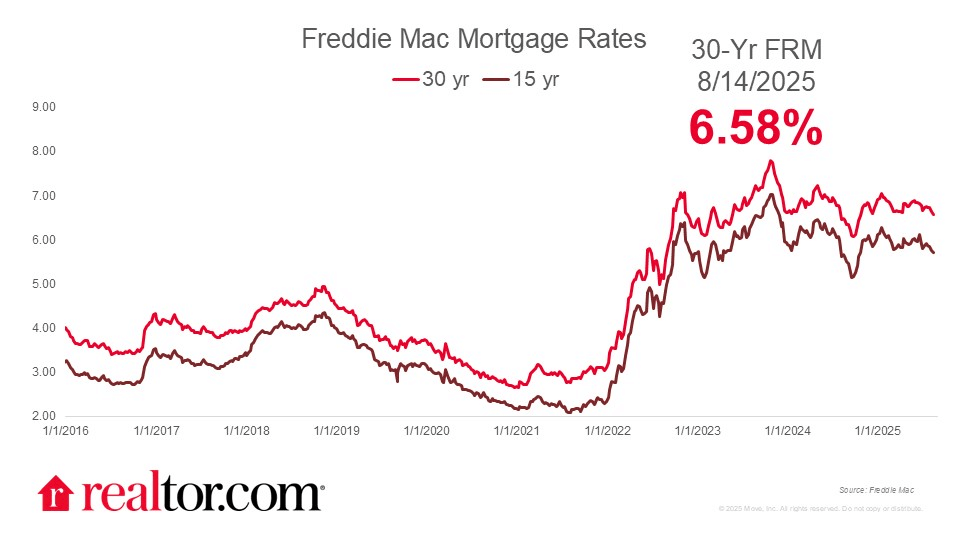

Joel Berner of Realtor.com reports that the Freddie Mac 30-year fixed mortgage rate ticked down five basis points to 6.58% this week, the lowest since October. Despite stubborn inflation data, this was driven by expectations of a Federal Reserve rate cut in September. While job market weakness previously fueled sharper declines, the latest CPI release showed topline inflation holding steady and core inflation accelerating, tempering momentum.

Source: Realtor.com (August 2025)

The 10-year Treasury yield held above 4.2%, reflecting bond market caution. For housing, the modest rate drop offers buyers some relief after a sluggish summer, and further Fed easing could spark a late-year buying surge, though mortgage rates remain higher than last year.

The Mortgage Bankers Association (MBA) also reports that mortgage applications surged 10.9% from the prior week on a seasonally adjusted basis, with the unadjusted index up 10%. Refinancing activity led the gains, jumping 23% from the previous week and 8% higher year-over-year. Further, purchase applications rose a modest 1% but remained 17% stronger than the same week in 2024.

Joel Kan, MBA’s Vice President and Deputy Chief Economist, comments:

“The 30-year fixed mortgage rate declined to 6.67 percent last week, which spurred the strongest week for refinance activity since April. Borrowers responded favorably, as refinance applications increased 23 percent, driven mostly by conventional and VA applications…Refinances accounted for 46.5 percent of applications and as seen in other recent refinance bursts, the average loan size grew significantly to $366,400. Borrowers with larger loan sizes continue to be more sensitive to rate movements.”

Kara Ng of Zillow notes that mortgage rates continue drifting lower, fueled by a weaker-than-expected labor market after July’s jobs report revealed sharp downward revisions to prior months. While CPI data showed tariffs nudging some prices higher, inflation largely matched expectations, keeping markets focused on growth concerns and boosting odds of Fed rate cuts ahead. For housing, affordability challenges persist, but shifting dynamics favor buyers: inventory is building, listings are lingering, and Zillow’s market heat index now classifies 27 major metros as neutral or buyer’s markets.

Ana Teresa Solá of CNBC explains that mortgage rates have been steadily declining thanks largely to falling 10-year Treasury yields rather than direct Fed policy. Despite the Fed holding its benchmark rate at 4.25–4.5% since December, weakening economic data has lowered bond yields, pulling mortgage rates down. Experts note this “substantial improvement” is creating refinancing opportunities, as refinance applications recently rose to their strongest pace in four weeks and now make up 42% of total mortgage activity.

Mark Worley of Redfin reports that the typical homebuyer’s monthly mortgage payment has dropped to $2,631, the lowest in seven months and down more than $200 from May’s $2,846 peak. Rates have now declined or held steady for 12 straight weeks, boosting affordability and giving a $3,000/month buyer about $20,000 more purchasing power compared to May’s 7.08% rate peak. With markets already pricing in a September Fed rate cut, Redfin’s Chen Zhao warns that waiting could backfire, as delayed buyers may miss today’s improved affordability window.

Multifamily update

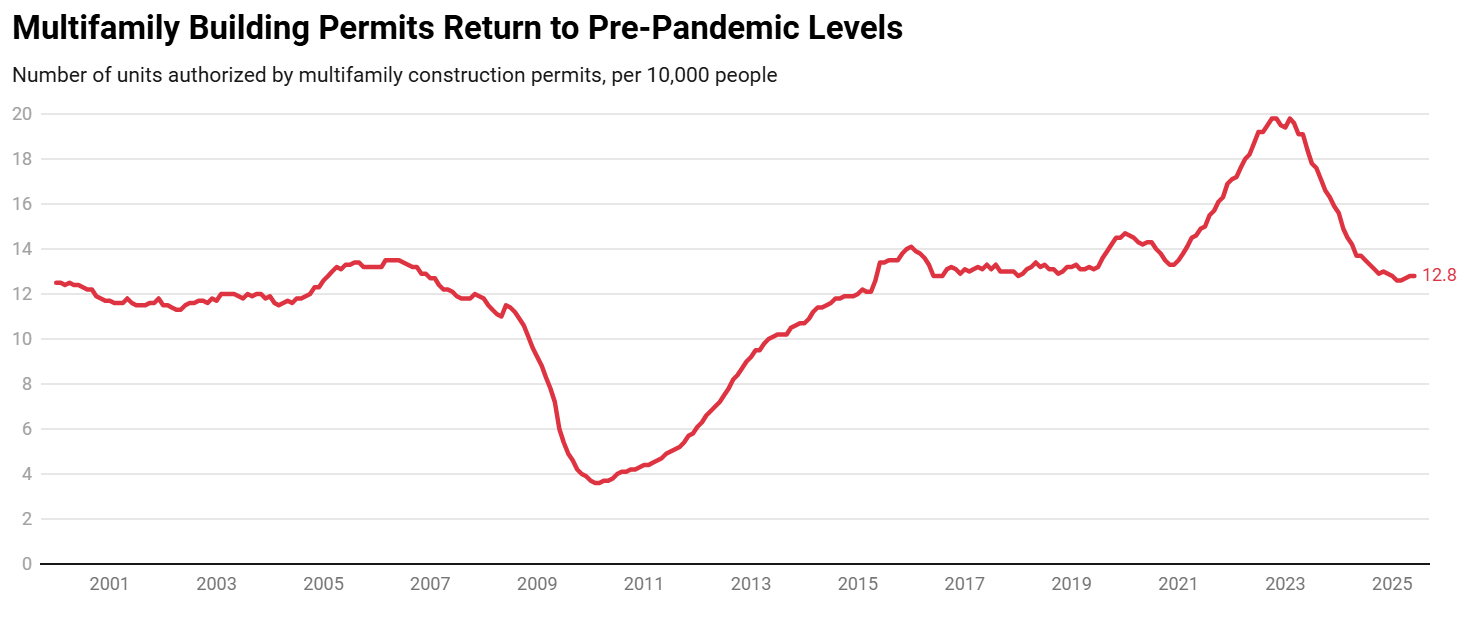

Lily Katz of Redfin reports that apartment construction permits have dropped 23% from the pandemic boom, with developers securing just 12.8 multifamily housing units per 10,000 people over the past year, down from 16.7 during 2020–2023 and even slightly below the pre-pandemic average of 13. Redfin’s analysis of Census Bureau data highlights stark regional differences: North Port, FL, and Austin lead in new multifamily permits, while Stockton and Bakersfield, CA, issue the fewest.

Source: Redfin (August 2025)

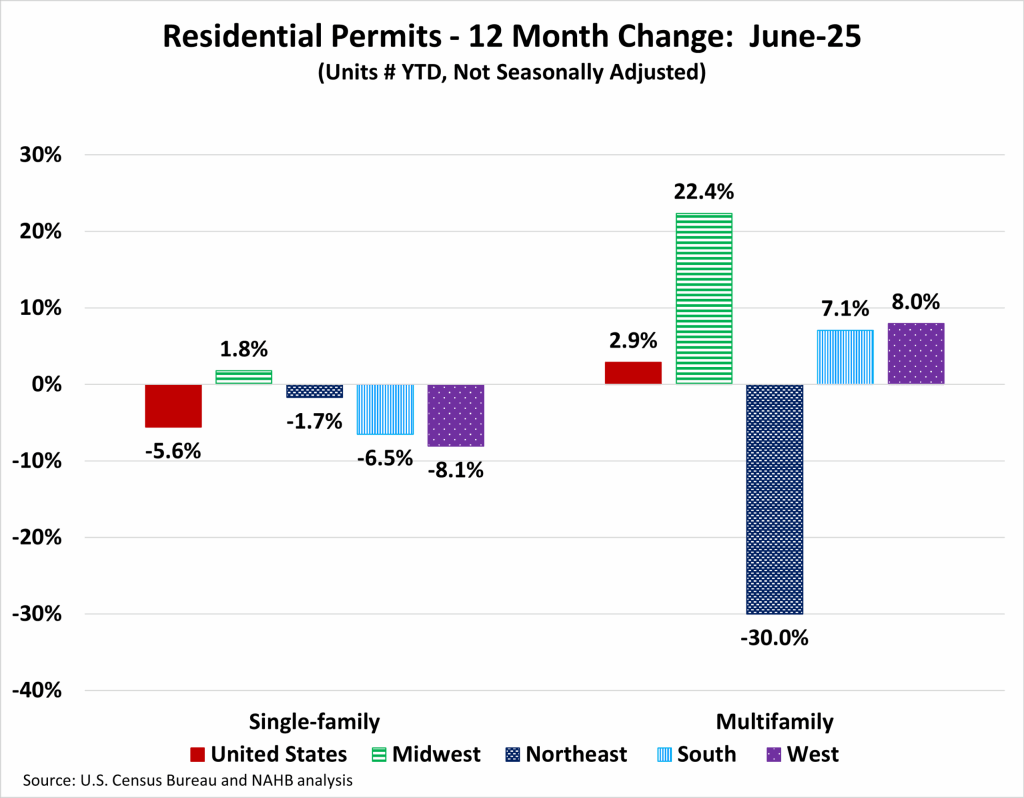

That said, Danushka Nanayakkara-Skillington of the National Association of Home Builders (NAHB) highlights that multifamily construction provided a rare bright spot in June 2025, with permits rising 2.9% year-over-year to 244,812 nationwide, even as single-family activity slumped. The growth was led by strong regional gains: the Midwest surged 22.4%, the West climbed 8.0%, and the South increased 7.1%. However, this momentum was offset by a steep 30% decline in the Northeast, mainly due to a 40% drop in the New York-Newark-Jersey City metro.

Source: NAHB (August 2025)

Kristen Smithberg of Globe St reports that rents have declined for two consecutive years, with July 2025 rents falling 2.5% year-over-year to a median of $1,712 for 0–2 bedroom units across the 50 largest markets. This year’s seasonal rent lift has been modest, with just 1.2% growth year-to-date versus 2.8% in 2024. Yet rents remain 17.4% above pre-pandemic levels, though now 2.7% below their August 2022 peak.

Alex Young of YieldPro reports that multifamily posted a record-breaking Q2 in 2025, with net absorption hitting 188,200 units, 47% higher than a year ago and 44% above the pre-pandemic Q2 average. With just 83,000 new units delivered, demand more than doubled supply, driving the national vacancy rate down 70 basis points to 4.1%, its lowest since before the pandemic. Over the past four quarters, absorption totaled 665,000 units versus 419,400 deliveries, creating a 58% supply-demand gap, the widest since the immediate post-pandemic recovery.

Finally, Leslie Shaver of Multifamily Dive reports that multifamily was the only major CRE sector to see rising delinquencies and servicing rates in July 2025, according to Trepp. Apartment CMBS delinquencies climbed 24 bps to 6.15%, more than double the 2.63% rate a year ago, while the multifamily special servicing rate jumped 19 bps to 8.37%, up from 5.11% last year. CRE delinquency rose to 7.23%, while the broader special servicing rate declined. Fitch Ratings also flagged apartment loans as a key driver of stress.

Foreclosures

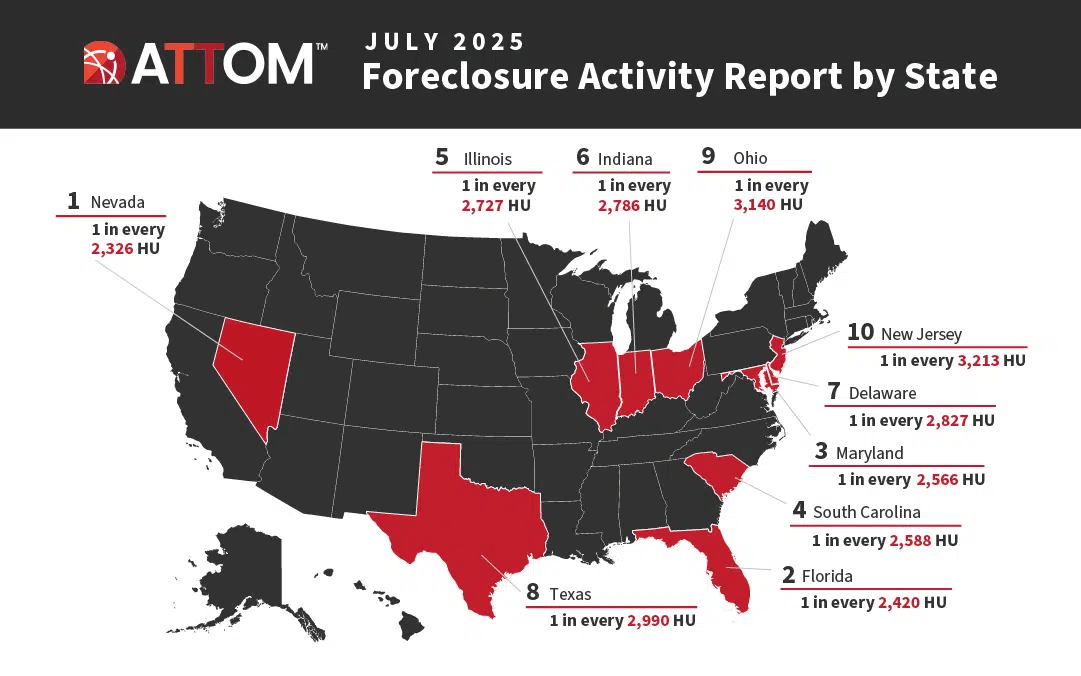

Megan Hunt of ATTOM Data Solutions reports that foreclosure activity rose in July 2025, with 36,128 properties facing filings, up 11% from June and 13% year-over-year, equating to one in every 3,939 housing units. Nevada had the highest foreclosure rate (1 in 2,326 units), followed by Florida, Maryland, South Carolina, and Illinois. New foreclosure starts totaled 24,302, marking a 12% monthly and 11% annual increase.

Source: ATTOM (August 2025)

ATTOM CEO Rob Barber comments: “July’s foreclosure activity continues to trend upward year-over-year, with increases in both starts and completions…While rising home prices are helping many owners maintain equity, the steady climb in filings suggests growing pressure in some markets.”

At the metro level, Bakersfield, CA (1 in 1,538), Cape Coral, FL, and Lakeland, FL recorded the worst foreclosure rates among midsize markets. At the same time, Houston (1 in 1,882), Jacksonville, FL, and Las Vegas topped large metros. CEO Rob Barber noted that while rising home prices are helping many owners preserve equity, the continued climb in filings points to mounting stress in specific markets.

“Overall, the July 2025 foreclosure data underscores a continued upward trajectory in activity, with notable increases in both starts and completions compared to last year. While strong home prices and equity levels may help many homeowners avoid foreclosure, the persistent rise in filings—especially in states and metros already facing higher rates—signals growing market stress that will be important to monitor in the months ahead.”

The National Mortgage Professional reports on how mortgage stress is mounting, with June delinquency rates rising nearly 5% month-over-month, the most significant mid-year jump since 2007. FHA loans remain weak, with the non-current rate up 25 bps year-over-year and delinquencies up 41 bps, marking the highest June level since 2013; more than half of all seriously delinquent U.S. loans are FHA-backed. Foreclosure activity is also climbing: it starts at 37% YoY, sales are at 18%, and active foreclosure inventory is at 10%, totaling 208,000 loans, though still 30% below pre-pandemic levels.