According to a Reuters poll, the Fed was widely expected to raise 25 basis points and hold for the remainder of the year. Further, the poll revealed that we will experience a “short and shallow” recession sometime this year. “Nearly 90% – 94 of 105 – of the economists who participated in the latest Reuters poll, predicted the U.S. central bank would hike its key policy rate by 25 basis points to the 5.00%-5.25% range at a May 2-3 meeting,” which is in line with market expectations.

Jeff Cox of CNBC reports on Fed meeting minutes showing that the central bank expects the ongoing banking crisis to fuel a forthcoming recession. Fed officials expect a GDP growth of only 0.4% for the rest of 2023, with Cox quoting Federal Open Market Committee Vice Chair for Supervision Michael Barr saying, “[g]iven their assessment of the potential economic effects of the recent banking-sector developments, the staff’s projection at the time of the March meeting included a mild recession starting later this year, with a recovery over the subsequent two years.”

Ben Casselman and Jeanna Smialek of the New York Times note that although wage and inflation growth are decelerating, these critical indicators for the Fed remain stubbornly high. Wages were up 5.1% year-over-year in March, and core inflation sat at 4.6%, slightly down from 4.7% the previous month. This data will “likely to add to policymakers’ conviction that their work is not done — officials are widely expected to raise rates a quarter percentage point, to just above 5 percent, when they meet next week. That would be the central bank’s 10th consecutive rate increase.”

In commenting on the slowing growth of core inflation, Orphe Divounguy of Zillow notes: “Further disinflation ought to eventually cause long-term yields, including mortgage rates, to fall. The yield on the 10-year Treasury, which mortgage rates tend to follow closely, fell on today’s news. That is good news for would-be home buyers frustrated by affordability challenges.”

GDP growth

GDP growth is slowing, with Austen Hufford of The Wall Street Journal (subscription required) reporting that GDP growth rose 1.1% annually in Q1 2023, a slowdown from the 2.6% growth seen in Q4 2022. The slowing growth adds to the above-noted fears of a short and shallow recession later this year.

Ben Casselman of the New York Times comments on the GDP data, noting that despite robust consumer spending, “[t]he Federal Reserve’s efforts to cool off the economy are having an effect. The housing sector shrank for the eighth consecutive quarter, and business investment in equipment fell for the second quarter in a row. Both areas are heavily influenced by interest rates, which policymakers have raised repeatedly over the past year to tamp down inflation.”

Source: New York Times (April 2023)

Jeff Cox of CNBC comments on consumer spending, reporting that the data shows that despite record inflation over the past year, people still want to spend money on things. Specifically, personal consumption expenditures jumped 3.7%, and exports were up 4.8%.

The Mortgage Bankers Association’s (MBA) VP and Deputy Chief Economist Joel Kan’s reacted to the GDP numbers:

“Continuing growth in the economy, coupled with a strong job market and inflation that is still too high – the first quarter PCE index showed 4 percent growth, double the Fed’s target – will likely lead the Fed to raise the Fed Funds Rate one more time at its next meeting, even as credit conditions tighten due to challenges and uncertainty in the banking sector. They are expected to then hold the funds rate at this higher level at least through the end of 2023. We forecast a short recession in the coming quarters, as these tighter financial conditions exert a drag on consumer and business activity through tighter lending conditions and higher rates. This will cause the unemployment rate to rise and gradually lower inflation closer to the Fed’s 2 percent target by the end of 2024.”

Housing profits

Lily Katz and Sheharyar Bokhari of Redfin report on investor profits, noting that according to their data, the average real estate investor lost money on 14% of the homes they sold in March. This is nearly the highest share seen since 2016. This is due to higher debt costs curbing demand for homes, and in pandemic boomtowns like Las Vegas and Phoenix, the percentage of sales losses for investors is almost double.

Source: Redfin (April 2023)

Redfin Senior Economist Sheharyar Bokhari comments on the data:

“You might wonder why investors don’t just wait to sell until the housing market bounces back. Many long-term investors who rent their properties out are doing that, but many flippers—especially those who bought recently—can’t afford to…Holding onto homes that aren’t producing income can be expensive because the owner is on the hook for property taxes, along with operating costs and monthly mortgage payments in some cases. Many short-term investors are also opting to sell because they know prices may have more room to fall and want to cut their losses.”

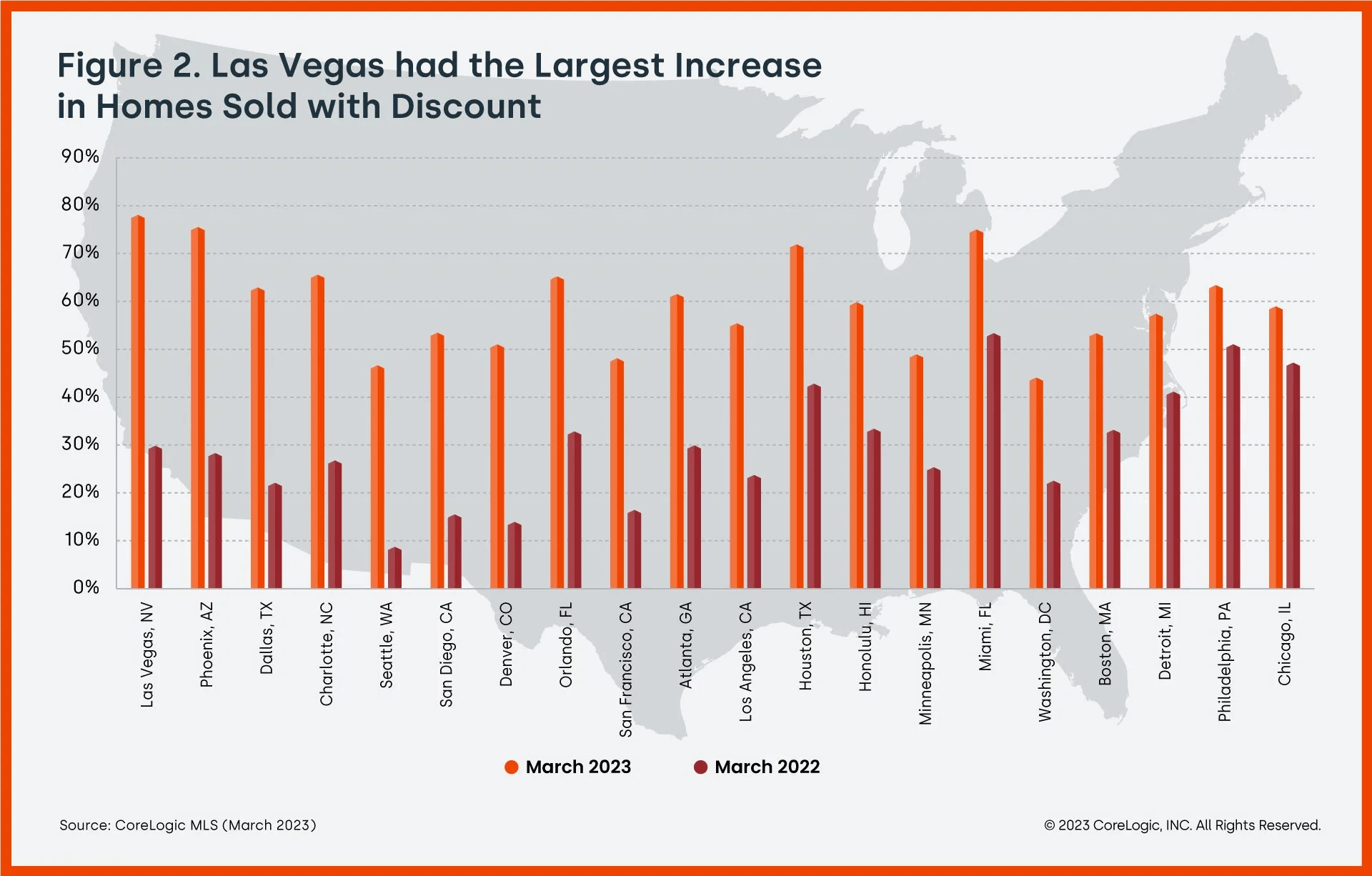

This reflects a broader market pullback on home prices, with Shu Chen of CoreLogic reporting that almost 60% of all U.S. homes sold were purchased below listing price. The overall softening of the resale market shows that favor is shifting to the buyers. This data is highly localized to some key markets like Las Vegas:

Source: CoreLogic (April 2023)

Finally, ATTOM Data Solutions came to similar conclusions after analyzing its data, finding that profit margins on median-priced homes decreased to 44.2%. This is the third straight quarterly decrease in home sale profit margins.

Source: ATTOM Data Solutions (April 2023)

Rob Barber, CEO of ATTOM notes:

“Homeowners are starting to take a significant hit in the form of lost profits from the recent market slowdown. Nine months of varying price declines around the country have carved away almost a quarter of the profit margin sellers were enjoying in early 2022. That’s a striking reversal of what we saw for a decade…It is possible that the upcoming peak buying season of 2023 could lead to increased profits, owing to favorable mortgage rates and other factors. Over the next few months, we can expect to gain more clarity regarding whether the current market stagnation is a short-term aberration or a more significant trend.”