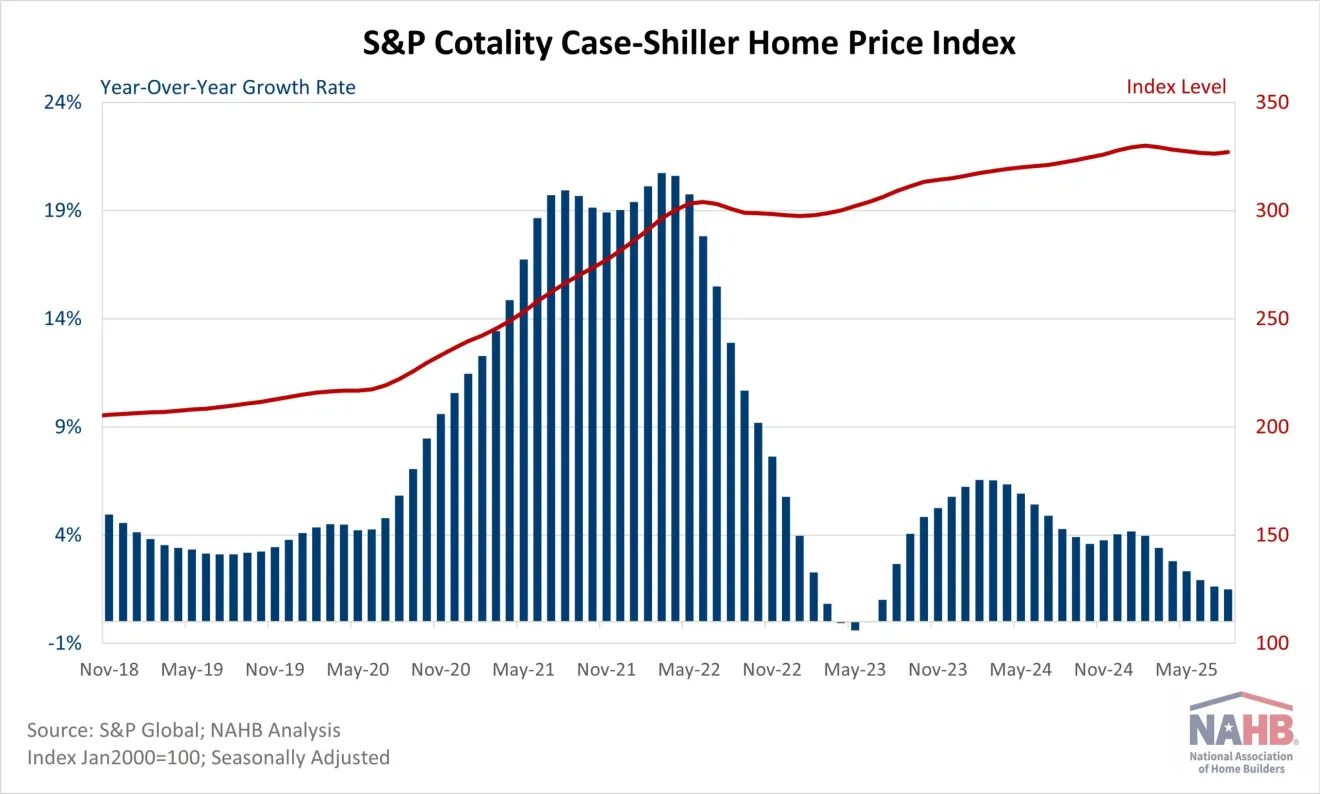

Onnah Dereski of the National Association of Home Builders (NAHB) reports that home prices grew at their slowest annual rate in over two years, with an increase of just 1.51% in August, nearly half the rate of inflation. This marks a sharp decline from the 6.5% growth seen in early 2024. While the index posted a modest monthly increase in August after five months of decline, 11 of the 20 major metro areas tracked saw home price increases. Notably, New York led with a 6.08% increase, followed by Chicago at 5.89% and Cleveland at 4.67%. In contrast, Tampa experienced the steepest drop at -3.34%, with Miami also seeing a decline of -1.69%.

Source: NAHB (November 2025)

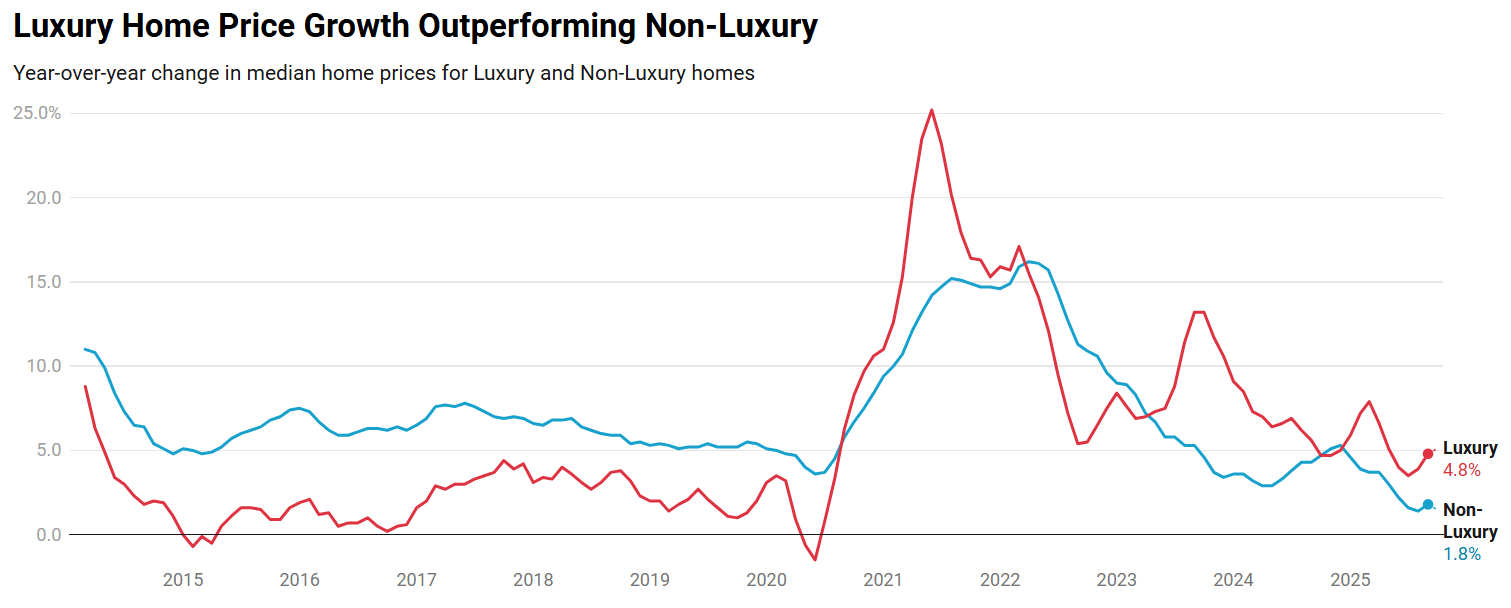

Mark Worley of Redfin reports that luxury home prices rose 4.8% year-over-year in September 2025, reaching a record high of $1.26 million, more than twice the 1.8% growth seen in non-luxury homes, which had a median price of $371,583. Luxury home sales were flat, showing signs of stabilization after a sharp slowdown last year, while non-luxury sales fell 0.3%, nearing their lowest level since 2013. Luxury homes took 52 days to sell, six days slower than the previous year, while non-luxury homes took 43 days, seven days longer. The highest price increase in luxury homes was observed in West Palm Beach, FL (+14.8%), while Tampa, FL experienced the most significant decline (-3.3%).

Source: Redfin (November 2025)

Redfin Senior Economist Sheharyar Bokhari comments:

“Luxury prices are outpacing the rest of the market because the people buying at the top end are playing by different rules…They’re not waiting for rates to drop or prices to fall—they have the cash, stock gains, and long-term confidence to act when they see a home they want. Some high-end buyers are also using real estate as a safe place to park their money amid economic uncertainty. That demand, even at a smaller scale, is enough to keep pushing luxury prices up faster than the broader market.”

Zillow’s October 2025 forecast predicts home values will remain flat in 2025, before recovering and growing at nearly 1.9% by August 2026. Home sales are expected to end the year at 4.07 million, a slight increase of 0.3% from 2024, but still reflecting weak momentum and slightly lower than the previous forecast of 4.1 million. New listings are projected to outpace sales, aiding inventory recovery after the pandemic’s impact.

Brooklee Han of HousingWire reports that pending home sales remained flat in September 2025, with the National Association of Realtors’ Pending Home Sales Index holding steady at 74.8. Despite low mortgage rates, affordability challenges and economic uncertainty hindered growth. Regional variations showed gains in the South and Northeast, while the Midwest and West saw declines. NAR’s chief economist, Lawrence Yun, noted that while contract signings matched the second-strongest pace of the year, they have not yet reached the levels needed for a healthy market, with stock market gains and rising housing wealth unable to offset a potentially softening job market.

Rents

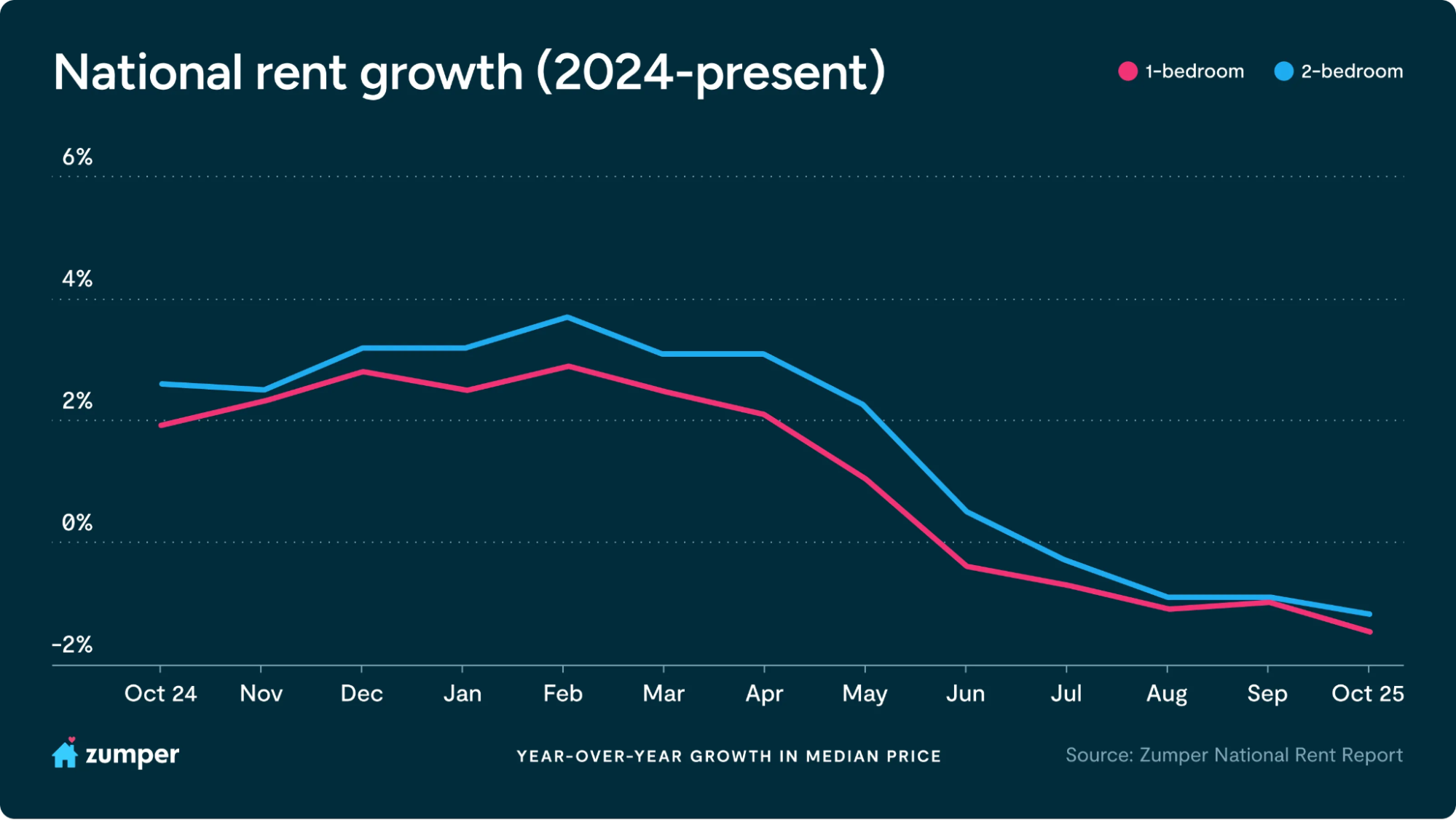

Crystal Chen and Quentin Proctor report in Zumper’s National Rent Index for October 2025 that rental rates have remained flat or declined for the fourth consecutive month. One-bedroom median rent decreased 0.4% to $1,511, while two-bedroom rents fell 0.3% to $1,888. Year-over-year, one-bedroom rents are down 1.5% and two-bedrooms 1.2%. San Francisco saw the steepest annual increase, with two-bedroom rents rising 17.6%, the highest recorded in the city since Zumper began tracking rents a decade ago. In contrast, New York City rents declined monthly and annually for the first time since spring 2021, driven by drops in The Bronx and Brooklyn.

Source: Zumper (November 2025)

Zumper CEO Anthemos Georgiades comments:

“With the rental market now entering the seasonally slower months, a clearer picture of the sector’s trajectory may not emerge until the spring leasing season begins…Until then, the interplay between abundant supply, cautious consumer behavior, and economic uncertainty will continue to define market conditions.”

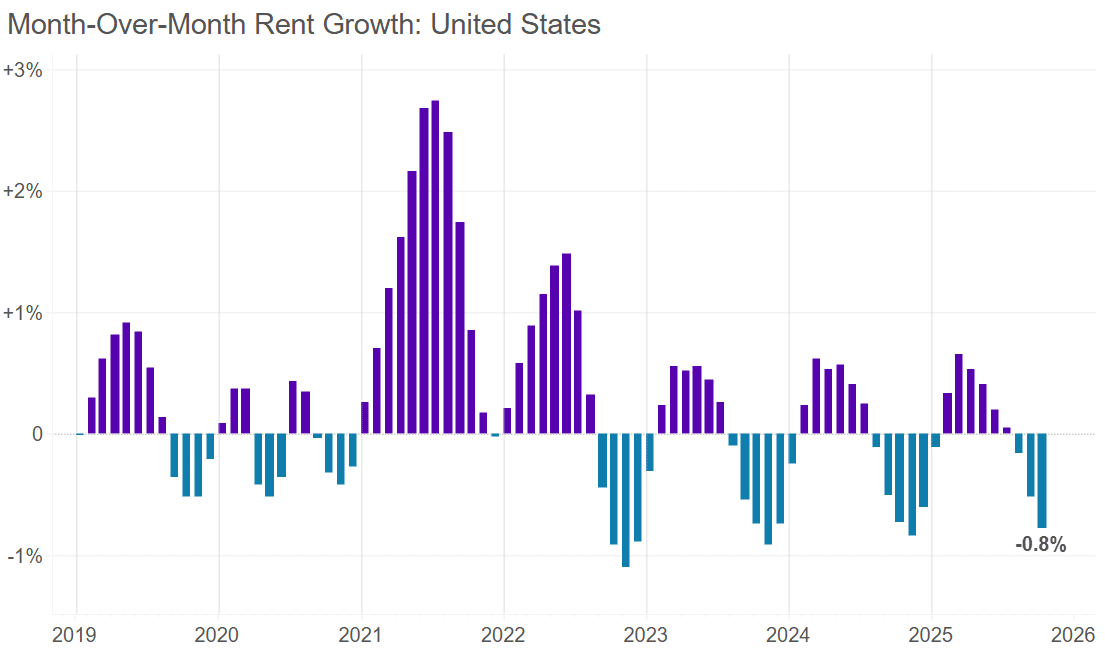

The Apartment List Research Team reports that the national median rent declined by 0.8% in October 2025, marking the third consecutive month of decreases, now standing at $1,381. Rent prices are down 0.9% year-over-year, continuing a trend of slight negative growth for over two years, with the national median rent having fallen 4.2% from its 2022 peak. The national multifamily vacancy rate rose to 7.2%, a new record high, as new units continue to hit the market amidst sluggish demand. Units are taking an average of 33 days to lease, one day longer than last month. The Austin metro has seen the sharpest rent decline, with a 6.5% decrease over the past year, while Providence, RI, leads in year-over-year rent growth at 5.3%.

Source: Apartment List (November 2025)

Manny Garcia reports that Zillow’s 2025 Consumer Housing Trends study, based on six nationally representative surveys and data from over 24,400 renters, reveals key shifts in renter behavior and preferences. Among recent movers, 58% received advertised concessions, 25% successfully negotiated them, and reduced rent ranked as the most valued perk (27%). Digital marketing matters: 57% of recent renters considered at least one modern media feature essential, including virtual staging (33%) and 3D common-area tours (29%). Most renters (75% overall) do not have a lease cosigner, although parents are the most common type of cosigner when one is present.

Fed comments

Jessica Dickler of CNBC reports that the Federal Reserve cut interest rates by 25 basis points on October 29, 2025, bringing the federal funds rate to 3.75%-4.00%. This move is expected to impact borrowing and savings rates across various consumer products, including credit cards, mortgages, auto loans, and savings accounts. While credit card interest rates, currently averaging over 20%, may decrease as a result, they will remain high. The rate cut is seen as a potential relief for consumers facing high borrowing costs, particularly those borrowing to supplement their income. However, the effect on longer-term rates will depend on inflation and other economic factors.

Maria Volkova of NMN reports that the Fed’s rate cut, while expected, sparked uncertainty about future actions. Chair Jerome Powell’s comments indicated that the likelihood of another rate cut in December is unclear, with differing opinions within the Fed on the matter. Powell noted that a further reduction in December is “far from” certain, with labor market data—yet to be released due to the government shutdown—playing a crucial role in influencing the decision. Additionally, the Fed plans to end its quantitative tightening program in December.

Flávia Furlan Nunes of HousingWire reports that the Fed’s cut has brought the benchmark interest rate to its lowest level in three years, potentially lowering mortgage rates further. Economists expect another rate cut in December, which, along with a shift in the Fed’s balance sheet strategy, could further ease mortgage rates and improve housing affordability, thereby boosting demand. Mortgage rates are already at their lowest levels of the year, offering relief to homebuyers.

Kara Ng of Zillow reports that Fed Chairman Jerome Powell emphasized that a December cut, previously expected by the market, is not guaranteed. Powell noted that the Fed is relying more on alternative data due to the absence of major government data releases. Still, no significant shifts in the labor market have been detected. As a result, Treasury yields rose, potentially putting upward pressure on mortgage rates. While mortgage rates have dropped recently, Zillow expects them to remain within the 6%-7% range in 2026, balancing risks from inflation and the labor market.

Finally, Keith Griffith of Realtor.com reports that Powell’s comments afterward surprised markets and are expected to push mortgage rates higher. Powell stated that a December rate cut is “far from” certain, citing strong divisions within the Fed’s policy-setting committee. His remarks led to a surge in the 10-year Treasury yield above 4%, signaling higher mortgage rates. While Freddie Mac reported a slight dip in mortgage rates to 6.17%, daily tracking showed rates rising above 6.3% following Powell’s comments. The market reacted to Powell’s unexpected emphasis on economic factors that could delay further rate cuts, as well as the unprecedented dissents within the Fed on the direction of policy.