Last Updated on July 8, 2026

Hannah Jones of Realtor.com reported that investors bought roughly 534,000 homes in 2025, or 11.3% of all residential purchases, up slightly from 11% in 2024. Small investors accounted for 62.7% of investor buys, the highest concentration in more than 15 years. Mega-investors with 1,000 or more homes fell to just 7.5% of investor purchases, their smallest share since 2011 and down nearly 70% from their 2021 peak.

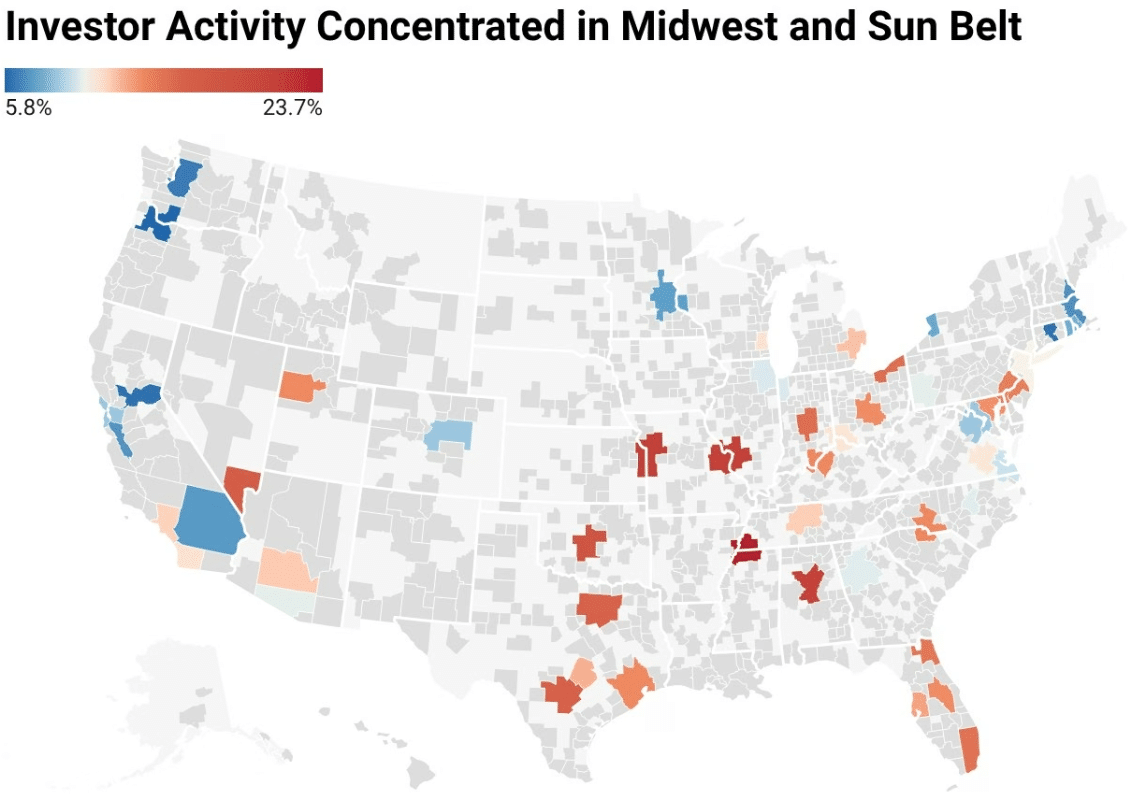

Source: Realtor.com (July 2028)

That said, Realty News Report reported that small investors remain steadfast net-buyers, acquiring about 53,000 more properties than they sold in 2025 while every other investor size category has moved to net-selling. Investor purchase share has held above 11% for three consecutive years, and Jones told the outlet the floor is unlikely to wear out quickly given how deep the small-investor base has become. Competition for entry-level homes has not gone away; it has simply shifted from Wall Street to Main Street.

Further, Giulia Carbonaro of Newsweek reported that a new map of investor activity shows mom-and-pop buyers concentrating in affordable Midwest and Sun Belt markets where prices are still within reach of local landlords. Large institutional investors, defined as those owning 350 or more homes, held just 7.5% of investor purchases in 2025, their smallest share since 2011. Jones told the outlet that competition has not disappeared, it has simply moved to the entry-level tier where small investors and first-time homebuyers now compete head to head.

However, Kavout Research reported that the Wall Street narrative is overblown, with institutional investors owning fewer than 4% of U.S. single-family homes nationally and some studies pegging the number closer to 1%. Small players with fewer than 10 properties own an estimated 85% of all investor-owned residential real estate. The report noted that even at their 2021 peak, investors with 1,000-plus homes accounted for less than 3% of national single-family purchases.

Finally, Morgan Stanley Real Estate Investing reported in its 2026 outlook that private capital is prioritizing cash-flow growth over cap-rate compression, targeting multifamily, single-family rental, and student housing in markets with clear demand-supply imbalances. The firm expects motivated sellers, engaged buyers, and improved debt availability to lift transaction activity and asset values in the back half of 2026. For individual investors, the takeaway is that a market dominated by mom-and-pop buyers plays to the strengths of well-organized small landlords with financial discipline and modern tools to compete against retail buyers.

Apartment rents climb, vacancy tightens

Naveen Athrappully of The Epoch Times reported that U.S. apartment rents rose 0.4% in June to a median $1,385, the fifth straight month of increases, according to Apartment List. Rents remain down 1.2% year over year and about 4% below the 2022 peak, but they are 21% higher than at the start of 2021. Fifty-one of the 56 largest metros posted month-over-month gains in June, and Apartment List called it the longest streak of consecutive monthly increases in a June reading going back to 2019.

That said, Intellectia.AI reported that a competing data set from CoStar showed rents up 0.1% month over month in June to an average $1,742, the seventh consecutive month of positive growth. The Pacific region led with a 0.2% monthly gain, while the South and Mountain regions posted year-over-year declines of 0.7% and 1.5% respectively. Among the top 50 markets, 41 saw month-over-month gains, with San Francisco leading at 0.7%.

Further, Building Design + Construction reported that the Harvard Joint Center for Housing Studies found the rental market is cooling as household growth slows, with the national renter vacancy rate reaching 7.3% in Q1 2026 after hitting historic lows in 2022 and 2023. Homeowner vacancy climbed to 1.1% over the same window. The Center flagged decelerating household formation as the primary drag on absorption, particularly in metros still working through 2024 delivery pipelines.

However, Roland Li of the San Francisco Chronicle reported that Bay Area rents are climbing sharply, with median asking rent for a one-bedroom in Oakland at about $2,000 in June, nearly 5% higher than a year earlier on an inflation-adjusted basis. Only 4.5% of Oakland units on Apartment List were vacant in June, the lowest share since the platform began tracking in 2017. San Francisco vacancy came in at 2.2%, down from 3.7% a year ago.

Finally, Sam Chandan of Chandan Economics reported that on-time rent collection at independent rentals stabilized at 83.8% in June, up 22 basis points year over year and ending a 34-month streak of annual declines. Two-to-four-family rentals led at 84.6%, single-family at 84.0%, and multifamily at 82.3%. For rental owners, the combined picture of firmer rents, tighter vacancy, and stronger collections marks the cleanest set of fundamentals since early 2023.

ROAD Act sits on Trump’s desk

Baker Botts reported that the 21st Century ROAD to Housing Act, which passed the Senate 85-5 on June 22 and the House 358-32 on June 23, is now on President Trump’s desk. The final bill defines a large institutional investor as any for-profit entity that controls 350 or more single-family homes and bars those firms from further acquisitions of existing single-family homes 180 days after enactment. Civil penalties reach up to $1 million per violation or three times the purchase price, whichever is greater; the prohibition sunsets 15 years after enactment.

That said, FBT Gibbons reported that the build-to-rent industry secured a broad exemption, allowing large institutional investors to continue funding, owning, and operating single-family homes purpose-built as rentals. The final bill also dropped the Senate’s original seven-year forced-disposition requirement for BTR communities, letting operators hold new-construction rentals for their full intended investment horizon. Renovate-to-rent, senior housing, and portfolio transfers among covered institutional investors are also excepted.

Further, Manu Raju of CNN reported that Speaker Mike Johnson transmitted the bill to the White House on June 29, starting the 10-day constitutional clock that ends on or around July 10. A source familiar told the network Trump is unlikely to sign but will not veto either, letting the bill become law without his signature. Trump canceled a scheduled June 25 signing ceremony after demanding Congress first move the unrelated SAVE America Act.

However, Meredith Lee Hill of Politico reported that Trump called the bill a “big yawn” during an Oval Office appearance on June 29, refusing to commit to signing while renewing his demand for the SAVE America Act. Realtor.com later reported Trump told an interviewer the bill is “fine” and hinted he will not veto it. Both chambers passed the bill with veto-proof supermajorities, meaning any veto could be overridden.

Finally, The Synthesis reported that the cap does not require divestiture: every home owned on the date of enactment stays, and the exceptions are broad enough to preserve most institutional strategies. Invitation Homes, which reported 85,970 single-family homes as of Q1 2026, keeps its entire portfolio and can still build or acquire homes for the rental market through the BTR carve-out. For rental investors below 350 homes, the ROAD Act is largely neutral on operations and modestly bullish on financing, thanks to a raised bank public-welfare investment cap of 20% and a new small-dollar mortgage pilot under $100,000.