Dana Anderson of Redfin reports that housing activity slowed sharply heading into the holidays, with new home listings falling 1.7% year-over-year in the four weeks ending December 7, the steepest decline in more than two years. Pending sales also dropped 4.1%, the largest decrease in 10 months. Homes are taking longer to sell, with the typical property going under contract in 51 days, about a week slower than last year. Despite weak demand and continued economic uncertainty, prices are still rising: the median home sale price is up 2%, driven by a tightening inventory. Mortgage rates have eased to their lowest level in over a year but remain above 6%, continuing to weigh on buyer activity.

Diana Olick of CNBC reports that home prices have turned negative for the first time in over two years, down 1.4% over the past three months and less than 1% year-over-year nationally. Active listings in November were nearly 13% higher than in the same month the previous year, while new listings rose by just 1.7%, indicating a growing inventory but cautious sellers. Price declines are concentrated in specific markets (Austin (-10%), Denver (-5%), and Tampa and Houston (-4%)), while others like Cleveland (+6%) and New York (+5%) continue to rise. With mortgage rates stuck in a narrow range and demand still weak, prices are likely to remain soft.

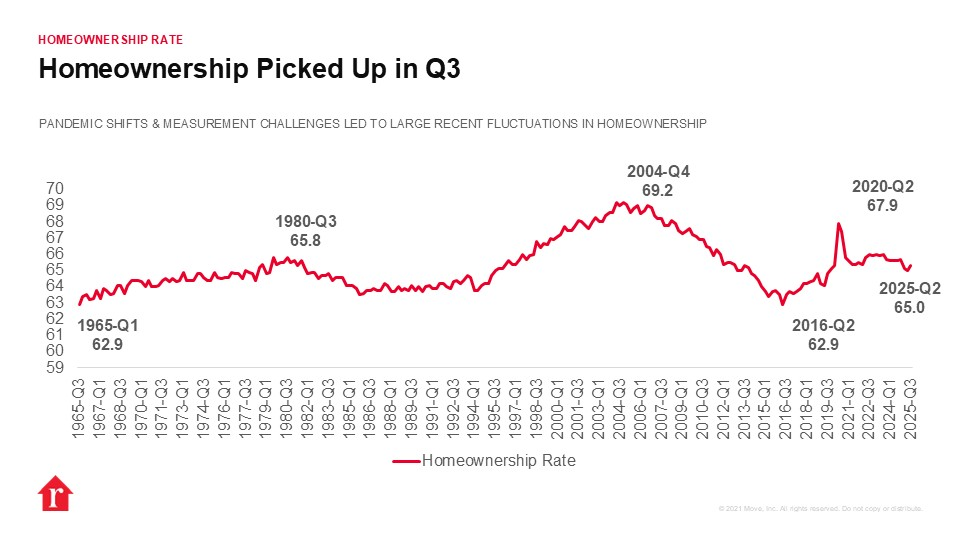

Hannah Jones of Realtor.com reports that the homeownership rate edged up to 65.3% in Q3 2025 (the highest level this year but still below its pandemic peak) helped by modest inventory gains, softer prices, and easing mortgage rates amid ongoing affordability challenges. The homeowner vacancy rate rose to 1.2%, up slightly from the previous quarter and year over year, although it remains well below pre-pandemic norms, signaling continued supply constraints. Rental vacancy ticked up to 7.1% and remains a key affordability outlet, with notable regional variation: the South leads in rental (9.1%) and homeowner vacancy (1.4%), while the Midwest posts the highest homeownership rate at 68.9%.

Source: Realtor.com (December 2025)

Na Zhao of the National Association of Home Builders (NAHB) comments on the data:

“Compared to the previous year, homeownership rates increased in three age groups. Among younger households, the homeownership rate for those under 35 increased 0.5 percentage points to 37.5% in the third quarter of 2025. This age group is particularly sensitive to mortgage rates and the inventory of entry-level homes. Householders ages 45-54 experienced a 0.3 percentage-point increase from 69.7% to 70%. Homeownership rates for householders aged 55-64 inched up by 0.1 percentage point over the same time. However, homeownership rates for householders aged 35-44 and those aged 65 years and over each declined 1.2 percentage points from a year ago.”

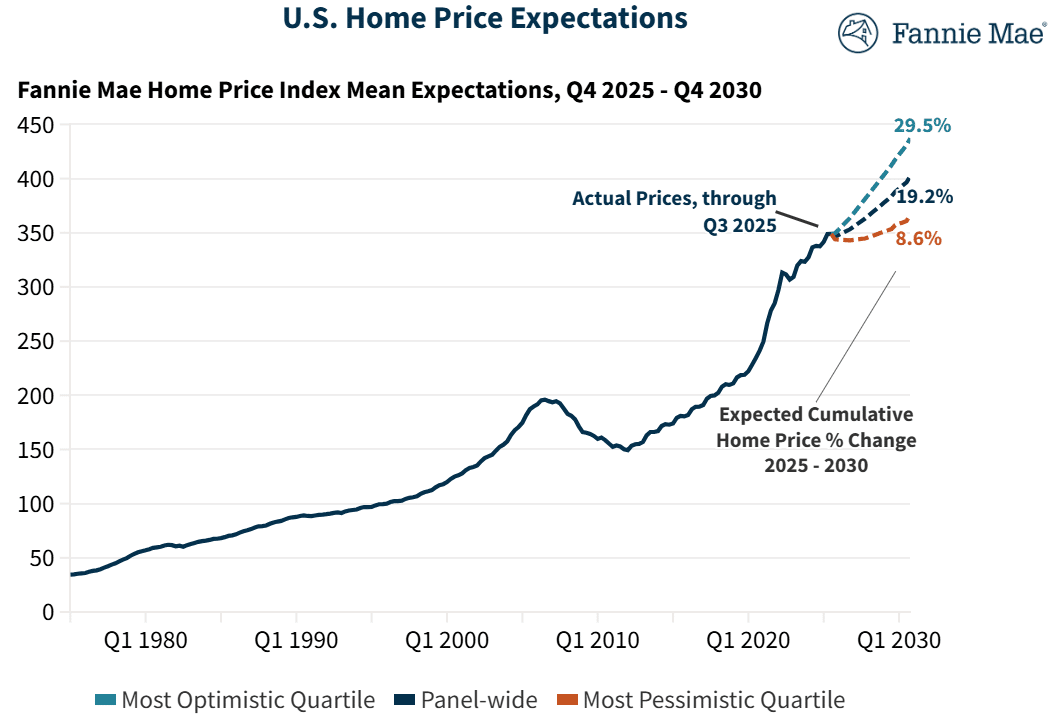

Fannie Mae reports that its Home Price Expectations Survey (HPES), which polls more than 100 housing experts, projects continued but modest national home price growth, with average annual increases of 2.6% in 2025, 2.0% in 2026, and 2.8% in 2027, based on the Fannie Mae Home Price Index.

Source: Fannie Mae (December 2025)

Regional news

Danielle Hale of Realtor.com identified Northeast and Midwest “value hubs” as the top housing markets for 2026, led by Hartford, Conn. (17.1% combined growth), Rochester, N.Y. (15.5%), Worcester, Mass. (15.0%), Toledo, Ohio (11.9%), and Providence, R.I. (11.2%). These markets are expected to outperform due to their relative affordability, limited new construction, and steady demand, with median list prices around $384,000, which is well below the national median of $415,000. This affordability attracts price-sensitive and out-of-state buyers from high-cost metros like New York, Boston, and Washington, DC.

Source: Realtor.com (December 2025)

Compass released its 2026 housing outlook, pointing to a more balanced national market, with regional dynamics driving very different experiences for buyers and sellers. Inventory is expanding most in the South and West, giving buyers more time and leverage, while parts of the North and Northeast remain tighter, with faster sales and firmer pricing. Affordability is set to improve modestly nationwide as home prices flatten (~0.5% growth), incomes rise faster, and mortgage rates ease into a 5.9%–6.9% range. Pent-up “shadow inventory” is largest in higher-cost, low-mobility markets. At the same time, demand remains strongest in relatively affordable metros, signaling a gradual thaw in mobility rather than a sharp price correction.

Mike Simonsen of HousingWire comments on the Compass report:

“For buyers, this means 2026 offers improved conditions compared to recent years, particularly in Sun Belt metros with elevated inventory. For sellers, realistic pricing from day one matters more than ever. For the broader market, patience is rewarded. The trajectory is finally moving in the right direction.”

Treh Manhertz of Zillow reports that affordability-driven demand reshaped housing search behavior in 2025, with Midwest and Northeast markets dominating Zillow’s most popular cities as buyers increasingly avoided high-cost coastal metros. Rockford, Illinois, ranked No. 1 nationally, with homes going pending in just five days and over 60% of interest coming from out-of-area shoppers, while other standout markets included Albany, NY; Dearborn and Toledo, OH; Carmel and South Bend, IN; and Springfield, IL, most with typical home values under $350,000. Even outside the Midwest, value hubs stood out, including Allentown, PA, and Abilene, TX, alongside a single West Coast entry, Berkeley, CA, underscoring that proximity to jobs, relative affordability, and faster-moving inventory were the key drivers of buyer interest in 2025.

Source: Zillow (December 2025)

Policy updates

The Real Deal reports that a rare bipartisan effort to boost housing supply stalled after House Republicans stripped the Senate-backed ROAD to Housing Act from the must-pass defense bill, sending the legislation into limbo. The package, backed by Senators Tim Scott and Elizabeth Warren and unanimously approved by the Senate Banking Committee, included zoning reform incentives, streamlined environmental reviews, and faster federal housing programs. House GOP leaders said they prefer a standalone bill aligned with their priorities, despite concerns that this move may delay action amid record housing costs. Industry groups, including the NAHB and NAR, expressed disappointment but remain hopeful that the bipartisan framework will resurface in 2026.

That said, Jonathan Delozier and Flávia Furlan Nunes of HousingWire report that the U.S. House has unveiled the Housing for the 21st Century Act, its version of the Senate-passed ROAD to Housing Act, in a rare bipartisan push to address housing supply and affordability. Sponsored by leaders from both parties, the bill targets incremental reform by easing regulatory barriers, modernizing federal housing programs, encouraging zoning updates, supporting smaller and manufactured homes, and giving local governments more flexibility. Industry groups say the changes won’t be transformational overnight, but could lead to meaningful improvements in housing production and affordability nationwide over time.

Flávia Furlan Nunes of HousingWire also reports that Fannie Mae rolled out a major Selling Guide update aimed at expanding access to affordable housing, including broader financing options for renovations and accessory dwelling units (ADUs), higher limits and expanded eligibility for manufactured homes, and updated requirements for adjustable-rate mortgages (ARMs). The policy changes are designed to enhance market liquidity and provide lenders and borrowers with more flexibility, particularly for lower-cost housing solutions and property improvements.

Finally, Robert Dietz of NAHB explains that last week’s Federal Reserve cut was a form of “insurance” against labor market weakening rather than inflation risk. The Fed also announced purchases of short-term Treasurys to support market functioning, a move explicitly separated from rate policy. The decision revealed rare internal division, with two members favoring no cut and one pushing for a larger 50-basis-point reduction; the most dissent since 2019. Policymakers acknowledged slowing job gains, a rising unemployment rate, and continued weakness in housing, with Chair Powell emphasizing structural undersupply, homeowner lock-in, and persistent affordability challenges despite inflation easing but remaining above target.