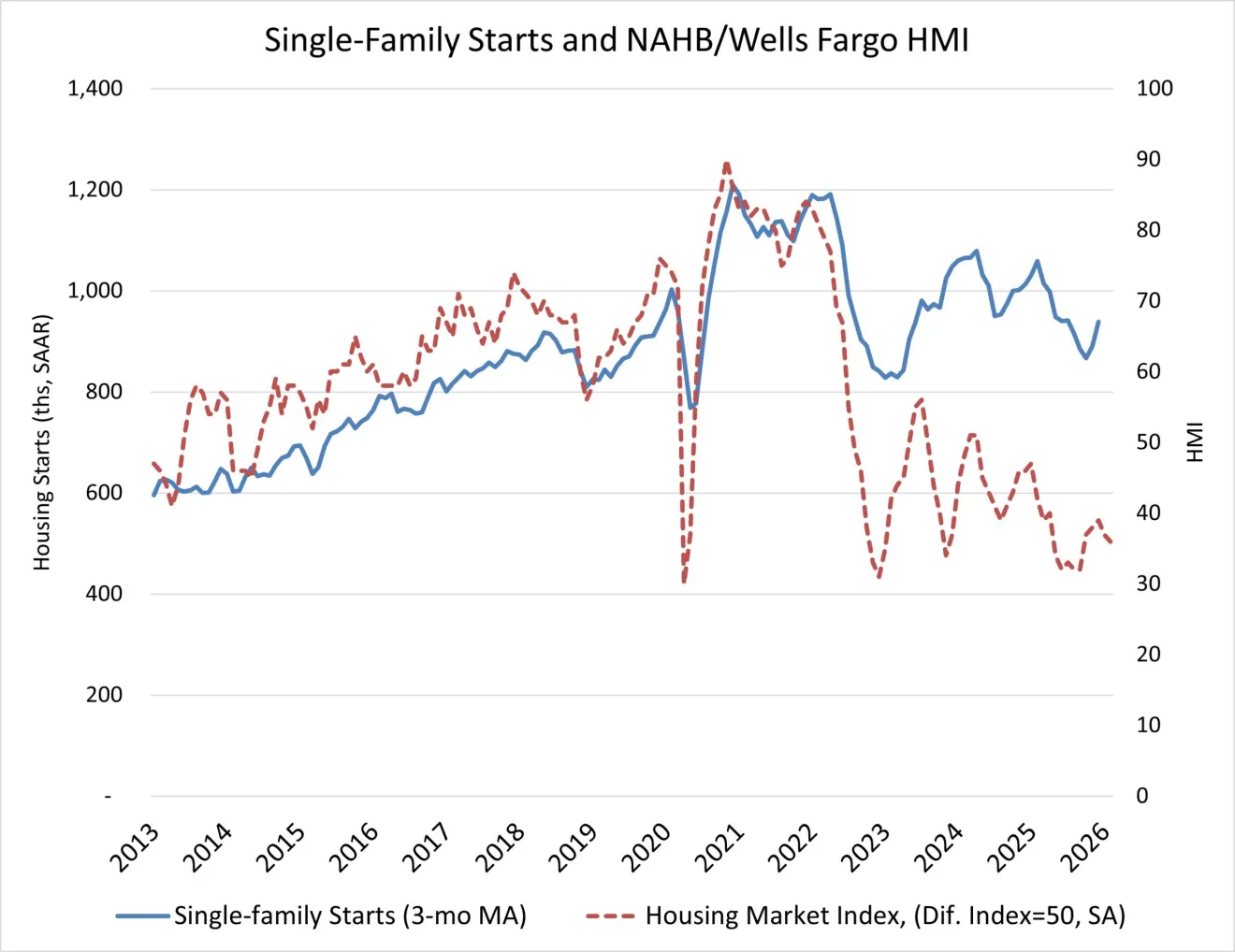

Orphe Divounguy of Zillow reports that housing activity closed 2025 with a modest rebound but a clear shift in builder strategy. Building permits rose to a seasonally adjusted annual rate of 1.45 million in December, up 4.3% from November but down 2.2% year over year, while housing starts climbed to 1.40 million, a 6.2% monthly gain yet still 7.3% below December 2024. Single-family permits fell sharply to 881,000, down 10.9% from a year earlier, and single-family starts, at 981,000, were up 4.1% month over month but 9% lower than a year earlier. Over the full year, single-family construction dropped 6.9%, while multifamily units in buildings with five or more units jumped 18%, signaling that builders are leaning harder into higher density even as rent growth cools.

Jing Fu of the National Association of Homebuilders (NAHB) reports that housing construction barely moved in 2025, with total starts slipping 0.6% to 1.36 million units from 1.37 million in 2024, as affordability pressures dragged on single-family building. Single-family starts fell 6.9% to 943,000 for the year, while multifamily activity jumped 17.4%, underscoring the ongoing pivot toward rentals and higher density. December provided a late boost, with overall starts rising 6.2%, as noted above. Single-family climbed 4.1% to 981,000, its strongest pace since February 2025, and multifamily surged 11.3% to a 423,000-unit rate, closing the year with unexpected momentum.

Source: NAHB (February 2026)

Danushka Nanayakkara-Skillington, also of NAHB, writes that new home sales closed 2025 with steady demand but heavy use of incentives. December sales dipped 1.7% month over month to a 745,000 seasonally adjusted annual rate, yet were 3.8% higher than a year earlier. For the full year, an estimated 679,000 new homes were sold, down 1.1% from 686,000 in 2024. Builders leaned hard on concessions, with 67% offering incentives in December, the highest share since the pandemic, and cutting prices by an average of 5%. The data suggests buyers are still active, but affordability pressures are forcing builders to negotiate to keep deals moving.

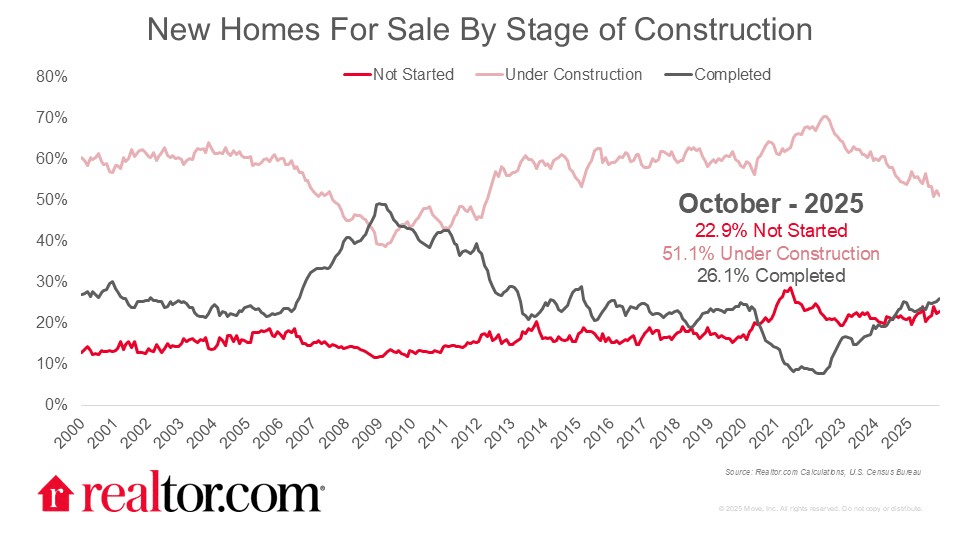

Joel Berner of Realtor.com highlights a market that quietly shifted from oversupplied to balanced by year’s end. While 2025 sales totaled 679,000 homes, down 1.1% from 2024, December’s pace ran 3.8% above a year earlier, and months of supply tightened from 8.2 to 7.6 as inventory fell 3.5% year over year. The median new-home price dropped 2% to $414,400, and affordability gains were most visible at the lower end, with homes under $300,000 rising to 18% of sales and 66% of December purchases priced below $500,000. Regionally, the Midwest surged 30.1% year over year in December, and the Northeast climbed 12.1%, even as the South dipped slightly. Builders are also adjusting tactics, listing more unstarted homes while keeping completed inventory steady, signaling confidence in demand but caution about breaking ground too fast.

Source: Realtor.com (February 2026)

“Builders are taking notice of the boosted demand for new homes and are listing more unstarted homes in December than they did in all of 2025. In a period when they face significant uncertainties, builders want to capitalize on current buyer demand and make sales before beginning construction of new homes. The number of homes under construction for sale fell to a 2025 low in December, while the number of completed homes held steady.”

Mortgage rates

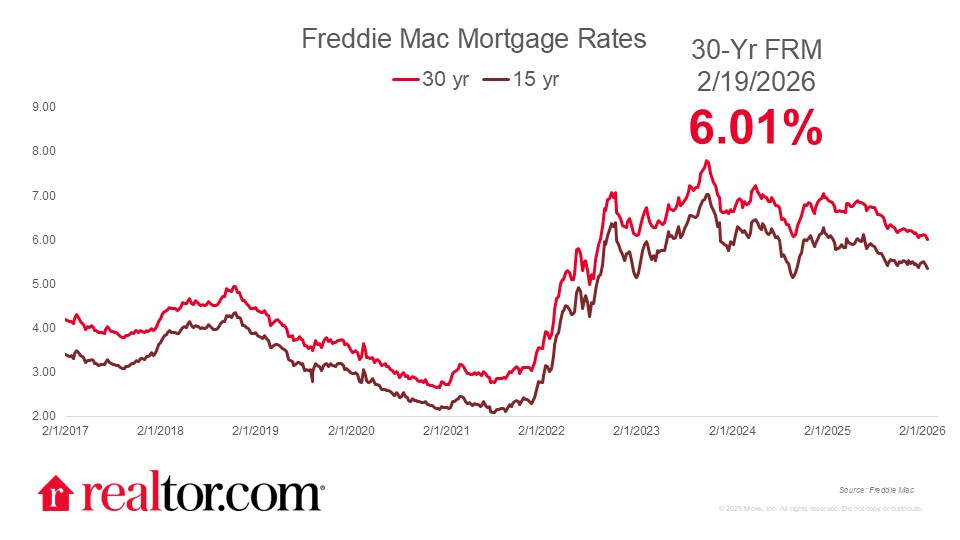

Jake Krimmel of Realtor.com reports that the average 30-year fixed mortgage rate fell to 6.01%, its lowest level since September 2022, down from 6.09% last week and well below 6.87% a year ago. Rates were near 6.6% just six months back, making this a meaningful shift tied to a drop in the 10-year Treasury yield after softer inflation data. Early demand is responding, with pending home sales up 1.2% year over year in January, the strongest gain since late 2024. Still, Fed minutes signal policymakers could turn hawkish again if inflation stalls, and with inventory growth slowing and new construction trailing last year, cheaper financing may boost competition as much as affordability.

Source: Realtor.com (February 2026)

Hal Bundrick of Yahoo! Finance reports on record-low mortgage rates amid geopolitical tensions and lingering inflation concerns that are rattling markets. Beyond homebuying, the bigger shift is in refinancing: Freddie Mac notes refinance applications have more than doubled over the past year, and the Mortgage Bankers Association saw another weekly increase. Economists say only a narrow band of borrowers with higher legacy rates are jumping in so far, but a sustained move below the 6% psychological line could unlock broader activity and put real cash flow relief back into homeowners’ pockets.

Sam Khater, Freddie Mac’s chief economist, comments on the rate decrease: “This lower rate environment is not only improving affordability for prospective home buyers [but] it’s also strengthening the financial position of homeowners…Over the past year, refinance application activity has more than doubled, enabling many recent buyers to reduce their annual mortgage payments by thousands of dollars.”

Liezel Once of MPA reports that the dip in mortgage rates, well below 6.87% a year ago, sparked a fresh burst of refinancing even as purchase demand softened. Refi applications jumped 7% week over week and were 132% higher than the same week last year, pushing refinances to 57.4% of total mortgage activity, the strongest showing since mid-January. Meanwhile, the purchase index fell 3% on the week and is only 8% above year-ago levels, with VA loans a rare bright spot. The data shows rate sensitivity is alive and well, but buyers remain constrained by affordability and thin inventory.

Lawsuits and policy changes

Eric Heisig of Bloomberg reports that the Ohio Supreme Court delivered a major win to Rocket Mortgage, ruling that a 2023 state law blocking class actions over pandemic-era errors in recording mortgage satisfaction documents applies retroactively. The decision, issued in a 6 to 1 split on key points, dismantles a proposed class seeking statutory damages and limits the case to the lead plaintiff’s individual claim of $250. By enforcing the retroactive ban even though it was passed after the lawsuit was filed, the court effectively shields lenders from broader liability tied to Covid-era filing mistakes, narrowing exposure to small, one-off claims rather than potentially costly class payouts.

Sarah Wolak of HousingWire reports that the Supreme Court, in a 6 to 3 decision, struck down “reciprocal” tariffs, ruling that the International Emergency Economic Powers Act does not give a president unilateral authority to impose broad import duties. For real estate, the immediate question is construction costs: the decision overturns tariffs of up to 34% on China and a 10% baseline on many other countries, as well as a 25% tariff on certain goods from Canada, China, and Mexico, though steel and aluminum tariffs remain in place under other laws. While the ruling reinforces that Congress controls taxation, economists caution that it will not meaningfully lower building costs in the short term, as supply constraints, labor shortages, and financing pressures continue to weigh on homebuilders.

Brooklee Han of HousingWire reports that a group of 18 Democratic lawmakers, led by Sen. Elizabeth Warren and Rep. Becca Balint, are pressing the Department of Justice for details on its antitrust review of the $1.6 billion Compass and Anywhere Real Estate merger. In a letter to Attorney General Pam Bondi, they question whether the review adequately addressed risks to competition and housing affordability, and whether any political or industry pressure influenced the outcome. From a real estate standpoint, the concern is market concentration: a combined brokerage giant could wield greater control over listings, agent commissions, and local market share, potentially reshaping competition at a time when consumers are already grappling with high home prices and limited inventory.

Tristan Navera of Realtor.com reports that Illinois Gov. JB Pritzker is pushing a sweeping statewide zoning reform under a new initiative called BUILD as part of a $56 billion budget, aiming to unlock more housing by legalizing duplexes, triplexes, four flats, and ADUs while cutting parking mandates and streamlining permits. The backdrop is stark: Illinois is already 142,000 homes short and needs 227,000 new units by 2030, or roughly 45,000 per year, to meet demand. A University of Illinois report highlights the gap, and Realtor.com gives the state a C on affordability.

Dani Romero of CoStar reports that the White House clarified President Trump’s proposed ban on institutional investors buying single-family homes, defining “large institutional investors” as entities owning 100 or more houses, including REITs and funds. Only 6.3% of single-family investors would be affected under that threshold, according to John Burns Research and Consulting. Build-to-rent projects, existing holdings, and certain distressed purchases would be exempt, and the ban would apply only to future deals. Large landlords argue they are adding supply, not crowding out buyers, while the proposal’s fate remains uncertain in Congress.

Finally, Jonathan Delozier of HousingWire reports that Kentucky lawmakers advanced Senate Bill 51, a proposed constitutional amendment that would freeze property tax assessments for homeowners age 65 and older by locking in the value of their primary residence. Seniors would continue paying taxes, but on the frozen assessment rather than rising valuations. The measure, sponsored by Sen. Mike Nemes, must win three-fifths support in both legislative chambers before heading to voters in November. Supporters say it offers relief to fixed-income homeowners, while policy analysts warn that broad tax freezes could squeeze funding for schools and local governments that rely heavily on property tax revenue.