Anthony Smith of Realtor.com reports that new listings fell 10% year over year for the week ending April 4, the steepest weekly decline since late January. Year to date, new listings are 2.3% below 2025 levels. Active inventory rose 3.9% YoY, but the pace of growth is moderating (up 5.2% in the prior two weeks). Median listing price dropped 2.1% YoY, marking the 24th consecutive week of flat or negative price growth.

Source: Realtor.com (April 2026)

Zillow reported that newly pending listings rose 4.6% YoY in March, the largest March increase in five years. Home values climbed 0.8% YoY (a slight acceleration from 0.4% in February), with 1.23 million homes for sale nationwide, up 4.2% YoY for the 28th consecutive month. Average daily page views per listing on Zillow were 32% higher than in March 2020, signaling pent-up demand.

Rachel Bader of HousingWire wrote that the housing market is fragmenting at the metro level, with inventory rising to 723,460 single-family homes while weekly pending sales slipped to 70,676 from 72,191 a year earlier. Florida led with a 43.6% price-cut rate (some metros near 50%), while the Northeast remained competitive; Boston posted a 21.4% weekly absorption rate with a median above $1 million. Detroit recorded a 29.5% absorption rate, well above national levels.

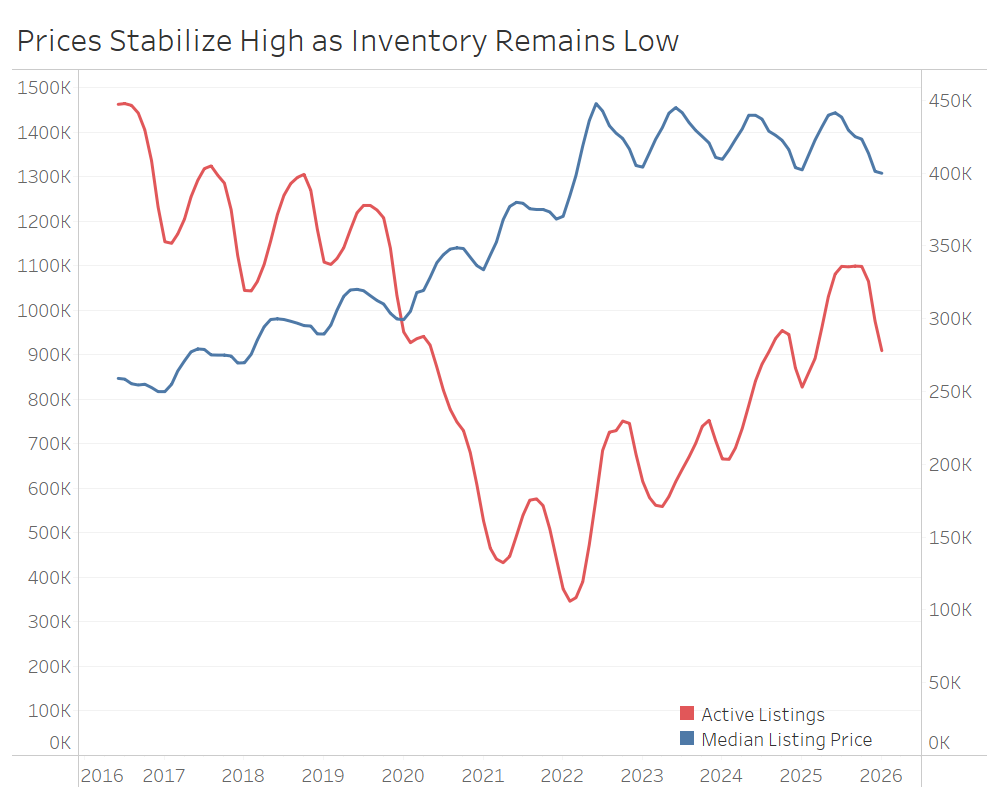

Dana Anderson of Redfin reported that pending home sales fell 2.4% YoY during the four weeks ending April 5, the biggest decline in three months. The typical home went under contract in 51 days, the longest time since 2019 for this time of year. Median sale price hit $392,973, up 2.2% YoY (the biggest increase in a year), while active listings dropped 2.2%, the largest decline since 2023. The ceasefire announced Tuesday in the Iran war could ease mortgage rates.

Source: Redfin (April 2026)

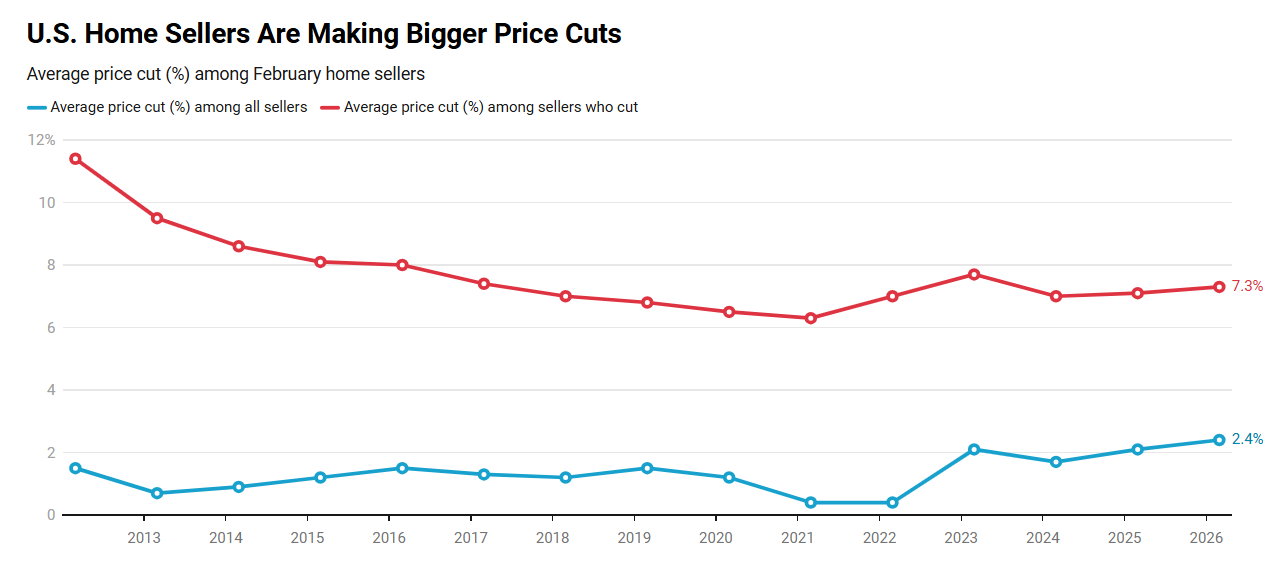

Finally, Lily Katz of Redfin found that a record 34.2% of February home sellers cut their list price, up from 31.5% a year earlier and the highest February share in data going back to 2012. Sellers who reduced their price lowered it by an average of $40,915, or 7.3%. San Antonio led at 57.9%, followed by Austin (55.2%) and Dallas (47.3%), while San Francisco had the lowest share at just 7.4%.

Source: Redfin (April 2026)

Mortgage applications

Joel Kan of MBA noted that while the Purchase Index edged up 1% week over week, it was 7% lower on an annual basis, the first YoY drop since January 2025. The 30-year fixed conforming rate eased to 6.51% from 6.57%. FHA purchase applications rose 5%, supported by the FHA rate being about 30 basis points lower than the conventional rate. Certain geographic segments with growing inventory are faring better.

“Higher mortgage rates and continued economic uncertainty weighed down on mortgage applications again last week. While mortgage rates saw a slight reprieve, with the 30-year fixed rate decreasing to 6.51%, many potential refinance borrowers have been frozen out by the sharp increase over the past month. The pace of refinance applications was at its lowest level since December 2025.”

Sarah Wolak of HousingWire wrote that the latest MBA data for the week ending April 3 showed applications declined 0.8%, with the refinance index down 3% week over week and 4% YoY, hitting its lowest level since December 2025. The 30-year fixed conforming rate eased to 6.51% from 6.57%, while FHA purchase applications rose 5%. The Xactus Mortgage Intent Index fell to 138.3, nearly 10% below the same period last year.

Matthew Graham of Mortgage News Daily noted that the pace of decline slowed considerably, with the Purchase Index rising 1% week over week even as it sits 7% below year-ago levels. FHA and ARM loans continue to hold up better due to relatively lower rates. Refinance share decreased to 44.3% from 45.3%, while ARM share increased to 8.6%. The 30-year fixed fell to 6.51% (from 6.57%), with jumbo loans at 6.54% and FHA at 6.22%.

Kara Ng of Zillow reports that mortgage rates have now eased into the mid-6% range after a ceasefire drove bond yields lower, though they remain well above the late February window when the 30-year fixed briefly dipped below 6%. Despite that rebound eroding a third of 2026’s affordability gains, March was one of the busiest months for newly pending home sales since late 2022, with Zillow listing page views up 32% year over year. Much of that resilience likely traces to buyers who locked rates during the sub-6% window and are now racing to close before those 30- to 60-day locks expire.

Sam Khater of Freddie Mac reported that the 30-year fixed-rate mortgage averaged 6.37% as of April 9, down from 6.46% the prior week and below the 6.62% recorded a year ago. The 15-year fixed averaged 5.74%, down from 5.77%. Khater called the decrease a positive development for prospective homebuyers that could spark a more favorable spring homebuying season than last year.

Housing policy

Jason Jordan of the American Planning Association wrote that HUD’s best practices guide is due by May 12, 2026, and the order directs streamlined permitting, by-right development for single-family homes, updated building codes, limits on green-energy mandates, and acceptance of manufactured/modular housing. HUD is also re-evaluating PRO Housing grant criteria, meaning these best practices may become conditions for federal housing grants. Formal regulatory action will take months to finalize.

The National Association of Home Builders (NAHB) reports that home builders surveyed through the Wells Fargo Housing Market Index see a complicated decade ahead, with the biggest long-term headwinds being government debt levels (cited by 82% of respondents), declining fertility rates (78%), the inflation outlook (70%), falling marriage rates (67%), and energy costs (61%). On the flip side, builders identified meaningful tailwinds in the aging housing stock (73%), work-from-home trends (65%), artificial intelligence (52%), modular and panelized construction (45%), and the aging population (39%).

NAHB Chief Economist Robert Dietz noted that while fiscal pressures and demographic shifts pose real challenges, builders are finding growth opportunities in evolving work patterns and emerging construction technologies that could improve both productivity and affordability over the next ten years.

Zach Halaschak of the Washington Examiner reports that President Trump is downplaying the bipartisan 21st Century ROAD to Housing Act, calling housing “all about interest rates” and signaling he’s focused on bigger priorities, even as the bill faces an uncertain path in the House after passing the Senate last month. Trump criticized Fed Chair Jerome Powell and expressed confidence that mortgage rates, which have climbed to 6.45% after briefly dipping below 6% before the Iran war, will fall once the conflict ends. Notably, the legislation is designed to boost housing supply through deregulation and has no bearing on mortgage rates, and Trump himself has sent mixed signals on whether he actually wants home prices to come down, given the wealth impact on existing homeowners.

The White House also released its FY 2027 budget request on April 3, proposing a $10.7 billion cut to HUD (a 13% decrease), including the total elimination of the $3.3 billion CDBG program and $1.3 billion HOME Investment Partnerships Program. The budget also proposes two-year time limits on housing subsidies and mandatory work requirements, though Congress has historically rejected similar cuts.

Finally, Josh Boak of the Associated Press reports that the White House Council of Economic Advisers estimates the US is short 10 million homes, a figure laid out in the latest Economic Report of the President released April 13, with the administration arguing that regulatory cuts could unlock more construction, stabilize prices, and boost economic growth. Trump signed two executive orders in March directing federal agencies to reduce housing regulatory burdens and make it easier for smaller banks to provide mortgages, but the administration has been slow to take additional concrete steps, with housing messaging repeatedly sidelined by global distractions, including tariff fallout and the Iran war.