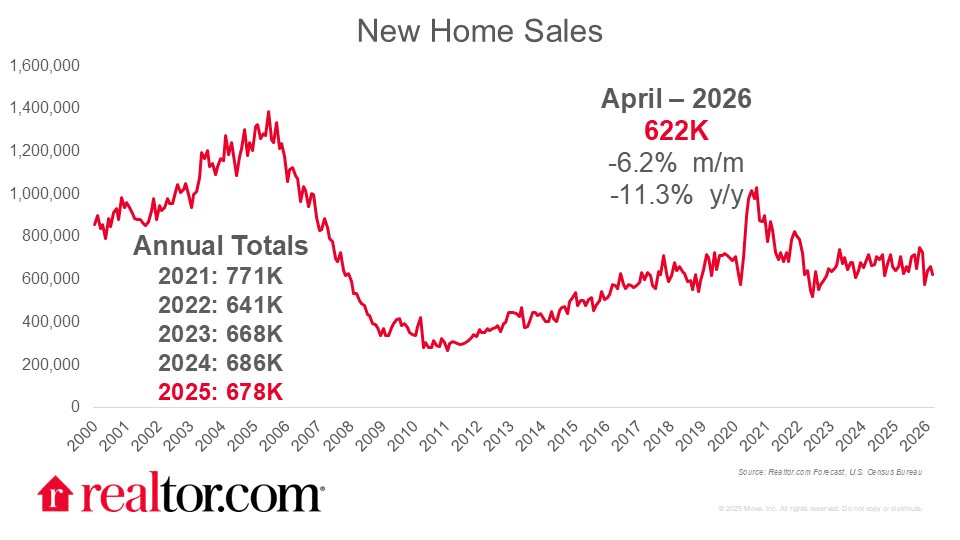

Joel Berner of Realtor.com reported that new-home sales slowed 6.2% month over month and 11.3% year over year in April, the weakest month for new-home sales in the past year apart from January’s storm-driven dip. The slowdown is attributed to higher mortgage rates and lower consumer confidence, with year-to-date new-home sales 6.5% below 2025 levels. The months’ supply rose to 9.4 from 8.7 in March (versus 8.6 last April), with the West the only region showing an upward sales trend at +18.7% MoM, while the Midwest tanked 25.0%, the Northeast fell 12.9%, and the South dropped 9.8%.

Source: Realtor.com (June 2026)

“The new-home market is strongly in the buyer’s territory. Expect builders to continue to pull back on single-family home construction if sales remain weak, and expect more price reductions and buyer incentives to be offered to sweeten the deal for reluctant buyers.”

That said, Tristan Navera, also of Realtor.com, reported that the April pace of 622,000 SAAR missed expectations as the median new-home price rose to $422,500 (up 8.0% from March and 2.2% above April 2025), driven by a shift toward higher-priced inventory rather than broad price appreciation. The average sales price of $508,000 was 1.1% below April 2025, suggesting the price mix is skewing upmarket even as overall demand softens. Builders’ reluctance to hold inventory likely means continued incentives, which could ultimately benefit buyers willing to transact at current rates.

Further, Zillow Research confirmed the April reading was the lowest for any April since 2022, with 622,000 SAAR new single-family home sales. The number of new homes for sale at the end of April stood at 504,000, the highest since November 2007, when the housing bubble was deflating. Zillow’s analysis noted builders are increasingly relying on incentives such as mortgage-rate buydowns and price reductions to move inventory, and that the share of new homes priced above $500,000 rose to roughly a third of all sales in April.

However, the U.S. Census Bureau and HUD released the primary April data showing total sales of new single-family homes fell 6.2% from a revised March pace to 622,000 SAAR (and 8.0% below April 2025). The seasonally adjusted estimate of new homes for sale stood at 504,000 (a 9.7-month supply at the current pace), and the median sales price was $422,500, with an average of $522,400. The release confirms a builder market that has lost momentum as financing costs reset higher into late spring.

Finally, KPMG wrote that sales activity is increasingly concentrated at the higher end of the market, with homes priced above $500,000 making up roughly a third of all April new-home sales. Affluent buyers able to absorb higher rates and prices are dominating, while demand at the entry-level and middle price points remains constrained. April CPI ran at the hottest pace since May 2023, and the personal saving rate fell to 2.6%, the lowest since 2008, with real disposable income declining for a third consecutive month. The firm concluded the spring buying season has delivered another disappointment with no sustained rate relief in sight.

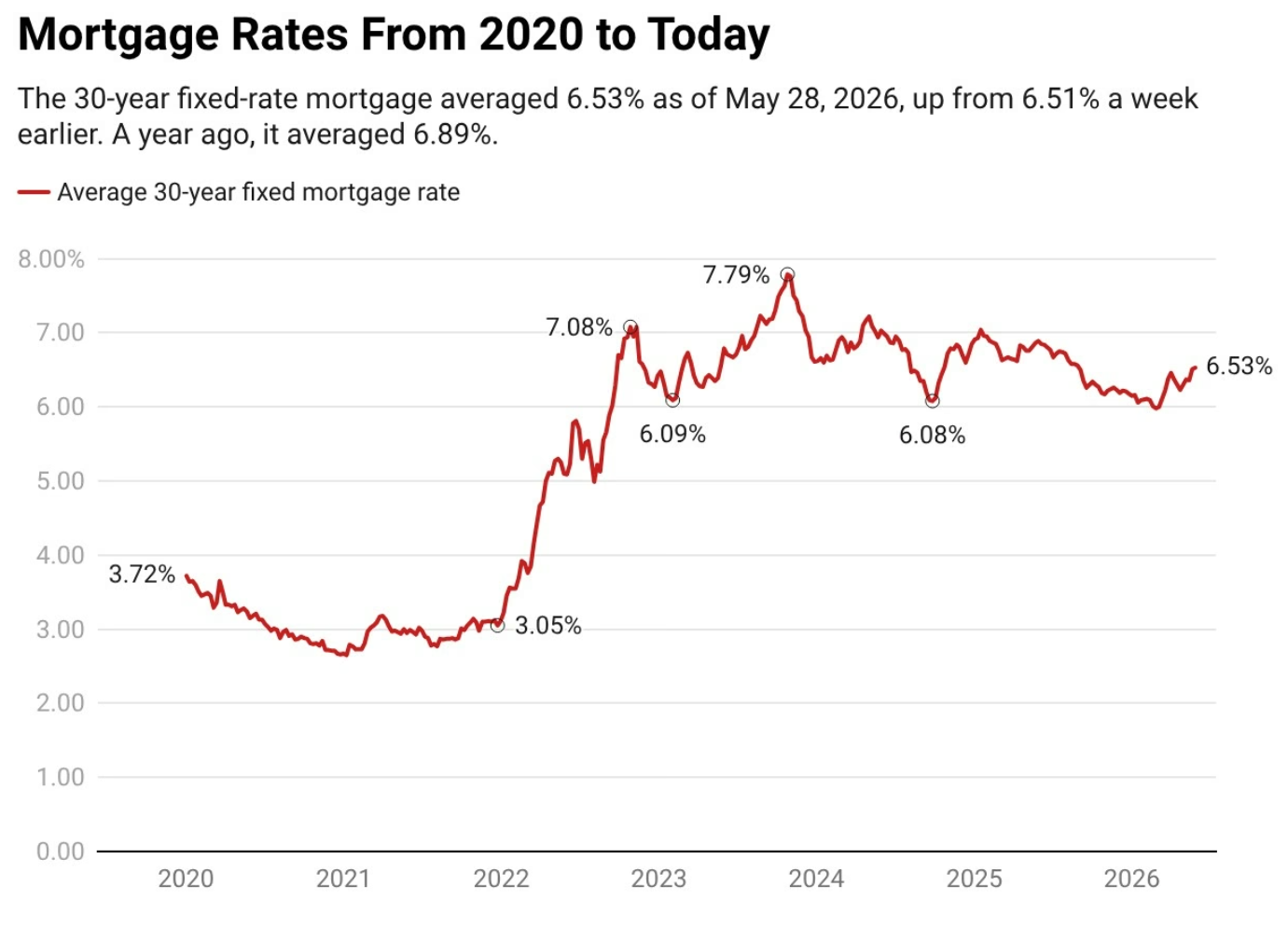

Mortgage rates hit a 9-month high

Snejana Farberov of Realtor.com reported that the average 30-year fixed mortgage rate climbed to 6.51% on May 21, the highest level since late August 2025, propelled higher by soaring energy costs from the ongoing Iran conflict. The outlet noted rates have moved up 53 basis points in less than three months, reversing the progress that briefly pushed rates below 6% in late February. April CPI rose 3.8% year over year while wages grew just 3.6%, meaning the war has effectively nullified real earnings growth for the typical household and dealt a double blow to housing affordability.

Further, Farberov updated readers that rates ticked up further to 6.53%, even with a looming Iran peace deal that could ease the energy-price shock. Krimmel noted that pending home sales have nonetheless increased three months in a row, indicating latent buyer demand that would re-engage if mortgage rates declined. Despite the headwinds, the economist argued that this spring is shaping up to be the most active in four years, with new listings and contract signings both up noticeably, even as buyers and sellers wait for clarity on the rate path.

Source: Realtor.com (June 2026)

“Pending home sales have increased three months in a row, indicating there’s latent demand and homebuyers are ready to jump back into the market if mortgage rates decline.”

Further, Kara Ng of Zillow published its weekly mortgage-rate analysis, noting the housing market is losing steam as rates stay elevated, with affordability the central constraint heading into June. The piece flagged that buyer demand remains highly rate-sensitive and that even small upticks in the 30-year fixed are now translating into measurable pullbacks in purchase applications and pending sales. Zillow’s framing matches the broader weekly data: rate sensitivity is acute at current levels, and a sustained move below 6.25% would be the catalyst the market needs to unlock additional transaction volume.

However, Mischa Fisher, also of Zillow, reported on its May 2026 home value and sales forecast, projecting a continued grind in transaction volumes with home values posting modest growth. The U.S. typical home value stands at $366,712 (up 0.7% YoY) and the typical rent at $1,930 (up 1.9% YoY) for April. The typical mortgage payment of $1,829 reflects the rate environment’s drag on buyer purchasing power, and Zillow flagged that sales of 323,631 units (-0.4% YoY) point to a flat-to-down transaction year barring meaningful rate relief.

Finally, Freddie Mac released its Primary Mortgage Market Survey for the week ending May 28, with the 30-year fixed averaging 6.53%, up from 6.51% the prior week, and the 15-year fixed averaging 5.79% (versus 5.74% the prior week). Chief Economist Sam Khater noted the modest uptick reflects sticky Treasury yields and that purchase application demand remains soft as buyers wait for clearer signals on the rate path. The PMMS anchors the week’s consumer rate read and reinforces the message coming from Realtor.com and Zillow that affordability is the binding constraint on spring activity.

Investor pullback

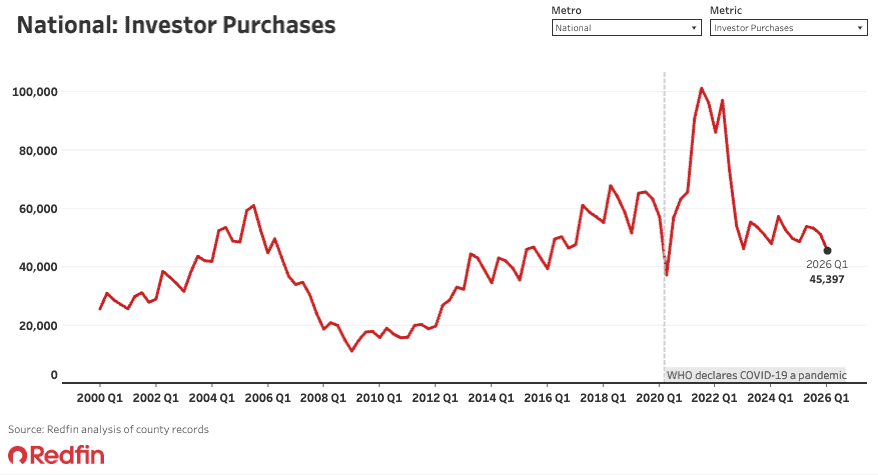

Redfin reported on May 28 that U.S. investor home purchases fell 6% year over year in the first quarter to their lowest level since 2020, with investors buying 19% of homes sold (down from 20% a year earlier) and holding just 7.8% of all U.S. home listings (the smallest share in five years). Investor purchases of low-priced homes fell 10% YoY to their lowest first-quarter level in a decade, and condo investor purchases dropped 8% to the lowest Q1 level since 2015. Detroit (-35%) and Orlando (-25%) led the metro-level declines, while Bay Area investor purchases bucked the trend with a modest rise.

Source: Redfin (June 2026)

“Higher mortgage rates, slowing price growth and rising construction costs are giving both investors and individual homebuyers pause…Flippers and investors are scaling back, and being much more strategic when they do buy homes. They’re buying less expensive materials, and being more careful about timing their projects to list during the stronger spring and summer seasons. It’s also noteworthy that large institutional investors are focusing more on building new homes than buying existing ones.”

That said, Redfin separately reported that the income needed to afford the typical U.S. home declined for the seventh straight month in April, with Americans now needing $116,780 to afford the median listing (down 2% from $119,191 a year earlier). One-third (32.9%) of U.S. home listings were affordable to someone earning the median income in April, up from 28.7% a year earlier. The data point to gradual improvement in affordability at the national level, even as rates remain elevated, driven primarily by modest price softening and wage growth rather than a meaningful rate break.

Further, Redfin noted that just 28.8% of U.S. homebuyers paid all cash in March, down from 29.8% a year earlier and tied with 2021 for the lowest March share since 2020. The all-cash share peaked at nearly 35% in 2023 when mortgage rates hit a two-decade high near 8%, and the decline tracks the gradual moderation in rates from those peaks alongside the broader investor pullback. The combination of fewer cash buyers and fewer investor transactions suggests the marginal homebuyer in this market is increasingly rate-sensitive and financing-dependent.

However, the U.S. House Committee on Financial Services announced that the House passed the amended 21st Century ROAD to Housing Act on May 20 by an overwhelming bipartisan vote of 396-13. The 56-provision package addresses housing supply, manufactured housing, mortgage financing, rural and veteran housing, and community banking, with Chairman French Hill (R-AR) calling it proof that Washington still works. The House version strips the Senate’s seven-year sell-off requirement for build-to-rent properties but preserves the core 350-home institutional investor framework, and the bill now heads back to the Senate for reconciliation with its earlier March version.