Megan Hunt of ATTOM Data Solutions reports that U.S. foreclosure activity in August 2025 totaled 35,697 filings, down 1.1% from July but up 18.1% year-over-year. This means 1 in every 3,987 housing units faced foreclosure. Starts reached 24,254 (down 0.2% MoM, up 16.9% YoY), while completed repossessions rose to 4,077 (up 5% MoM, up 41% YoY). Nevada overtook South Carolina and Florida for the highest foreclosure rates, highlighting regional stress tied to affordability and lending conditions. While month-to-month activity dipped slightly, the strong annual rise points to continued upward pressure heading into late 2025.

ATTOM Data Solutions also reports that foreclosure activity rose for the sixth straight month. Metro-level stress was most pronounced in Lakeland, FL (1 in every 1,212 housing units), Columbia, SC (1 in 1,347), Chico, CA (1 in 1,545), Cleveland, OH (1 in 1,755), and Ocala, FL (1 in 1,816). Among larger metros, Cleveland led, followed by Las Vegas (1 in 1,817), Jacksonville (1 in 2,057), Houston (1 in 2,195), and Orlando (1 in 2,210). Foreclosure starts totaled 24,254 (up 16.9% YoY) with the highest volumes in New York (1,431), Houston (1,178), Chicago (1,009), Los Angeles (862), and Miami (748), underscoring regional pressures from high costs and interest rates.

Neil Pierson of HousingWire reports that homeowners remain well cushioned by equity even as price appreciation cools, with the average mortgage holder holding about $307,000 and total national equity standing at $17.5 trillion in Q2 2025. While equity levels slipped roughly $9,200 per homeowner over the past year, this still marks one of the strongest cushions in history and provides a buffer against rising foreclosure activity, which has increased year-over-year for six straight months. The divergence highlights a split market: strong equity for most owners, but mounting distress in certain regions where affordability and high rates are driving foreclosures higher.

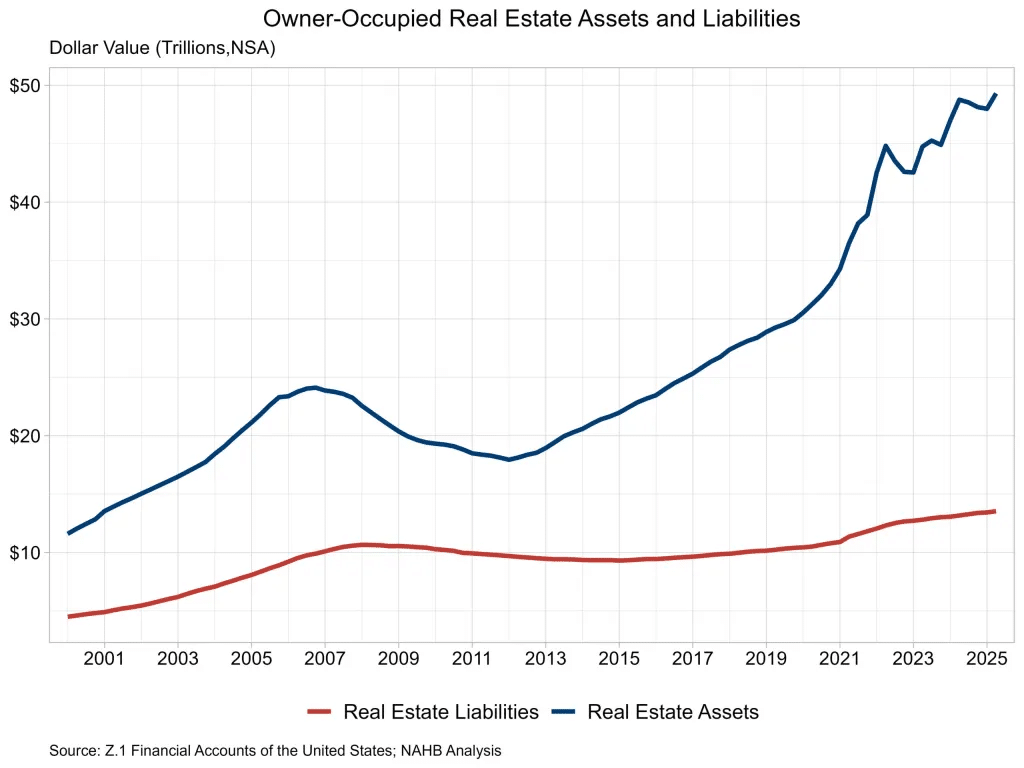

Indeed, Jesse Wade of the National Association of Home Builders (NAHB) reports that the market value of U.S. household real estate assets climbed to a record $49.3 trillion in Q2 2025, up 2.7% from Q1 and 1.1% year-over-year. Real estate liabilities also grew to $13.5 trillion, leaving owners’ equity at $35.8 trillion, or 72.6% of total assets—the longest stretch above 70% since the 1950s. While this rising wealth and historically strong equity buffer most households, it contrasts with the uptick in foreclosure activity across certain regions, where affordability pressures and high interest rates expose more vulnerable borrowers despite record-high national housing wealth.

Source: NAHB (September 2025)

Teresa Mettela or Realtor.com reports that affordability remains a key driver for foreclosures. Since August 2019, median list prices are up 36.1% and price per square foot 51.3%, even as August’s median price of $429,990 held flat YoY. High interest rates, rising insurance costs, and adjustable-rate mortgage resets are straining homeowners, particularly in markets like Florida, where overlapping cost pressures are accelerating distressed sales and listings.

Fannie and Freddie

Joseph Zeballos-Roig of Quartz reports that Commerce Secretary Howard Lutnick signaled Fannie Mae and Freddie Mac could reopen to investors by late 2025, potentially through a $30 billion IPO that might be the largest in history. The plan, still under federal control since their 2008 bailout, would allow limited shareholder stakes (about 5%) while the government retains ownership. Lutnick emphasized affordability as a priority, while FHFA Director Bill Pulte noted the administration is preparing for a public offering, even rehiring staff to ready the housing giants, which collectively underpin a vast share of the U.S. mortgage market.

Max Gottlich of Seeking Alpha reports on the announcement, commenting that shares went up sharply (Fannie by 8% and Freddie by 8.9%). Lutnick emphasized that the IPO would highlight the massive taxpayer-owned assets, stressing that the government doesn’t plan to “sell a lot” but sees strong merit in taking the mortgage giants public.

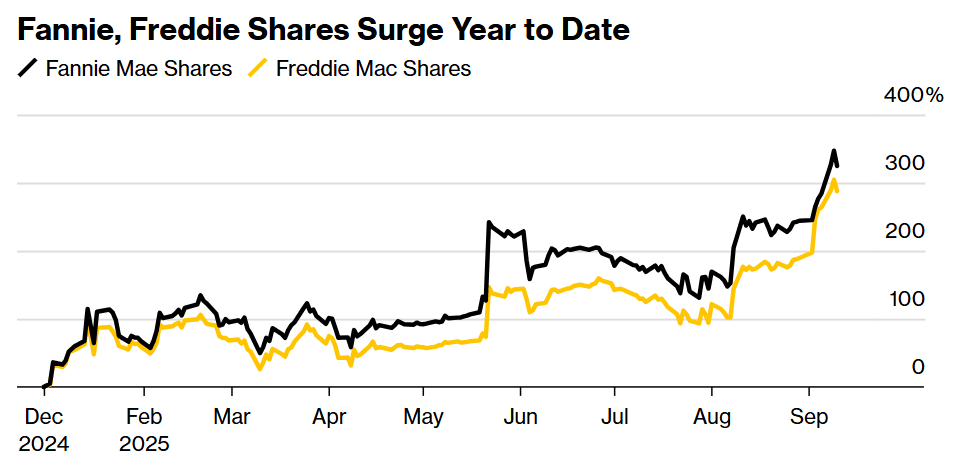

Georgie McKay of Bloomberg reports that Deutsche Bank became the first Wall Street firm to issue buy ratings on Fannie Mae and Freddie Mac, projecting further gains as the mortgage giants edge toward a potential release from government control. Fannie shares have soared 320% year-to-date and Freddie 288%, with Deutsche Bank setting price targets of $20 and $25, respectively, well above current OTC levels. Analyst Mark DeVries noted significant upside but warned that recapitalization could bring heavy dilution, making the stocks risky for conservative investors.

Source: Bloomberg (September 2025)

Finally, The Economist notes that investors have already seen over 2,000% gains betting on a release. Still, the Fannie and Freddie hold more than $7 trillion in mortgage debt and face capital shortfalls of $188 billion (Fannie) and $139 billion (Freddie) to meet regulatory requirements. The Treasury also holds $355 billion in liquidation preferences after injecting $193 billion, raising thorny questions of how much value taxpayers should recoup versus what investors argue should be forgiven. Ultimately, any path forward must balance recapitalization, shareholder rights, and the government’s role in housing policy, making this $7 trillion question far from straightforward.