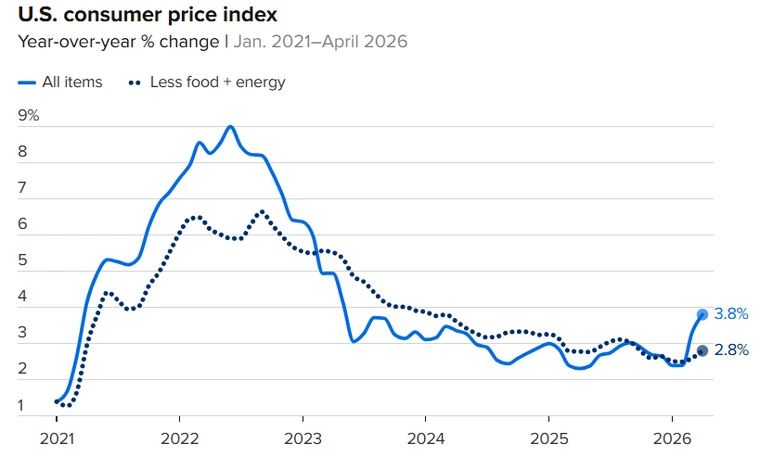

The U.S. Bureau of Labor Statistics reported that the Consumer Price Index rose 0.6% on a seasonally adjusted basis in April after a 0.9% gain in March, lifting the 12-month rate to 3.8%, the highest annual reading since May 2023. The energy index jumped 3.8% on the month and 17.9% over the past year, accounting for more than 40% of the all-items monthly increase. Shelter rose 0.6% monthly, with both rent and owners’ equivalent rent each up 0.5%, while the 12-month shelter gain held at 3.3%. Core CPI (all items less food and energy) climbed 0.4% monthly and 2.8% annually, up from 2.6% the prior month.

That said, Jeff Cox of CNBC reported that the April reading exceeded the Dow Jones consensus of 3.7% and marked the hottest annual print since May 2023. Real average hourly wages fell 0.5% for the month and 0.3% year over year, the first time in three years that wage gains have been consumed by inflation. Grocery prices jumped 0.7% in April, the largest monthly increase since August 2022, and CME Group data now shows roughly a 30% probability of a Fed rate hike by year-end. The Federal Reserve held rates steady in late April amid four dissenting votes, as national gasoline averaged $4.50 per gallon and crude oil traded above $100 a barrel.

Source: CNBC (May 2026)

Further, Piero Cingari of Interactive Brokers documented how the energy shock from the Strait of Hormuz blockade reverberated across the CPI basket, with crude oil futures jumping above $101 per barrel and fuel oil up 54.3% year over year. Shelter reaccelerated to 0.6% month over month from just 0.3% in March, with lodging away from home up 2.4% on the month and owners’ equivalent rent up 0.5%. Core CPI ticked higher to 2.8% from 2.6% (topping the 2.7% forecast), and CME FedWatch traders are now pricing over a 70% probability of a Fed rate hike by April 2027, with the door to cuts effectively shut through year-end.

However, Chandan Economics framed the report through a rental-housing lens, noting that the shelter CPI nearly doubled its monthly pace in April after months of gradual cooling, reversing one of the more encouraging trends in recent reports. Core CPI now sits 80 basis points above the Fed’s 2.0% target, and the post-CPI implied probability of a rate hike by year-end jumped to 30.4% (versus just 1.6% on April 10). The 10-year Treasury was trading near 4.38% on May 12 and moved higher after release, which, combined with sustained energy and food inflation, could squeeze payment performance for workforce and affordable housing tenants in the months ahead.

Finally, George Ratiu of the National Apartment Association highlighted the under-the-hood pressure on operators, observing that PPI surged 1.4% in April (the largest monthly increase since March 2022) and 6.0% year over year, the fastest pace in more than two years. Shelter makes up 33% of the CPI basket, so its 3.3% annual gain continues to drive headline inflation even as private-market rents have moderated. With the 10-year Treasury near 4.5% and elevated mortgage rates likely to keep homeownership out of reach for many, apartment demand should remain supported even as building materials, maintenance supplies, and contracted-services costs continue to pressure NOI.

Amended SFR bill

Lance Murray of The MortgagePoint reported that senior House lawmakers reached a bipartisan deal late Wednesday on the 21st Century ROAD to Housing Act and scheduled a floor vote for next week under suspension of rules (requiring a two-thirds majority). The amended text preserves Trump’s priority of restricting Wall Street’s purchase of single-family homes but scales back the Senate bill’s institutional investor limits, including removing the seven-year sell-off requirement for long-term rental homes. The bill also narrows the definition of single-family home to exclude manufactured housing and renovated-for-sale homes, preserves a five-year ban on a Federal Reserve digital dollar, and retains the Build Now Act tying CDBG funding to local housing production.

That said, Tristan Navera of Realtor.com explained that while the seven-year BTR sell-off rule was stripped from the House version, the core institutional investor ban remains largely intact: companies owning 350 or more single-family homes are barred from purchasing additional ones, with civil penalties enforced by the Treasury Department. The House version also removed the 15% rehab spending requirement for renovate-to-rent investors. Despite the heated debate, large institutional investors currently account for just 1% of total single-family home purchases nationally, though they comprised up to 16% of all investor purchase activity between 2015 and 2025.

Further, Katherine Hapgood of Politico placed the housing vote in a broader political context, reporting that House Republicans are simultaneously pursuing a third reconciliation bill by the end of July to address affordability concerns for voters ahead of the midterms. Speaker Mike Johnson expressed confidence in meeting the timeline, while Rep. August Pfluger noted that the party has achieved every objective set so far. With only about 30 legislative days before the July 23 summer recess, the housing vote is one of several time-pressured priorities competing with the gas-tax holiday debate and stalled energy permitting bills.

However, Winthrop & Weinstine reported that bipartisan members of the U.S. House urged leadership to strip or revise Section 901’s BTR-related restrictions, warning that the sweeping definitions combined with the mandatory seven-year divestiture requirement would effectively halt nationwide BTR production and eliminate hundreds of thousands of future units. On May 11, President Trump doubled down on Truth Social, demanding Congress pass the Act to ensure that ‘homes are for people, not Corporations.’ For BTR and SFR sponsors, the firm advises treating the Act as an immediate transaction and underwriting issue.

Finally, the Banking Journal summarized the banking-sector angle, noting that the House amendment rethinks regulations hampering small-dollar mortgage lending and expands tenant assistance and protections. The bill includes provisions to reward communities that build more housing supply and to ease environmental review of new construction. House Financial Services Committee Chairman French Hill emphasized that the bill cuts unnecessary barriers to home construction and modernizes HUD programs, while preserving banks’ ability to deploy funding into their communities, a key win for the community banking title preserved in the House version.

Mortgages

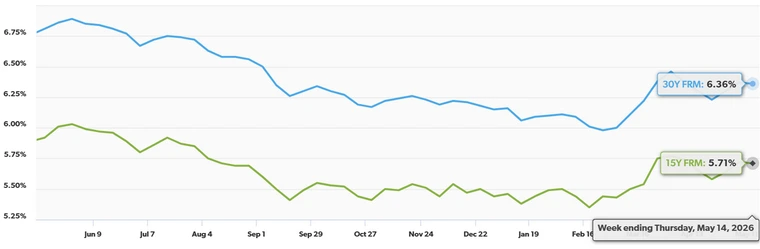

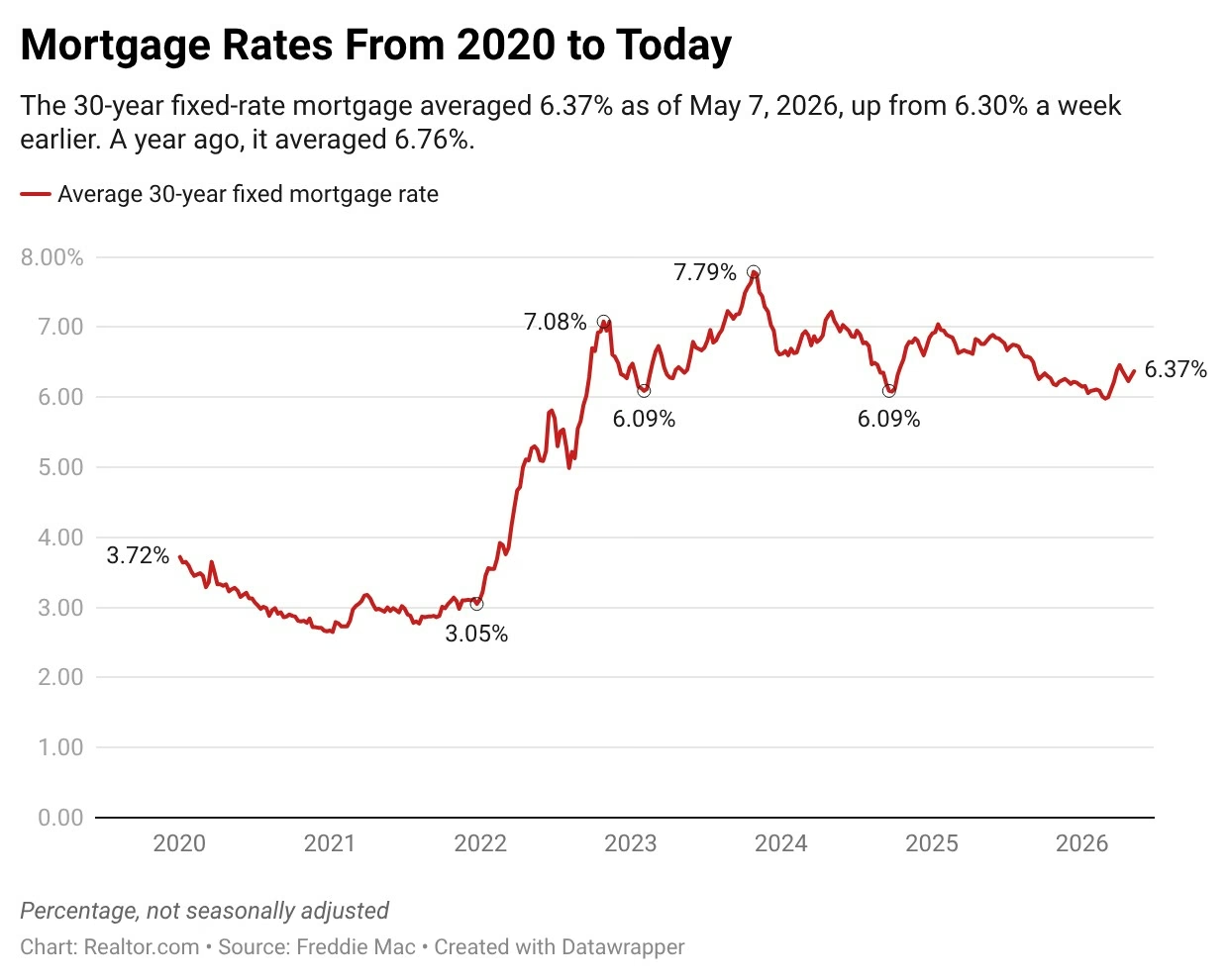

Freddie Mac’s Primary Mortgage Market Survey reported that the 30-year fixed-rate mortgage averaged 6.36% for the week ending May 14, down one basis point from 6.37% the prior week and 45 basis points below the 6.81% recorded a year ago. The 15-year fixed-rate mortgage averaged 5.71%, also down one basis point from 5.72% and below 5.92% a year earlier. Freddie Mac noted that purchase demand is softening but remains above the same time last year, with recent data also showing existing-home sales modestly edging up.

Source: Freddie Mac (May 2026)

“Mortgage rates ticked down this week, averaging 6.36%. While purchase demand is softening, it remains above this time last year. Recent data also shows existing-home sales modestly edging up.”

That said, Freddie Mac also confirmed the data and attributed commentary, with Chief Economist Sam Khater noting that purchase demand is softening but remains above last year’s levels. The 30-year FRM is down 45 basis points year over year, and the 15-year FRM is down 21 basis points, providing some affordability relief versus spring 2025 even as rates remain elevated against the post-pandemic backdrop. The release underscores that while geopolitical headlines have whipsawed weekly readings, the longer-run trend is one of gradual easing from cycle highs.

Further, Joel Kan of the Mortgage Bankers Association (MBA) reported that total mortgage applications rose 1.7% in the week ending May 8 (seasonally adjusted), with the Purchase Index up 4% week over week and 7% above year-ago levels across all loan types. The 30-year conforming fixed rate edged up to 6.46%, its highest level in five weeks, while refinance applications slipped 1% and the refinance share of activity fell to 40.8%, the lowest reading since July 2025. Kan attributed the purchase pickup to homebuyers shrugging off economic and rate uncertainty and returning to the market.

However, Hannah Jones of Realtor.com Research described a market in a holding pattern, with median listing prices falling 2.5% year over year for the 17th consecutive week of annual declines (improving from the prior week’s -2.9% pace). Active inventory is up 2.3% year over year but growth has moderated from nearly 10% at the start of the year, while asking prices have fallen or held flat for 29 straight weeks. New listings ticked up 2.1% year over year (reversing the prior week’s -2.5%), and homes spent just one extra day on market versus last spring, suggesting sellers are pricing to sell rather than listing high and cutting later.

Finally, Keith Griffith of Realtor.com captured the week-prior context, reporting that both buyers and sellers grew cautious in early May as rates ticked higher to 6.37% from 6.30%, with new listings down 2.5% year over year for the week ending May 2 and purchase applications down 4% week over week (though still 5% above year-ago levels).

Source: Realtor.com (May 2026)

Realtor.com economist Jiayi Xu noted some sellers are gradually reengaging while others stay on the sidelines amid rate volatility, and MBA’s Joel Kan attributed elevated rates to the ongoing Middle East conflict. The picture across both weekly reports is one of a market sensitive to every basis-point move but slowly absorbing supply.