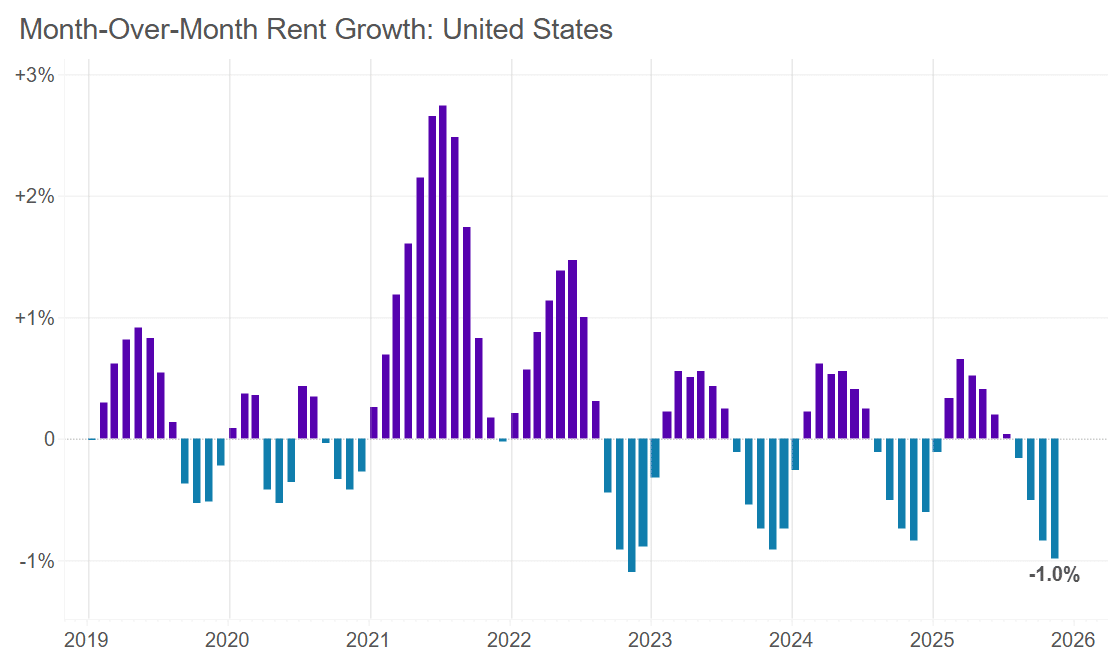

Apartment List reports on its own data, showing that rents fell 1.0% in November (the fourth straight monthly drop), bringing the national median rent to $1,367, down 1.1% year over year and 5.2% below its 2022 peak. A record-high 7.2% multifamily vacancy rate is driving the softness as the market absorbs an unprecedented surge in construction, with more than 600,000 units delivered in 2024 and elevated supply still entering the market. Units now take 36 days on average to lease, two days longer than last year, and metro performance is highly uneven: Austin leads declines with rents down 6.8% annually, while Providence posts the strongest growth at +5.2%.

Source: Apartment List (December 2025)

Mortgage rates

Jake Krimmel of Realtor.com reports that mortgage rates inched down to 6.23%, a 3-basis-point drop, as markets price in a higher likelihood of a Federal Reserve rate cut in December. A cut would push rates toward 2025 lows and add welcome support to a housing market already showing mild improvement: pending home sales rose 1.9% in October, existing home sales have logged four straight months of annual gains, and builders are offering more competitive pricing and financing. With the fall buying season closing, the trajectory of both mortgage rates and housing demand now hinges on upcoming inflation and labor data and whether the Fed ultimately follows through on the expected cut heading into 2026.

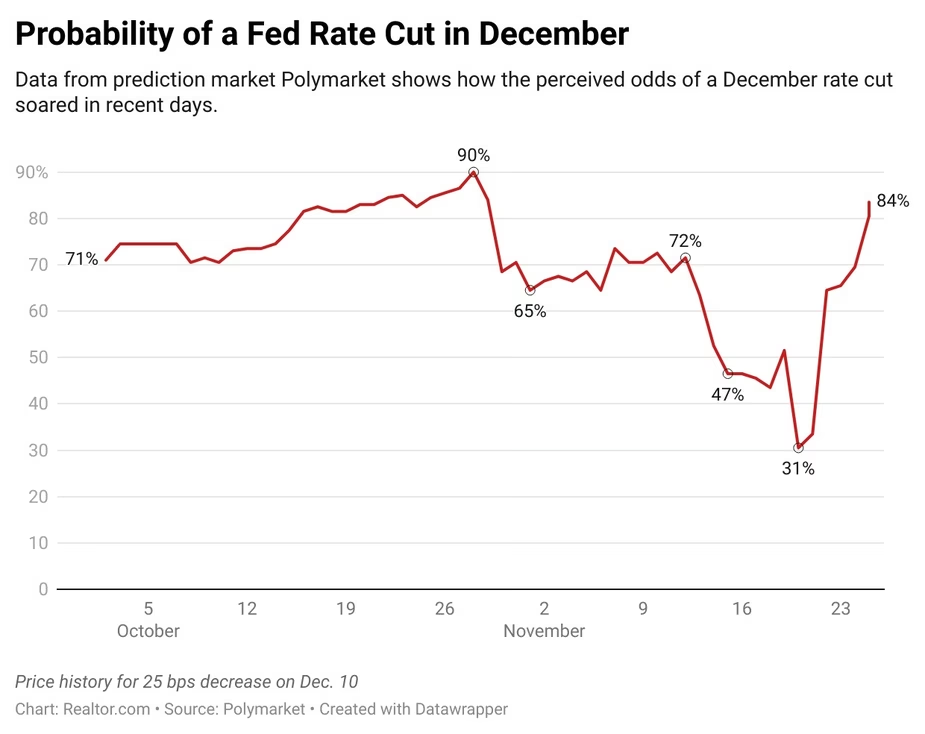

Keith Griffith, also of Realtor.com, reports that expectations for a December Fed rate cut have now surged to roughly 85%, up from a 50-50 split a week earlier, after key Powell allies (New York Fed President John Williams and San Francisco Fed President Mary Daly) signaled support for lowering rates “in the near term.” Despite dissent from Boston’s Susan Collins and St. Louis’s Jeff Schmid over concerns about inflation, markets now see the Fed trending toward a third consecutive rate cut, following recent moves that brought the policy rate to 3.75%–4%. Treasury yields responded quickly, with the 10-year briefly dipping below 4%, suggesting further easing in mortgage rates, which already hit a one-year low of 6.17% in October.

Source: Realtor.com (December 2025)

“It’s hard to think of something that would reverse the momentum toward a cut we’ve seen this week, but there are still over two weeks until the meeting, which can be an eternity in this uncertain macro environment…A few major FOMC voices would have to change their tune or some really troubling inflation/labor data would have to surface.”

Jim Edwards of Fortune explains that markets are increasingly convinced the Fed will cut rates in December as macro data aligns almost perfectly with the Fed’s dual mandate: weaker job growth and lower inflation. Goldman Sachs and UBS both signaled that this combination strongly supports another cut, potentially even multiple cuts over the next six months. Despite turbulence in tech (Nvidia down nearly 6% this month and Michael Saylor’s firm plunging 40%) investors remain upbeat: the S&P 500 has logged four straight gains, sits just 1% below its all-time high, and retail investors snapped up $5.8B in stocks this week. Add in $1 trillion in corporate buybacks over 12 months, and markets appear primed for another rally heading into the Fed’s Dec. 9–10 meeting.