Glenn Thrush and Colby Smith of the New York Times report that the U.S. attorney’s office in Washington, D.C., has opened a criminal investigation into whether Federal Reserve Chair Jerome H. Powell misled Congress about the scope of a $2.5 billion renovation of the Fed’s headquarters, with investigators reviewing Powell’s public statements and the project’s spending records; officials say the probe was approved in November by Jeanine Pirro, a Trump ally appointed to run the office last year, and Powell confirmed the Fed was served with grand jury subpoenas days earlier. Powell called the move “unprecedented” in a rare Fed video and warned it could become a test of the Fed’s independence as President Trump escalates a long-running campaign against Powell over interest rates, has floated firing him, and says he’s chosen a replacement ahead of Powell’s chair term ending in May.

Howard Schneider and Ann Saphir of Retuers report that the Trump administration’s criminal probe of Powell has triggered unusually broad pushback; with Powell publicly calling the investigation a “pretext” to gain presidential influence over interest rates, former Fed chairs Janet Yellen, Ben Bernanke, and Alan Greenspan warning it risks undermining central-bank independence, and multiple Republican senators (including Thom Tillis, Lisa Murkowski, and John Kennedy) condemning the move. Market jitters were evident in higher long-term Treasury yields as investors weighed the implications of a less independent Fed for inflation and monetary policy.

Greg Iacurci and Jessica Dickler of CNBC report that the criminal investigation could hit consumers’ wallets by undermining confidence in the Fed’s political independence. Economists warn that this erosion would likely translate into higher long-term borrowing costs (especially mortgages and other loans), more market volatility that can weigh on retirement and investment accounts, and potentially a weaker economy over time. Moody’s chief economist Mark Zandi warns there’s “nothing but downside” for investors and consumers. At the same time, Columbia’s Brett House argues an “assault” on Fed independence can mean higher rates, greater volatility, and uncertainty, even if the White House frames pressure for faster rate cuts as affordability relief.

Jake Krimmel of Realtor.com argues that the administration’s criminal investigation and broader pressure campaign on the Fed risks undermining the central bank’s credibility, which economic research and historical experience suggest can translate into higher inflation expectations, greater market volatility, and (counterintuitively) higher long-term borrowing costs even if the White House’s stated goal is lower mortgage rates. Krimmel’s core point is that the Fed influences short-term rates. In contrast, 30-year mortgage rates track the long end of the Treasury curve (predominantly the 10-year) and therefore depend on investors’ confidence in stability and low inflation, which political interference can weaken.

At the same time, Krimmel notes the Fed still has enough institutional “credibility capital” that near-term policy is unlikely to change in January, and he flags the political check on the probe; swift pushback from senators that could complicate confirming a successor and increase the odds Powell stays on as a governor after his chair term ends.

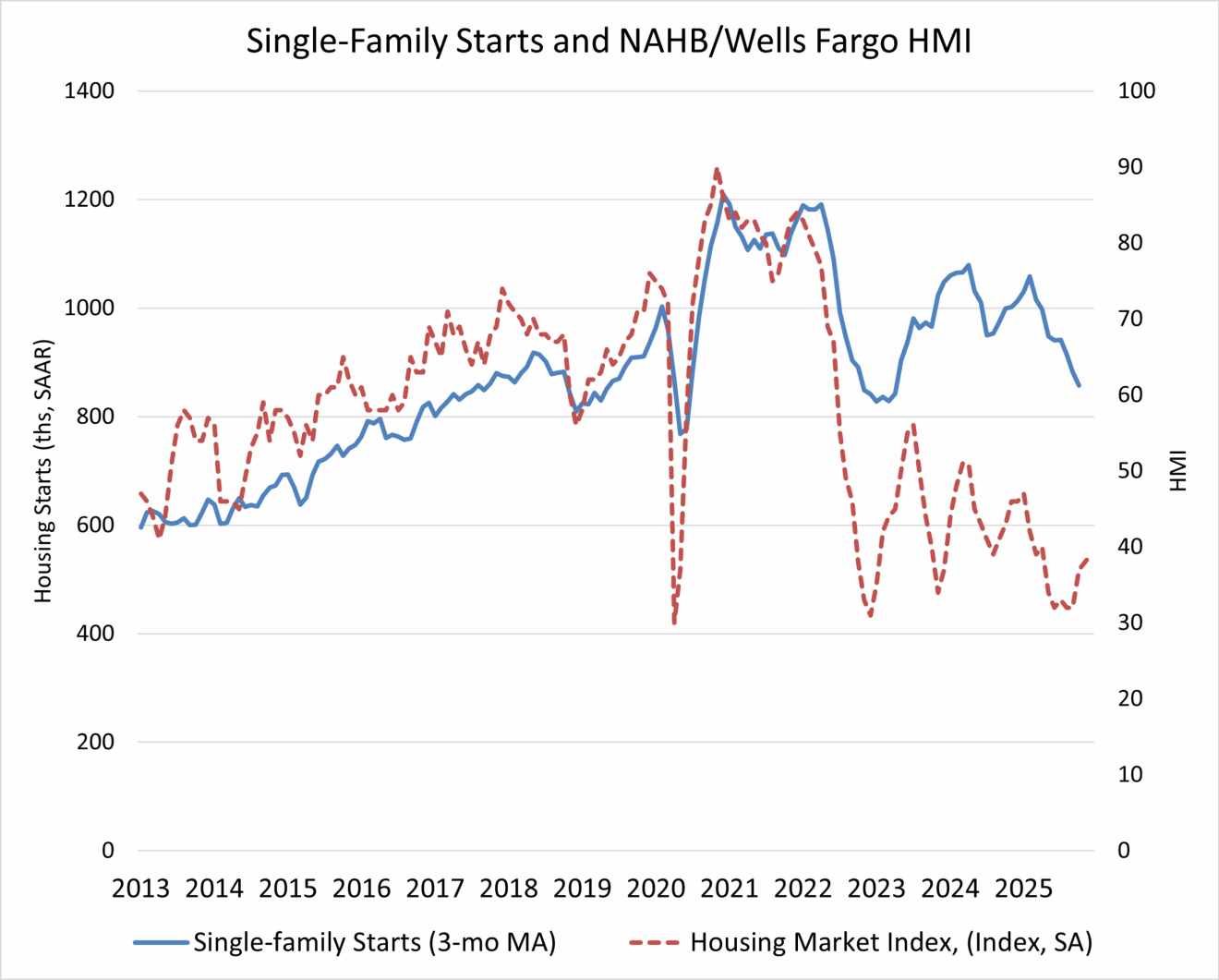

Construction update

Danushka Nanayakkara-Skillington of the National Association of Home Builders (NAHB) reports that U.S. residential construction weakened in October as earlier elevated mortgage rates and persistently high construction costs squeezed demand and builder activity: housing starts fell 4.6% to a 1.25 million seasonally adjusted annual rate, with single-family starts up 5.4% to 874,000 but still down 7.8% year over year (and down 7.0% year-to-date), while the three-month moving average for single-family slipped to 857,000.

Source: NAHB (January 2026)

Meanwhile, multifamily starts dropped 22.0% to 372,000, with the multifamily three-month average down to 424,000 and activity 7.9% below year-ago levels.

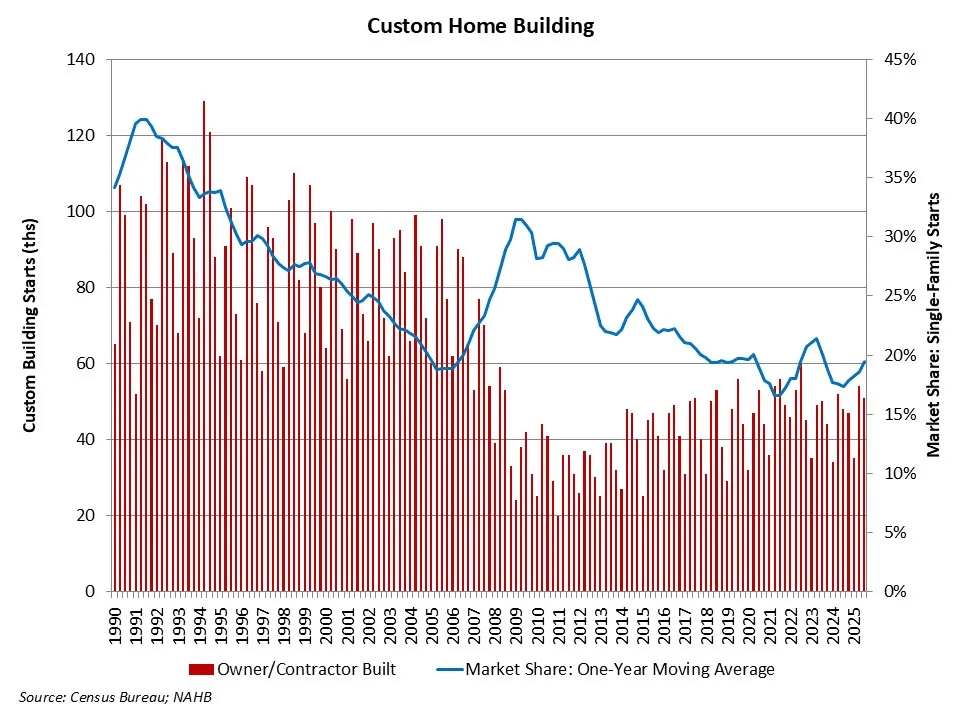

Robert Dietz of NAHB reports that custom home building is growing year over year even as broader single-family construction remains weak, with NAHB’s analysis of Census data showing 51,000 custom starts in Q3 2025, up 6% from Q3 2024, and 187,000 custom starts over the last four quarters, up 5% versus 178,000 in the prior four-quarter period; custom homes now account for just over 19% of total single-family starts on a one-year moving average, below the 31.5% peak in Q2 2009 and the 21% peak in early 2023, reflecting how custom building (less rate-sensitive, more tied to household wealth/stock prices) is gaining share as spec home building declines and equities rise.

Source: NAHB (January 2026)

Dietz also reports that townhouse (single-family attached) building continued to take share in Q3 2025, with 46,000 attached starts in the quarter and 179,000 townhouse starts over the last four quarters (up 1% from 177,000 in the prior four-quarter period) putting townhouses at almost 20% of all single-family starts in Q3; on a one-year moving average, newly built townhouses reached 18.7% of single-family starts, the highest share on record in data going back to 1985, well above the prior two-decade peak of 14.6% in Q1 2008, as demand shifts toward medium-density, walkable neighborhoods where zoning allows them to be built.

More policy updates

It was a busy few weeks of federal housing policy moves, beginning with Mike Winters of CNBC reporting that President Trump wants to ban large institutional investors from buying additional single-family homes to improve affordability. Still, experts say the effect may be limited because firms owning 100+ homes control about ~2% of U.S. single-family housing stock and institutional investor purchases have cooled from a pandemic peak, falling from about ~3% to ~1% as rates rose; supporters argue big landlords can outbid families, especially in fast-growing markets, while skeptics counter the core driver is a multi-million-home supply shortage (Goldman Sachs estimates roughly 3 million additional homes are needed), noting ownership is geographically concentrated (about 80% of institutional-owned homes in just 5% of counties) and that restricting investor demand doesn’t add supply. Therefore, affordability hinges more on building constraints, such as construction costs, labor shortages, and regulations.

Max Zahn of ABC News reports that Trump’s proposed ban on large institutional investors buying more single-family homes is as much a political signal as an affordability fix, since analysts say Wall Street ownership is too small nationally to move prices much; about 450,000 homes (~3%) of the single-family market per a GAO study using 2022 data. That said, the idea resonates because investor ownership is highly concentrated in certain Sun Belt metros (GAO cites 21% in Jacksonville, 18% in Charlotte, and approximately one in four in Atlanta). Zahn notes the proposal’s immediate market impact was sharper than its housing impact: shares of major landlords/investors like Blackstone, Invitation Homes, and American Homes for Rent fell 4%–6%, while industry groups signaled willingness to engage, and the White House offered few details on how a ban would be implemented or enforced.

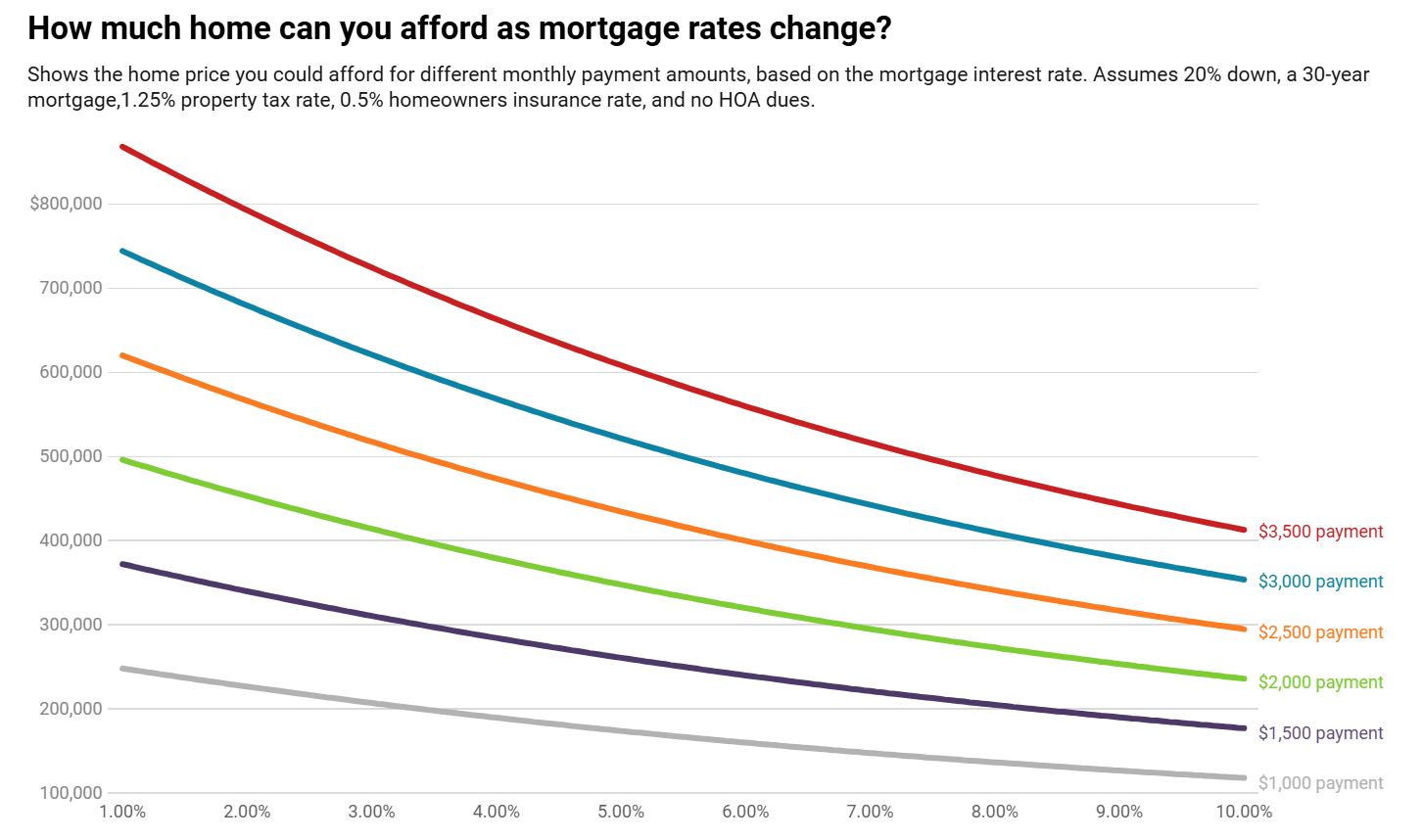

In an additional move, Dana Anderson of Redfin reports that mortgage rates fell below 6% for the first time in nearly three years after President Trump ordered the government to buy $200B in mortgage bonds, with the daily average rate dropping to 5.99% on Jan. 9 (from 6.21% the day before); for a buyer with a $3,000/month budget, that translates to about $14,000 more purchasing power versus a month ago at 6.35% (roughly $479,750 affordable now vs $466,000 then) and $30,000+ more versus early July’s roughly 6.8% (about $449,500 then), while the monthly payment on a $433,000 median-priced home is estimated at $2,537 now versus about $2,720 six months ago (~$180 more).

Source: Redfin (January 2026)

Chen Zhao, Redfin’s head of economics research, comments:

“House hunters should know that this may be near the lowest mortgage rates fall for the foreseeable future…The Fed is on track to leave rates alone for the next few meetings, especially after today’s mixed jobs report. Another plus for buyers: There are hundreds of thousands more home sellers than buyers in the market, allowing buyers to negotiate. Serious buyers may want to jump in before competition heats up in the spring.”

Manya Saini of Reteurs reports that Trump’s proposed one-year cap on credit-card interest rates could give some borrowers short-term relief (cards average about 19.65% APR, and U.S. balances hit $1.23T by Sept. 30) but may also tighten credit availability (especially for subprime borrowers) because banks use high card APRs (sometimes near 30%) to cover defaults; analysts warn a cap could cut bank profits, reduce lending and consumer spending, and push riskier borrowers toward BNPL providers or other higher-cost, less regulated options.

Finally, Sarah Wolak of HousingWire reports that the House passed H.R. 5184, the Affordable HOMES Act, 263–147 with bipartisan support (57 Democrats joining a unified Republican “yes” vote) seeking to boost manufactured-housing supply by restoring HUD authority over manufactured-housing energy standards and repealing a pending DOE rule, a change supporters argue could lower costs by about $10,000 per unit and speed one of the fastest, lowest-cost paths to expanding affordable housing.