Last Updated on March 11, 2026

Mary Cunningham of CBS News reports that the U.S. housing market is feeling the ripple effects of the war in Iran, with 30-year fixed mortgage rates ticking up to 6%, a slight increase from 5.98% the prior week, which had been the lowest point since September 2022. The uptick is being driven by rising global oil prices, which are fueling inflation fears and pushing bond yields higher as investors seek higher returns. While 0.2 percentage points won’t make or break a home purchase, the psychological weight of crossing the 6% threshold feels significant to buyers.

Dave Gallagher of Real Estate News explores two possible paths the war in Iran could take for the U.S. housing market as the traditionally busy spring season gets underway. The 30-year fixed rate jumped to 6.13% on March 3 after dipping below 6% the week prior, and Bright MLS Chief Economist Lisa Sturtevant warned that a prolonged conflict could keep rates elevated by sustaining higher energy prices and inflation, while a shorter one might only temporarily delay the buying season. Before the war began, conditions were actually looking up: price growth had slowed, inventory was improving, and rates had hit their lowest since September 2022.

Rachel Clun of the BBC reports that major UK lenders are already raising mortgage rates in response to the Iran conflict, with Nationwide hiking some products by up to 0.25%, and HSBC UK and Coventry Building Society following suit. The increases are being driven by a jump in swap rates, which reflect the market’s expectations for Bank of England interest rate decisions. Average UK fixed rates now sit at 4.84% for a two-year deal and 4.96% for a five-year.

Keith Griffith of Realtor.com digs into the oil market mechanics fueling rate concerns, noting that Brent crude surged more than 8% to nearly $79 per barrel as the bombing campaign entered its third day, with the Strait of Hormuz, which handles roughly 20% of global crude shipments, emerging as a major vulnerability. The 10-year Treasury yield jumped 9 basis points back above 4%, signaling that inflation fears are overpowering the typical flight-to-safety effect, while homebuilder stocks slid more than 2% as investors priced in the risk of prolonged higher rates. CME FedWatch data shows markets now see a 53% chance the Fed holds rates steady through June, up from 43% before the strikes, potentially pushing any relief out to July.

Kara Ng of Zillow comments: “Both bond yields and mortgage rates spiked higher this week. While geopolitical risks can send investors toward safe assets like bonds, driving yields down, rising oil prices raise concerns about higher inflation, which sends yields up. Notably, the 30-year fixed mortgage rate, which had dipped below the 6% threshold, has moved back above it.”

Chen Zhao, Redfin’s head of economics research, also provides commentary:

“Last week, Americans were hit with headlines about mortgage rates dropping below 6%, which provided some hope. But over the weekend, those headlines were replaced with ones about the war in the Middle East…The war could make some would-be buyers think twice, much in the same way economic and global uncertainty have been turning off buyers for the last year, and it’s likely to cause short-term volatility in mortgage rates. But the war’s impact on the economy will mostly be felt in oil markets, which are unlikely to have a big impact on mortgage rates or demand unless the conflict goes on much longer than expected.”

Cushman & Wakefield’s analysis argues that commercial real estate is largely insulated from the Iran conflict, since geopolitical shocks tend to hit CRE indirectly through financial markets rather than through direct changes in space demand. The biggest risk channel would be sustained higher energy prices pushing inflation up and delaying expected rate cuts, which could tighten financial conditions and weigh on investment activity. Notably, public REITs were trading slightly better than broader market indexes on the day, suggesting investors see liquid real assets as a modest safe haven rather than assigning outsized risk to CRE fundamentals.

Jobs data

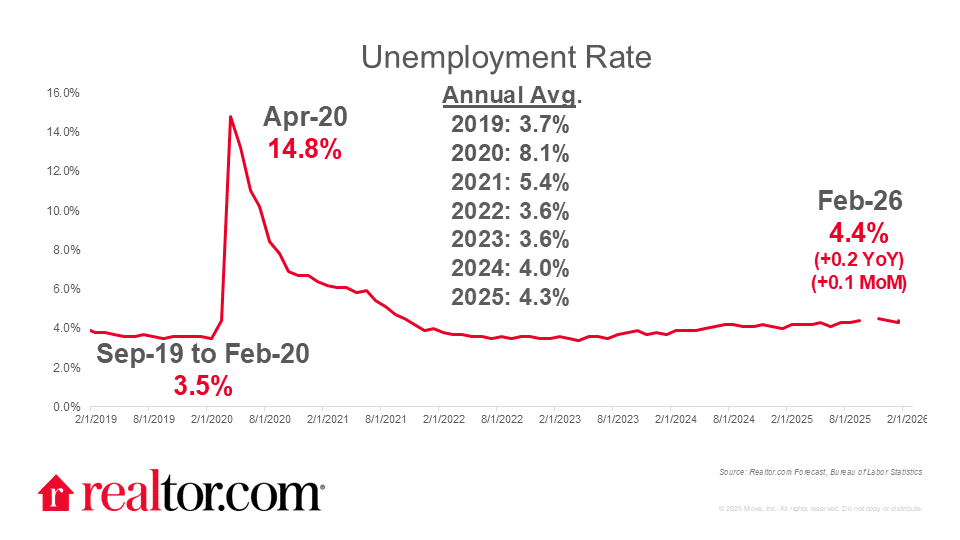

Jake Krimmel of Realtor.com breaks down a “soft surprise” February jobs report, with nonfarm payrolls dropping by 92,000 and unemployment ticking up to 4.4%. That followed a revised January gain of 126,000 and a 65,000-job downward revision to December, painting a messier picture than last month’s headline suggested. Krimmel argues that neither month should be taken in isolation, noting that the “low-hire, low-fire” job market dynamic remains intact. The takeaway for housing: the labor market is volatile but not collapsing, and the first two months of 2026 suggest cautious optimism for the spring season remains reasonable despite the bumpy start.

Source: Realtor.com (March 2026)

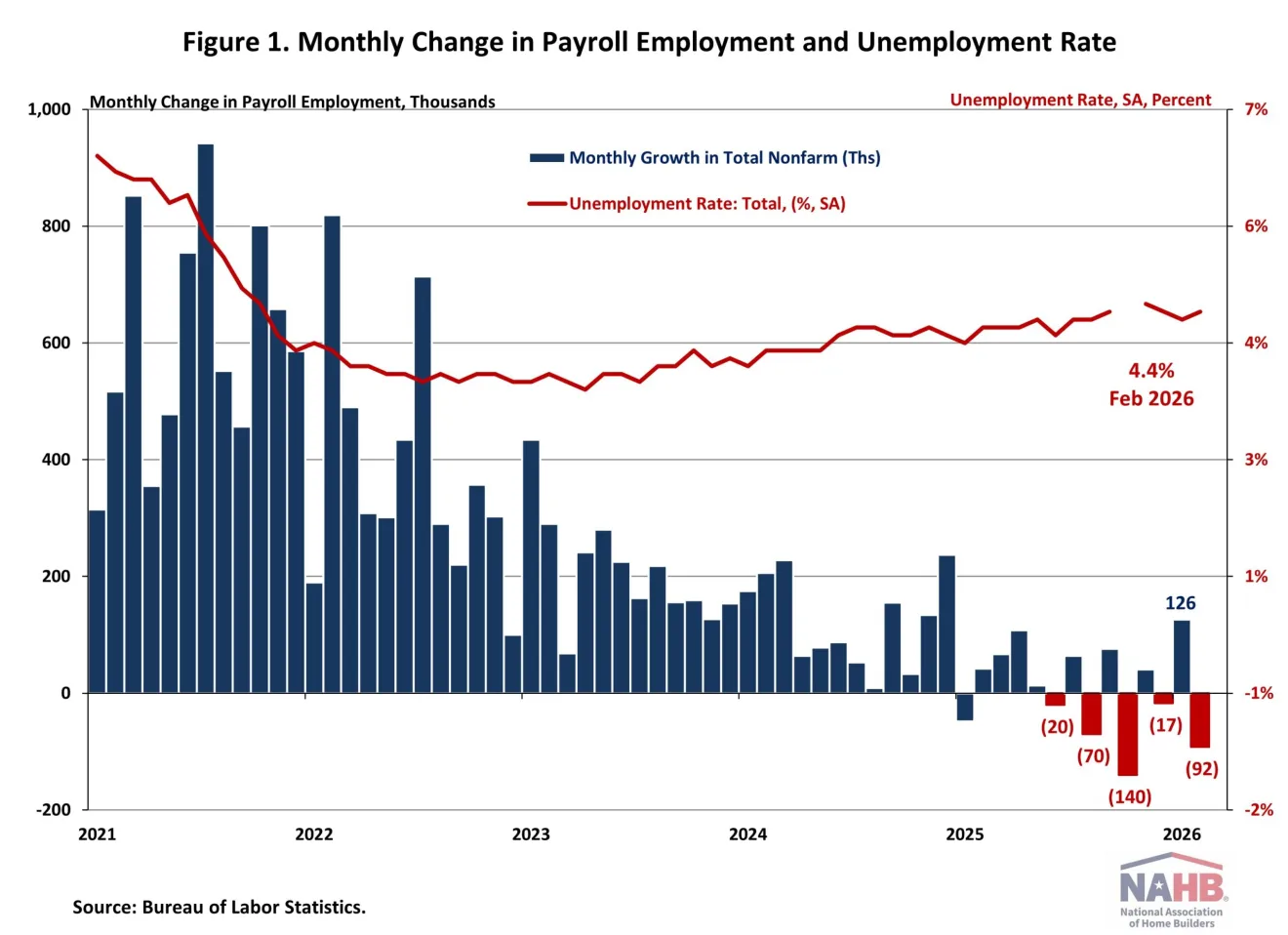

Jing Fu of the National Association of Home Builders (NAHB) highlights several deeper labor market signals beneath February’s 92,000-job loss. The labor force participation rate slipped to 62.0%, its lowest since January 2022 and still well below the pre-pandemic level of 63.3%, suggesting more Americans are stepping back from the workforce entirely.

On the sector level, health care has been the primary engine of job growth in recent months. One bright spot: wage growth held up at 3.8% year over year, and workers’ pay has been outpacing inflation for nearly two years running. Still, the cooling labor market puts the Fed in a tough spot as it tries to balance slowing job growth against inflation pressures from rising oil prices tied to the Iran conflict.

Source: NAHB (March 2026)

Orphe Divounguy of Zillow comments on the jobs data and its impact on real estate:

“A weakening labor market generally increases the risk that households turn more cautious — especially first-time buyers and payment-sensitive movers. Housing activity depends heavily on confidence in job security and future income growth; when that confidence weakens, renters stay put longer, buyers delay entry, and would-be sellers hesitate to list. There is an offset: a weaker jobs report can support lower bond yields and mortgage rates, which helps affordability at the margin. But for housing turnover, confidence often matters as much as rates — and in a cooling-labor scenario, the confidence channel can dominate.”

Jeff Cox of CNBC adds context around the broader workforce trends behind February’s numbers, noting the economy has averaged fewer than 5,000 new jobs per month since Trump took office in January 2025, while federal government payrolls have shrunk by 330,000 positions, or 11% of the total federal workforce, since October 2024. Long-term unemployment also climbed, with the average duration reaching 25.7 weeks, the longest since December 2021. Fed San Francisco President Mary Daly struck a cautious tone, warning that “both of our goals are risks now,” as inflation prints above target and oil prices rise alongside a softening labor market, reinforcing the central bank’s wait-and-see posture heading into spring.

Spring selling season

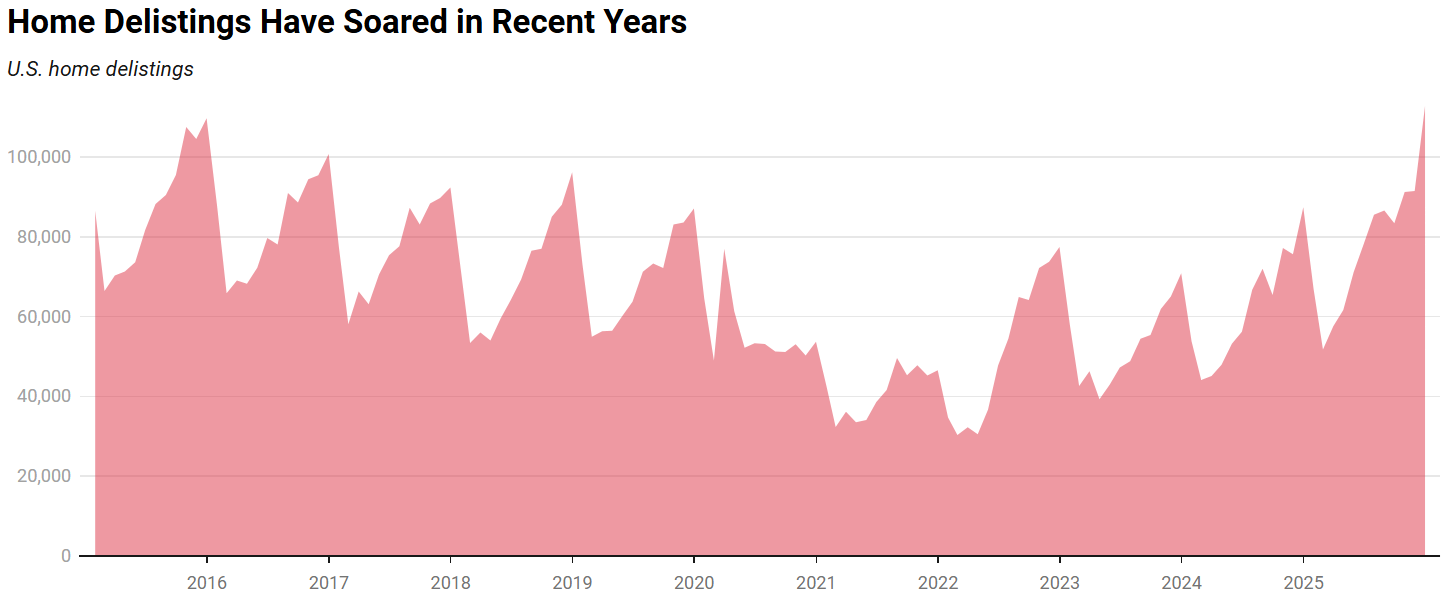

Lily Katz and Asad Khan of Redfin report that nearly 45,000 previously delisted homes returned to the market in January, the highest January figure in a decade and a record 3.6% of active listings. Many of these sellers pulled their homes last year rather than cut prices in a buyer-friendly market, with delistings hitting a record 112,788 in December 2025. Now they’re betting on the spring season to deliver better results, a trend that could further boost an already improving inventory picture and give buyers even more negotiating leverage heading into the busiest stretch of the year.

Source: Redfin (March 2026)

“Homebuyers are already scoring discounts because there are more homes for sale than people who want to buy them, and it’s possible those discounts will get bigger if relistings boost supply further…Some sellers will be more flexible on price when they relist since they’ve already been burned once. Buyers shouldn’t be shy about asking for concessions; even if the list price is high on paper, the seller may be open to negotiating.”

Anna Baluch of Realtor.com captures the optimism that was building just before the Iran conflict shook things up, with agents and lenders urging buyers to act in March while conditions were favorable. March buyers typically face far less competition than summer shoppers, reporting 40% more closed transactions during this period than in any other. Baluch warns that if too many buyers wait and flood the market later, rising prices could wipe out any savings from lower rates, a dynamic that now looks even more complicated as geopolitical uncertainty reshuffles the spring outlook.

Diana Olick of CNBC captured the surge in mortgage demand just before the Iran conflict disrupted the trend, with total applications jumping 11% in a single week as rates sat at their lowest since 2022. Refinancing activity was especially hot, up 14.3% week over week and a striking 109% higher than the same week a year ago, with conventional refinances alone climbing 20%. MBA analyst Joel Kan noted that rising average loan sizes among refinancers suggest borrowers with bigger mortgages were racing to lock in savings, a window that may now be narrowing as geopolitical uncertainty pushes rates back up.

Danielle Hale of Realtor.com offers a perspective, pointing out that even with rates ticking back up to 6%, they’re still well below the 6.6% to nearly 6.9% range buyers faced last spring. She also flags an important inventory nuance: while new listings climbed in February, overall active listing growth is losing momentum, with gains concentrated in lower-priced tiers in the South and West, a pattern that’s nudging the typical listing price lower. The takeaway is that despite the jobs slump and geopolitical jitters, the housing market still has meaningful tailwinds heading into spring compared to a year ago.