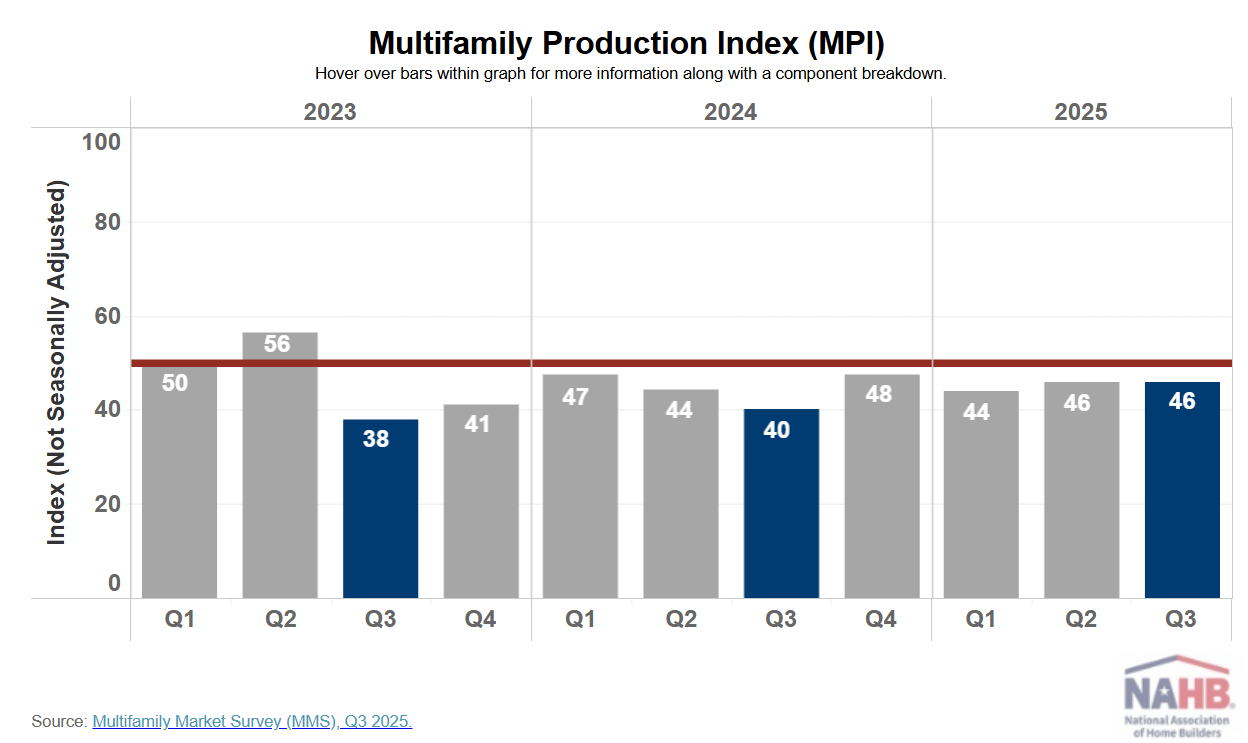

Eric Lynch of the National Association of Home Builders (NAHB) reports that confidence among multifamily developers improved year-over-year in Q3 2025, but remains negative overall. The Multifamily Production Index rose six points to 46 (still below the 50 “positive” threshold). At the same time, the Multifamily Occupancy Index slipped one point to 74, marking its lowest level since the survey was redesigned in the first quarter of 2023.

Source: NAHB (November 2025)

The market shows a sharp divide: low-rise and subsidized rental properties are strengthening (up to 51 and 55, respectively), while mid/high-rise and condo sectors lag (37 and 35). Occupancy remains solid across all segments, with subsidized units at 81%, garden/low-rise at 76%, and mid/high-rise at 66%. However, weakness is concentrated in high-density metro areas, as construction and demand shift toward lower-density markets.

Liezel Once of MPA reports that despite a slight year-over-year improvement in Q3 2025, multifamily developers remain under pressure as confidence continues to lag in high-rise and condo projects. The Multifamily Production Index rose to 46, with garden and low-rise properties the only segment in positive territory at 51. Mid- and high-rise sentiment climbed nine points yet stayed negative at 37, and condos reached just 35, reflecting the ongoing challenges of financing, rising construction costs, and regulatory hurdles.

Kim O’Brien of RealPage reports that apartment demand fell sharply behind supply in Q3 2025, with just 42,430 units absorbed—about half the decade’s average and well below the 105,525 new units delivered during the same period. The resulting 63,100-unit gap marks one of the steepest third-quarter imbalances in RealPage data since 1993, driven by softer employment, weaker consumer sentiment, and broader economic uncertainty. Despite the slowdown, strong leasing earlier in the year kept 12-month absorption high at 637,079 units, and with new supply easing from its 2024 peak, the market could rebalance in the near term.

Source: RealPage (November 2025)

Apartments.com reports that national multifamily rent growth continued to slow in October 2025, with average rents slipping 0.3% month-over-month to $1,708, marking the steepest decline in October in more than 15 years. It marks the fourth straight month of flat or negative rent change, with three of the five sharpest monthly drops in the past 15 years occurring within the last three months. Annual rent growth cooled to 0.8%, down from 0.9% in September and 1.5% at the start of 2025.

Julie Strupp of Multifamily Dive reports that state attorneys general are clashing with major landlords over nearly $142 million in proposed settlements tied to a 2023 price-fixing class action involving RealPage’s rent-setting software. AGs from Washington, D.C., Maryland, New Jersey, and Kentucky asked a federal judge to reject the 26 settlements, arguing they could undermine the states’ own enforcement actions against many of the same landlords. This includes Greystar, Bell, BH Management, Bozzuto, and other companies that deny wrongdoing. In a counter-filing, defendants accused the AGs of blocking resolution to pursue “duplicative damages” and additional legal fees. At the same time, the AGs argued they must protect the public interest and prevent inadequate settlements from being approved.

Jobs report

Jeff Cox of CNBC reports that the record-long government shutdown has halted the release of official labor data. Still, alternative indicators show a sharply slowing (yet not collapsing) job market. Economists estimate October’s nonfarm payrolls would have declined by 60,000, with unemployment rising to roughly 4.5%. ADP data showed just 42,000 jobs added, Challenger announced 153,074 layoffs (a 22-year October high), and ISM employment indexes for services (48.2%) and manufacturing (46%) signaled contraction. Small businesses are bearing the brunt: firms with fewer than 250 employees lost 34,000 workers in October, and Homebase data show that employment and hours worked are down 2.9% from January.

Cox notes that despite signs of cooling, state-level jobless claims remain steady (Goldman Sachs estimates 228,000 last week), and economists say the labor market looks weaker but still too stable to indicate the start of a recession.

Jake Krimmel of Realtor.com reports that, with the federal shutdown blocking a second consecutive month of official jobs data, alternative indicators suggest a cooling labor market, creating uncertainty that is spilling over into housing. The lack of “source of truth” data makes it harder for the Fed to gauge conditions, and markets now see a December rate cut as less likely. Treasury yields have inched up, suggesting mortgage rates may rise after recently hitting their lowest levels in over a year. Lower borrowing costs have offered buyers some relief, but affordability and confidence remain fragile, especially in federal-dependent markets like Washington, D.C., where the shutdown has slowed activity.

Indeed, Scott Horsley of NPR reports that the government shutdown leaves workers and policymakers relying on mixed signals from the private sector. Glassdoor finds employee confidence slipping, with job seekers less likely to reject offers, while Challenger counts 153,074 layoff announcements in October; the worst for that month in more than 20 years. Yet state jobless claims remain steady and ADP shows a modest increase in private payrolls, underscoring a labor market that is slowing but not collapsing. Workers in more vulnerable groups face sharper stress, with unemployment for 20–24-year-olds at 9.2% and for Black workers at 7.5%, a sign of a “two-speed” economy emerging beneath the surface.

Buyers and sellers

Manny Garcia of Zillow reports that the typical homebuyer is 42 years old, with Millennials making up the largest generational share at 35%. Younger buyers are active (21% are in their twenties or younger), while another 20% are in their sixties or older. Buyers remain disproportionately white: 66% identify as non-Hispanic white, compared to 60% of U.S. adults, while Black buyers represent just 9% despite making up 18% of the adult population. Regionally, 40% of buyers are located in the South, the nation’s largest housing market and the source of 55% of for-sale inventory, followed by the Midwest (26%), the West (23%), and the Northeast (12%).

Source: Zillow (November 2025)

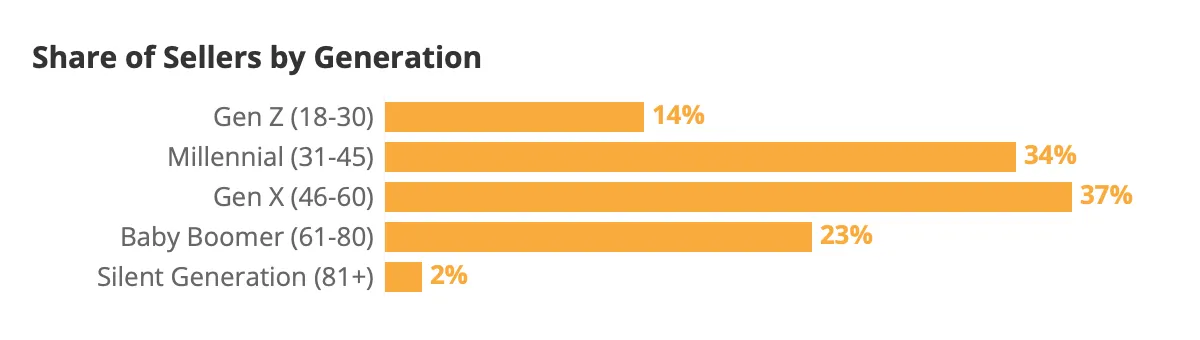

On the seller side, Garcia reports that the typical seller is 47 years old, falling between recent buyers and long-term homeowners. Sellers skew middle-aged (27% are 40–49 and 21% are 30–39), with Millennials (34%) and Gen X (37%) making up the bulk. Two-thirds of sellers are non-Hispanic white (68%), a higher share than their representation among U.S. adults (60%). Regionally, 41% of sellers are in the South, followed by the Midwest (22%) and the West (21%). Sellers also tend to have higher incomes, with a median household income ranging from $95,000 to $99,999, which is well above the national median of roughly $80,000.

Source: Zillow (November 2025)

Seller-buyers in the 30-39 and 40-49 age groups are most likely to buy a more expensive home (59% and 60% respectively), indicating a strong tendency to upgrade financially as they progress in their careers and potentially expand their families. Even the 18-29 age group shows a higher-than-average inclination (55%) to buy a more expensive home compared to the 50+ age group.

Dana Anderson of Redfin reports that pending home sales rose just 0.7% year over year in early November—the smallest gain in four months, as buyers remain cautious despite lower mortgage rates. Homes are taking a median of 48 days to go under contract, the slowest pace in October since 2019. The average rate has fallen to 6.17%, which is pushing the median monthly payment down to $2,508. However, rising home prices and economic uncertainty are keeping shoppers selective, with many holding out for the “perfect” deal. New listings are up 4% from last year, suggesting sellers are returning even as buyers tread carefully.