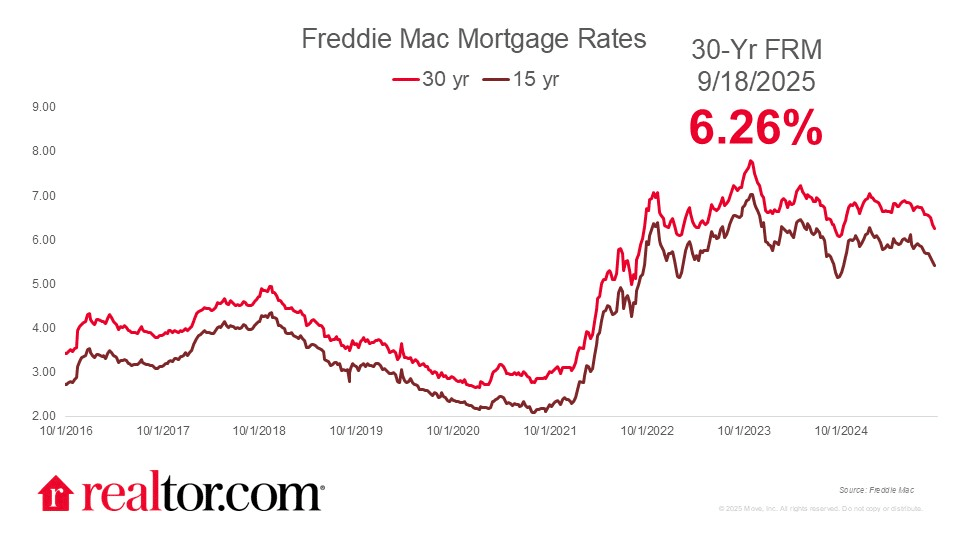

Jiayi Xu of Realtor.com reports that mortgage rates dipped to an 11-month low as the Freddie Mac 30-year fixed rate fell nine basis points to 6.26% following the Federal Reserve’s first rate cut since December 2024. The Fed lowered the federal funds rate by 25 basis points to a 4%–4.25% target range, citing rising employment risks and lingering tariff-related inflation uncertainty. Looking ahead, markets expect three more quarter-point cuts in 2025 and see rates dropping to 3% by mid-2026, while the Fed projects policy will stay slightly above 3% through 2028.

Source: Realtor.com (September 2025)

“Meanwhile, the current environment is opening refinancing opportunities for households that purchased at early highs, offering some affordability relief. At the same time, household real estate wealth has reached record levels, with elevated equity providing a meaningful cushion for both consumers and the wider economy. Affordability challenges persist as home prices remain elevated. Renting, however, has become a more budget-friendly option, with rents declining for more than two years and providing households with a wider range of affordable alternatives.”

Logan Mohtashami of HousingWire comments on the situation, noting that mortgage rates jumped 15 basis points after the Fed’s September meeting, with the 10-year Treasury yield climbing to 4.10%, despite the central bank’s quarter-point rate cut. The rise came as stronger-than-expected economic data (including retail sales and jobless claims) bolstered yields and offset dovish expectations. Mortgage spreads initially narrowed but quickly reversed following Fed Chair Jerome Powell’s press conference, which struck a less dovish tone than markets anticipated, fueling volatility and sending mortgage pricing higher instead of lower.

The Mortgage Bankers Association (MBA) reported that mortgage applications surged 29.7% for the week ending September 12, 2025, compared to the prior week, which had been adjusted for the Labor Day holiday. On an unadjusted basis, applications rose 43%. Refinancing drove much of the increase, with the Refinance Index jumping 58% week-over-week and 70% year-over-year. Purchase activity also strengthened, with the seasonally adjusted Purchase Index up 3% and the unadjusted index up 12% from the previous week, translating to a 20% gain from the same period in 2024.

Mike Fratantoni, MBA’s SVP and Chief Economist, comments: “Indicative of the weakening job market, and in anticipation of a rate cut from the Federal Reserve, mortgage rates last week dropped to their lowest level since last October, with the 30-year fixed rate declining to 6.39 percent. Homeowners responded swiftly, with refinance application volume jumping almost 60 percent compared to the prior week…Homeowners with larger loans jumped first, as the average loan size on refinances reached its highest level in the 35-year history of our survey. Almost 60 percent of applications were for refinances, but there was also a pickup in purchase applications.”

Home flipping

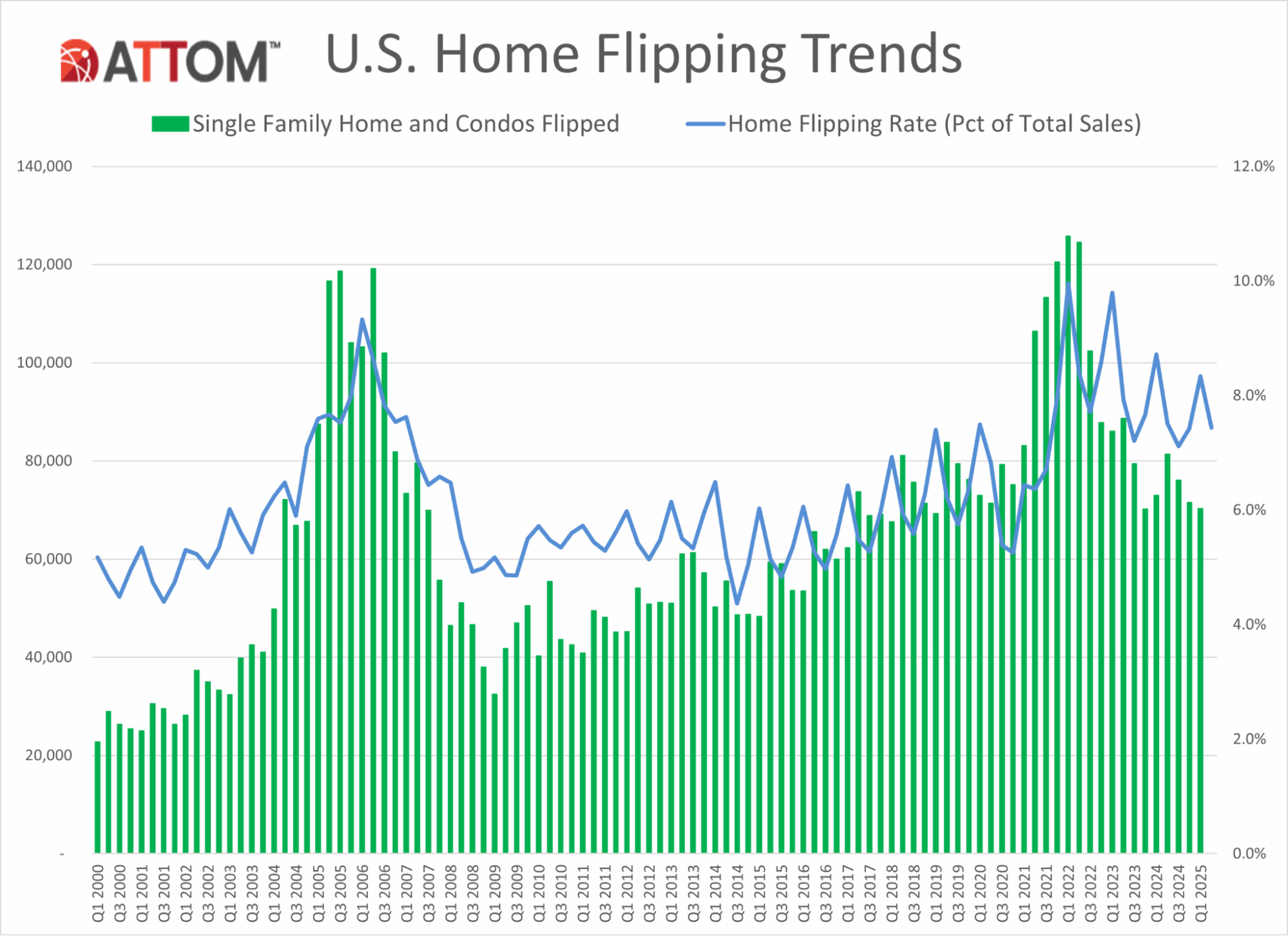

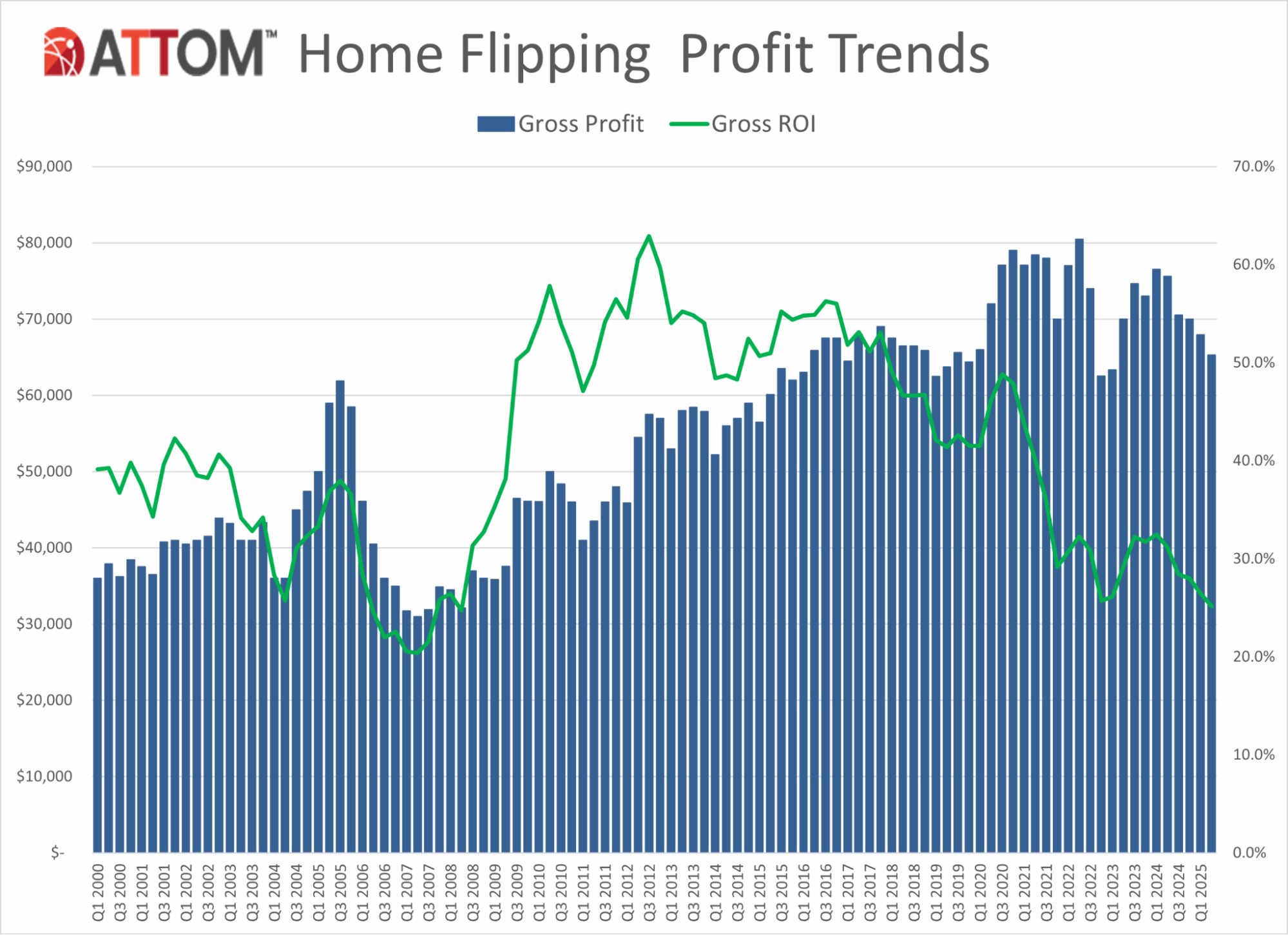

ATTOM Data Solutions reports that home flipping profits fell to a 17-year low in Q2 2025, with typical returns dropping to 25.1%, down from 62.9% in 2012 and the weakest margin since 2008. A total of 78,621 homes were flipped, making up 7.4% of all sales, slightly below both Q1 2025 (8.3%) and Q2 2024 (7.5%). Gross profits averaged $65,300, down 4% quarter-over-quarter and 13.6% year-over-year. Investors paid a median of $259,700 for flipped properties, the highest since tracking began in 2000, while the median resale price held steady at $325,000, squeezing margins despite elevated sales prices.

Source: ATTOM (September 2025)

In Q2 2025, 62.6% of flipped homes nationwide were purchased with all cash (flat from last year but slightly above Q1), highlighting investors’ reliance on liquidity. Cash flipping was most prevalent in Tuscaloosa, AL (85.3%), Youngstown, OH (82%), and Flint, MI (80.3%). The typical flip took 165 days from purchase to resale, up from 163 days in Q1. FHA-backed buyers made up 11.2% of flips, with the highest concentrations in California’s Central Valley and Florida’s Lakeland, where over 30% went to FHA buyers. Regionally, Georgia dominated the flipping landscape: 13 of the top 20 counties for flip share were in the state, led by Cobb (23.1%), Clayton (21.4%), and Douglas (20.5%), underscoring its role as the nation’s most active flipping market.

Source: ATTOM (September 2025)

Rob Barber, CEO at ATTOM, comments:

“We’re seeing very low profit margins from home flipping because of the historically high cost of homes…The initial buy-in for properties that are ideal for flipping, often lower priced homes that may need some work, keeps going up…As prospective homeowners get priced out of the middle and high end of the market, they’re more likely to be competing with flippers over the same homes.”

Housing starts

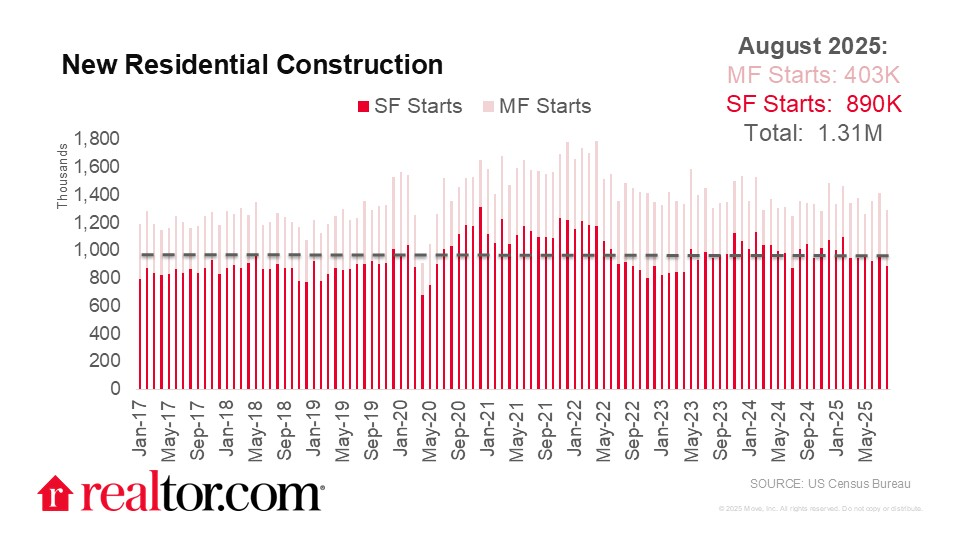

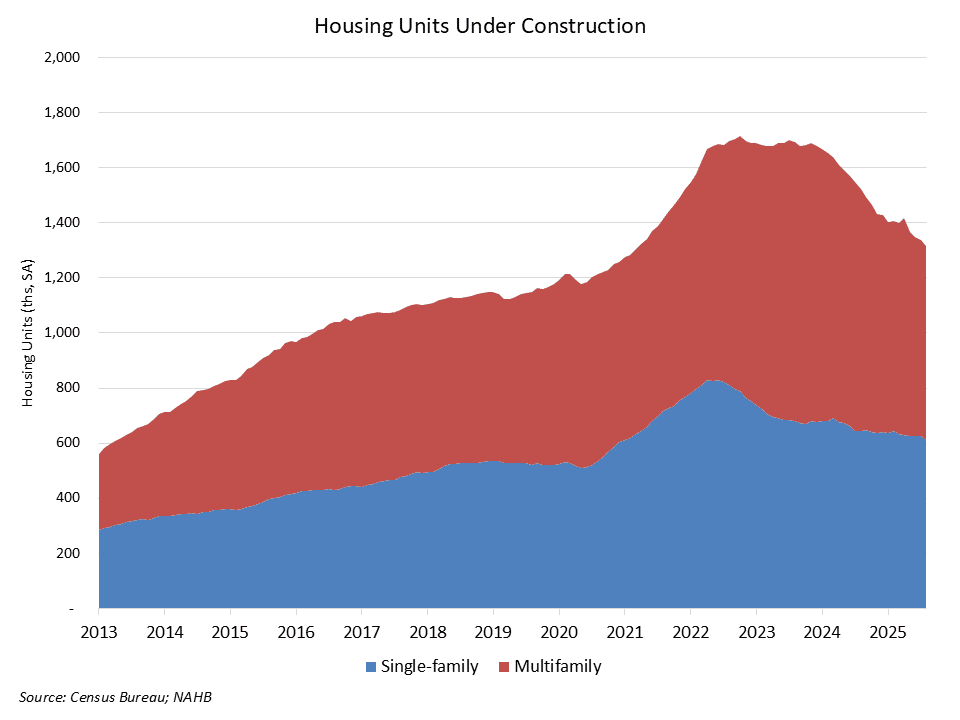

Orphe Divounguy of Zillow reports that housing starts fell sharply in August 2025, dropping 8.5% from July to a seasonally adjusted annual rate (SAAR) of 1.307 million, down 6% year-over-year. Building permits declined to 1.312 million (SAAR), 11.1% lower than a year earlier, while single-family starts slid to 890,000, down 11.7% annually. Weak sales, slowing price growth, and rising input costs dampen builder confidence, leaving many projects sidelined and unsold homes accumulating. The Midwest was the only region to see stable permitting, reflecting relative affordability, while nationally, the median new-home price per square foot fell 1.2% year-over-year in July.

Hannah Jones of Realtor.com highlights that August 2025 brought mixed signals for housing construction: while starts and permits declined, completions offered a modest bright spot. Single-family permits fell 2.2% from July and 11.5% year-over-year to 856,000 units, while multifamily permits slid 6.7% monthly and 10.8% annually, with only the West showing a rebound thanks to multifamily strength. Multifamily starts dropped 11% from July but climbed 15.8% from last year, contrasting with single-family starts, which slipped 7% monthly and 11.7% annually.

Source: Realtor.com (September 2025)

Completions rose 8.4% from July, with single-family completions up monthly (+6.7%) and annually (+5.6%). Multifamily completions surged 10.8% from July but remained nearly 29% below last year. Regionally, the Midwest stood out, with completions soaring 41.1% year-over-year. Builders, facing weak demand, tariffs, and labor issues, are leaning on incentives like mortgage rate buydowns to attract buyers, but slowing permits signal tighter supply ahead.

Robert Dietz of the National Association of Home Builders (NAHB) emphasizes that August 2025 marked the weakest pace of single-family homebuilding since July 2024. Multifamily construction also slumped to 417,000 units, though strength persisted in some exurban markets. Year-to-date, combined housing starts rose 15% in the Midwest and 8.3% in the Northeast but slipped in the South (–3.5%) and West (–0.1%). Permits mirrored the slowdown, with year-to-date single-family permits down 7% and multifamily off 6.4%.

Source: NAHB (September 2025)

Finally, Elizabeth Thompson, also of NAHB, reports that builder confidence in August 2025 slipped to 32 on the NAHB/Wells Fargo Housing Market Index, marking the 16th straight month in negative territory and continuing its narrow range between 32 and 34 since May. Affordability challenges remain the top drag, with 37% of builders cutting prices (averaging 5%) and sales incentives rising to 66%, the highest share in the post-COVID period. The index measuring current sales conditions fell to 35, sales expectations held at 43, and buyer traffic ticked up to 22 but stayed weak. Regionally, confidence edged up in the Midwest (42) but slipped in the Northeast (44), South (29), and West (24), underscoring broad caution amid high mortgage rates and regulatory hurdles.