Brooklee Han of HousingWire reports that inflation climbed to an annual rate of 3% in September, marking the third consecutive monthly increase and the highest level since January 2025, according to the delayed BLS release. Monthly, prices rose 0.3% seasonally adjusted, a slight slowdown from August’s 0.4% gain.

Jake Krimmel of Realtor.com reports that September’s delayed CPI showed headline inflation rising 0.3% month over month and 3% year over year, with core CPI up 0.2% monthly and 3% annually, mainly in line with expectations. The benign reading reinforces expectations of a 25 bps Federal Reserve rate cut at the Oct. 28–29 meeting. However, the shutdown has frozen other key economic data and left policymakers limited visibility. For housing, steadier inflation could keep the 10-year Treasury near 4% and mortgage rates at 12-month lows, improving affordability, though inflation still squeezes household budgets and constrains a full demand recovery.

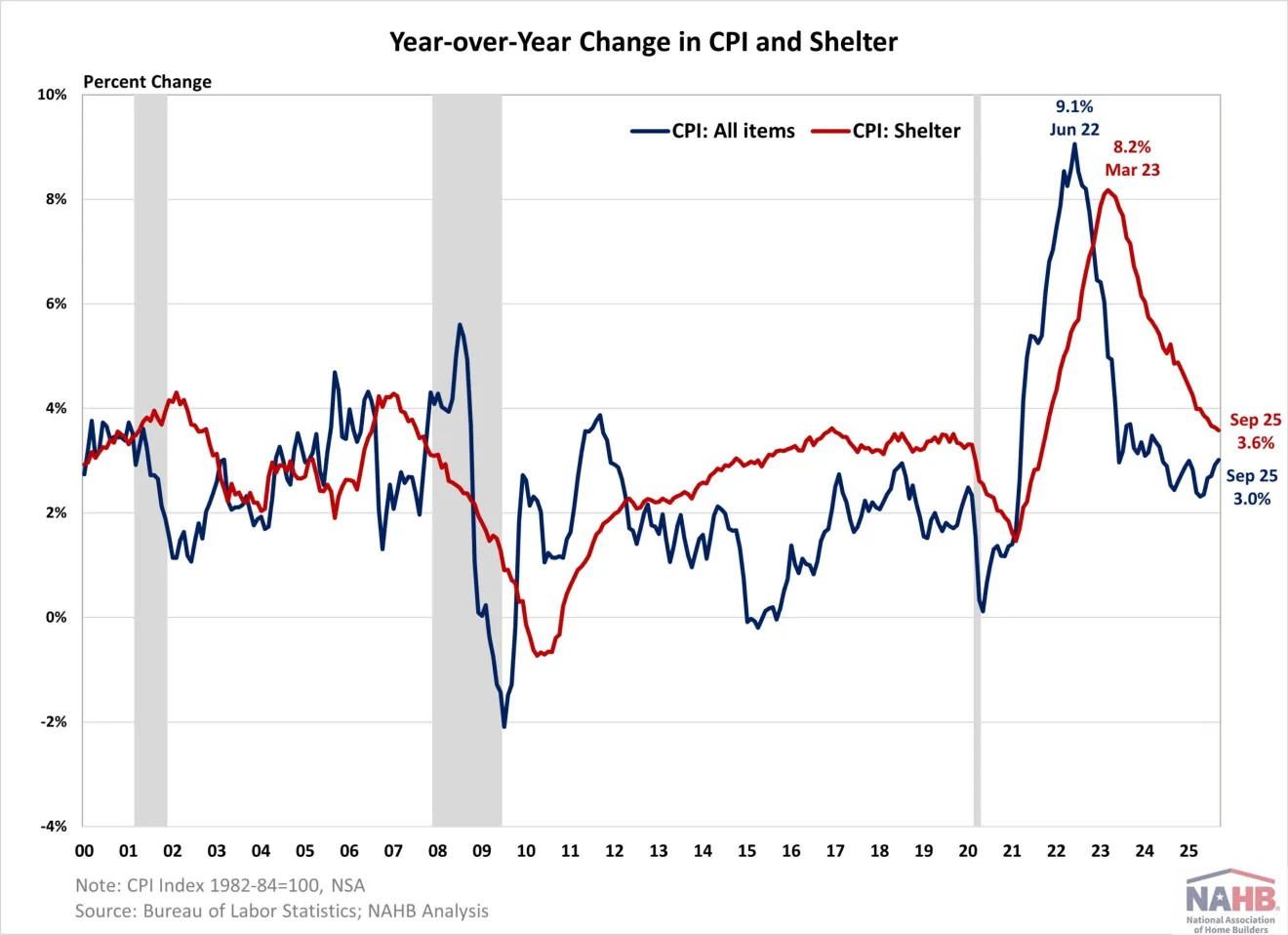

Fan-Yu Kuo of the National Association of Home Builders (NAHB) reports that inflation growth was the fastest since January 2025, as tariff-driven price pressures continue to emerge. While headline CPI rose 0.3% month over month and core CPI increased 0.2%, the most significant shift came from energy: gasoline prices surged 4.1%, overtaking shelter as the largest contributor to monthly inflation. Still elevated but easing shelter costs rose 0.2% monthly and 3.6% annually, the lowest since October 2021. Despite inflation staying sticky, signs of a weakening labor market suggest the Fed will continue easing, offering potential rate relief for a housing sector still facing affordability and supply constraints.

Source: NAHB (October 2025)

Mark Zandi, chief economist at Moody’s Analytics, comments:

“Inflation is well above the Fed’s inflation target, and the direction of travel is not encouraging…Tariff pass-through to goods prices will continue well into next year, and the highly restrictive immigration policy is adding to labor costs and thus food and service price inflation…We expect the core CPI to have increased by a relatively softer 0.3 percent in September on the back of further price pressures in tariff-exposed goods, most notably vehicles…The reacceleration in consumer spending also creates upside risk for discretionary services prices.”

PYMNTS reports on the data, highlighting that shelter costs, which make up more than one-third of the CPI, rose 0.2% in September and 3.6% annually. Rents rose 3.4% year over year, and owners’ equivalent rent posted its smallest monthly increase since 2021, at 0.1%. Food inflation continued to bite: overall food prices rose 0.2% in September and 3.1% over the year. Key grocery categories like cereals, bakery products, and nonalcoholic beverages jumped 0.7% monthly.

Source: PYMNTS (October 2025)

Housing inventory

Brooklee Han of HousingWire reports that existing-home sales rebounded in September, rising 1.5% month over month and 4.1% year over year to a 4.06 million seasonally adjusted annual rate, helped by easing mortgage rates and improving affordability. At the same time, unsold inventory climbed 1.3% to 1.55 million homes, reaching a five-year high and standing 14% above last year’s levels, a welcome sign for buyers who have faced record-low supply throughout the market slowdown.

The National Association of Realtors (NAR) reports that inventory climbed to 1.55 million homes, a five-year high and 14% above last year. Prices continued their steady ascent, with the median sales price up 2.1% year over year to $415,200, marking the 27th straight month of annual gains. Regional activity was mixed: sales jumped 5.5% in the West and 2.1% in the Northeast, dipped 2.1% in the Midwest, and rose 1.6% in the South. Homes spent a median of 33 days on market, 30% of buyers were first-timers, and cash sales held at 30%, reflecting stronger affordability from falling mortgage rates and continued financial stability among home sellers.

Danielle Hale of Realtor.com highlights that September’s sales momentum may extend into October and November thanks to seasonal advantages that favor buyers. Fall typically brings more inventory, fewer competing bidders, and softer pricing, conditions already emerging with more widespread price cuts, especially in lower-priced segments. Because many September closings were tied to contracts written in August, when buyer incentives improved, the market is now entering a period where seasonal tailwinds and cooling prices could help sustain modest sales growth even if overall demand remains muted.

Source: Realtor.com (October 2025)

Lucia Mutikani of Reuters comments: “Though mortgage rates have declined to one-year lows and housing inventory has improved, economists said affordability remained a challenge for many prospective buyers, especially lower and middle-income households. That problem is being compounded by a hazy economic outlook and lack of hiring by employers against the backdrop of import tariffs.”

Mortgage rates

Jake Krimmel of Realtor.com reports that 30-year mortgage rates fell to 6.19%, their lowest level in more than a year and roughly 50 basis points below midsummer, as markets price in a Fed rate cut and the 10-year Treasury dips under 4%. The government shutdown has created a “data vacuum,” leaving investors to lean on limited indicators like the delayed CPI report to gauge inflation and policy direction. While the October cut is already baked in, Krimmel notes that uncertainty over a December move, persistent budget deficits, and sticky inflation expectations may cap how much further rates can fall.

Source: Realtor.com (October 2025)

Kara Ng of Zillow reports that a September dip in mortgage rates helped propel unusually strong fall housing activity, keeping buyers and sellers engaged when the market typically cools. Lower rates helped soften the seasonal slowdown: new listings swung from a 3% annual decline in August to a 3% yearly growth in September, and pending sales fell far less than usual. With rates easing and inventory up 14% yearly, buyers have more breathing room, reflected in a jump from 6 to 15 major metros classified as buyer’s markets. In short, cheaper borrowing costs didn’t just boost affordability—they helped extend housing momentum deeper into fall than usual.

Dana Anderson of Redfin reports that falling mortgage rates are boosting purchasing power: a buyer with a $3,000 monthly budget can now afford a $473,750 home, up $26,000 from last year as rates drop to an average 6.17%, near a three-year low. Yet the market isn’t responding: pending sales slipped 0.7% year over year, marking the third straight weekly decline. Anderson highlights that while lower rates ease payments (the typical mortgage is up just 0.6% annually), buyers remain hesitant due to economic and political uncertainty, and home prices are still rising, with the median up 2% year over year, the largest jump in six months.

Finally, Diana Olick of CNBC notes that even as lower mortgage rates pushed September home sales up, as stated above. The gains are not evenly distributed; the luxury market carries outsized weight. Homes priced above $1 million saw a 20% jump in sales. The most affordable tier (under $100,000) grew less than 3%, highlighting how price pressure and limited supply continue to squeeze entry-level buyers. Despite a 14% annual increase in inventory, supply is still historically lean, keeping the median sales price at $415,200, up 2.1% year over year and 53% above pre-COVID levels.