Joel Berner of Realtor.com reports that the S&P Cotality Case-Shiller U.S. National Home Price NSA Index showed modestly firmer price growth in October, with prices up 1.4% YoY (vs. 1.3% the prior month), reflecting closings primarily from August–October when mortgage rates eased in early fall but affordability and “rate lock-in” kept turnover low. Regional gaps remain wide, with metro results ranging from +5.8% YoY in Chicago to -4.2% in Tampa. Tighter supply supports faster gains in the Northeast/Midwest, while more plentiful inventory and longer days-on-market weigh on the South/West.

Source: Realtor.com (January 2026)

Looking ahead to early 2026, Berner expects mortgage rates to remain near current levels, providing only incremental relief to affordability. National price growth is expected to continue decelerating, with local inventory conditions driving outcomes. Supply-constrained markets are expected to remain firmer, while areas with rebuilding inventory and new construction competition will continue to face price pressure.

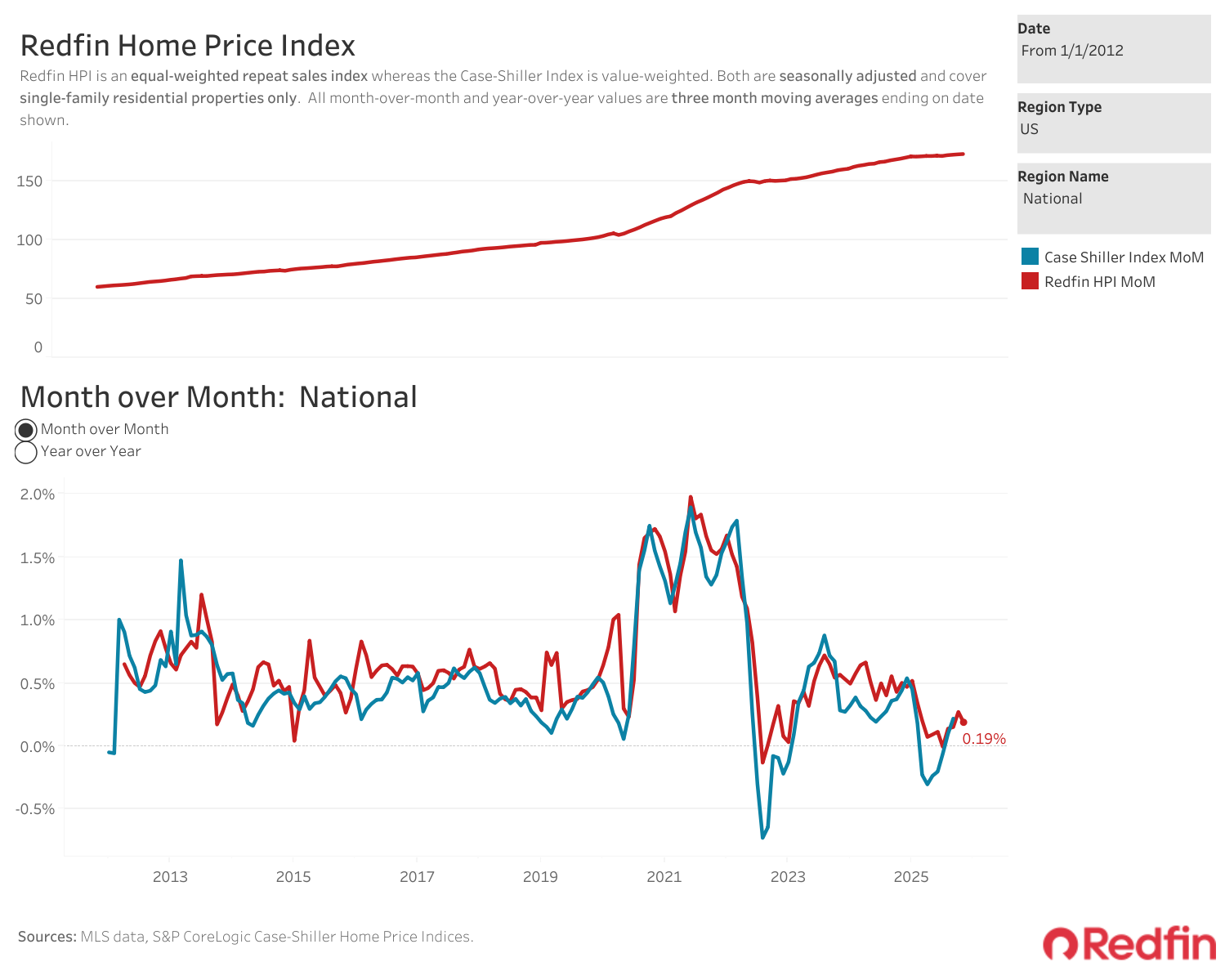

Dana Anderson of Redfin reports that home prices rose 0.2% month over month in November (seasonally adjusted), while annual growth slowed to +2.6% YoY (down from +2.9% in October), the slowest pace in Redfin’s records back to 2012. Prices fell MoM in 11 major metros, led by Charlotte (-0.9%), Austin (-0.6%), and Cincinnati (-0.6%), while standouts on the upside included Pittsburgh (+2.3%), Montgomery County, PA (+1.6%), and Chicago (+1.3%). YoY, gains were most substantial in Chicago (+11%), Pittsburgh (+10.1%), and New York (+9.5%), while the most significant drops were in Austin (-3.8%), Dallas (-2.8%), and Oakland (-2.5%).

Source: Redfin (January 2026)

Chen Zhao, Redfin’s head of economics research, comments:

“Home-price growth is cooling as the calendar turns to winter, but prices are still rising and they’re still too high for many house hunters…Still, we’re in the midst of the strongest buyer’s market in a decade; even though prices remain high, buyers have a chance to negotiate with sellers and get some concessions. The other bright spot for buyers: We expect wages to grow faster than home prices in 2026, improving affordability and perhaps thawing the housing market.”

Diana Olick of CNBC reports that housing affordability is improving as mortgage rates fall and supply rises, but down payments remain the most significant barrier (Realtor.com estimates the typical buyer now needs 7 years to save one). The 30-year fixed rate is ~6.19% (down from 7%+ earlier this year), and active listings are ~12% higher YoY, while prices are essentially flat: Parcl Labs shows national prices just +0.3% YoY. Case-Shiller highlights significant metro gaps (e.g., more substantial gains in Chicago/New York/Cleveland vs. notable declines in Tampa/Phoenix/Dallas), and S&P notes home-price growth is running below an estimated ~3.1% CPI. This implies slightly softer inflation-adjusted values; for a $410K home with 20% down, the monthly payment is about $200 less than a year ago.

2026 outlook

Logan Mohtashami of HousingWire forecasts a steadier, more “normal” 2026 housing market, arguing that active inventory has returned to near-normal levels and home-price growth has cooled, putting buyers and sellers on firmer ground than the overheated period from 2020 through early 2022. He frames the year around a clear rate threshold: housing data tends to improve when mortgage rates fall below 6.64% and move toward 6%, but demand and activity tend to fade when rates are above 6.64% (especially over 7%). With price growth no longer “out of control” and supply healthier, he suggests watching the “slow dance” of the 10-year Treasury yield as the primary signal for how housing will trend through 2026.

Daniella Genovese of Fox Business reports that while the housing market is inching in a better direction, 2026 is unlikely to deliver meaningful relief for most buyers: expect mortgage rates to dip only slightly to about 6.3% (from an average 6.6% in 2025), translating to just a ~1.3% drop in housing payments. Genovese notes that a significant “lock-in” effect remains, with approximately 52.5% of mortgages under 4%, 70% under 5%, and 80% at 6%. This will keep many owners from selling and limit supply despite improving inventory in some regions.

Nationally, projections are that home prices will be roughly similar to 2025, rising about 2% in 2026. Still, with a sharp regional split: inventory is as much as 50% above pre-pandemic levels in the South and West (adding downward pressure as new construction comes online). In comparison, the Midwest and Northeast remain 30%–50% below pre-pandemic inventory.

Sami Sparber of Axios writes that 2026 should bring slightly lower mortgage rates but not a dramatically easier housing market, with economists expecting 30-year fixed rates to average around 6.3% (down from 6.6% in 2025) while affordability and the “lock-in” effect persist. Forecasts call for a modest rebound in activity (existing-home sales +1.7% (Realtor.com) to +3% (Redfin)) and home prices up ~1% in 2026, even as wages are expected to rise faster than prices.

Sparber also highlights a widening regional split: Top markets lists are now dominated by the Northeast/Midwest (led by Hartford, Rochester, Worcester), where prices are expected to rise ~3–4% on tight inventory, while the South/West see softer pricing amid slower migration and higher insurance costs.

Sarah Sharkey of MSN reports that some agents expect home prices to dip in 2026 in eight markets: Austin, Boise, Raleigh, Cape Coral, Tampa, Phoenix, Seattle, and Los Angeles. This is mainly because pandemic-era demand has cooled while new construction and rising inventory are giving buyers more leverage (especially in places like Austin/Boise/Raleigh). The piece also points to region-specific pressures: Florida markets face hurricane/insurance-cost blowback (Cape Coral, Tampa), Phoenix is flagged for high prices and dulled buyer demand in a higher-rate world, Seattle for softening demand tied to slower growth, and Los Angeles for cost-of-living strain that could push more would-be buyers and residents to look elsewhere.

Dave Gallagher of Real Estate News says 2026 could be a “normalizing” year for sales and inventory, while the industry’s rules of the game remain chaotic. Here are a few key points:

- The Sitzer/Burnett and Gibson commission settlements (including a ~$1B seller settlement fund) face appeals in the 8th Circuit, with oral arguments set for Jan. 14, 2026, and a decision expected later this year (an overturn would force brokerages/MLSs back into uncertainty).

- Faster MLS fragmentation and consolidation are expected as NAR shifts toward advocacy, noting that there are over 500 MLSs and looser standardization could confuse consumers.

- Increase in the “lifestyle renter” trend, with only 37% of renters saying they’d buy even if rates dropped (down from 45% a year earlier), nearly 60% plan to keep renting in 2026, and apartment rents are expected to rise just 0.3%

- Pre-midterm policy action on affordability, but doesn’t expect actual cost “normalcy” until 2030.

Trump housing reforms?

Samantha Delouya of CNN reports that the Trump administration is signaling “aggressive” housing reforms aimed at improving affordability in 2026, but economists say the impact may be limited because the specifics are still unclear. The market’s direction will likely hinge more on rates, inventory, and jobs than on Washington policy. Even with that policy push, the backdrop is steep with home prices rising nearly 55% from early 2020 to Q3 2025. Compass economist Mike Simonsen expects prices to remain essentially flat in 2026 (approximately +0.5%), with more meaningful relief potentially resulting from increased homebuilding and a decline in mortgage rates (recently at 6.18% for a 30-year fixed).

Terry Lane of Investopedia reports on the subject, noting that President Trump is promising “aggressive” housing reforms in 2026, with ideas on the table including declaring a national housing emergency, exploring 50-year mortgages, and using federal action to cut closing costs, standardize local building codes, and potentially lower tariffs on building materials. This, while also arguing that immigration enforcement could ease demand pressure. Bipartisan momentum in Congress (the Housing for the 21st Century Act) could also push reforms aimed at speeding approvals and increasing housing supply.

Keith Griffith of Realtor.com writes that a core tension in Trump’s housing agenda is political and economic. In a Dec. 18 Oval Office remark, Trump openly said boosting affordability for buyers can conflict with his goal of keeping existing homeowners “wealthy and happy” by avoiding any meaningful drop in home values, especially for older homeowners sitting on record equity. Griffith argues that this helps explain why Trump leans so heavily on lower mortgage rates as the fix (because it can help buyers without directly cutting prices), even though presidents don’t control mortgage rates and supply-driven affordability would, by basic economics, pressure prices for both new and existing homes. Griffith notes that even a drastic rate drop wouldn’t fully restore affordability at today’s prices, and that at current wage-growth trends, it could take 11 years to return to pre-pandemic affordability.

SeekingAlpha argues that Trump’s most market-moving idea is portable mortgages (letting homeowners transfer their existing low-rate loans to a new home), which could “unfreeze” turnover by removing the penalty of giving up 3%-era mortgages, but would likely complicate mortgage-backed securities and could push rates higher as lenders reprice that risk. The piece also flags other levers the plan may lean on (deregulation to expand manufactured housing, streamlined permitting via the Housing for the 21st Century Act, and modernizing FHA loan limits) and frames the bet as a broad “housing-thaw” trade for housing-linked sectors (appliances, home improvement, builders) if these policies actually boost transaction volume rather than just re-inflate prices.