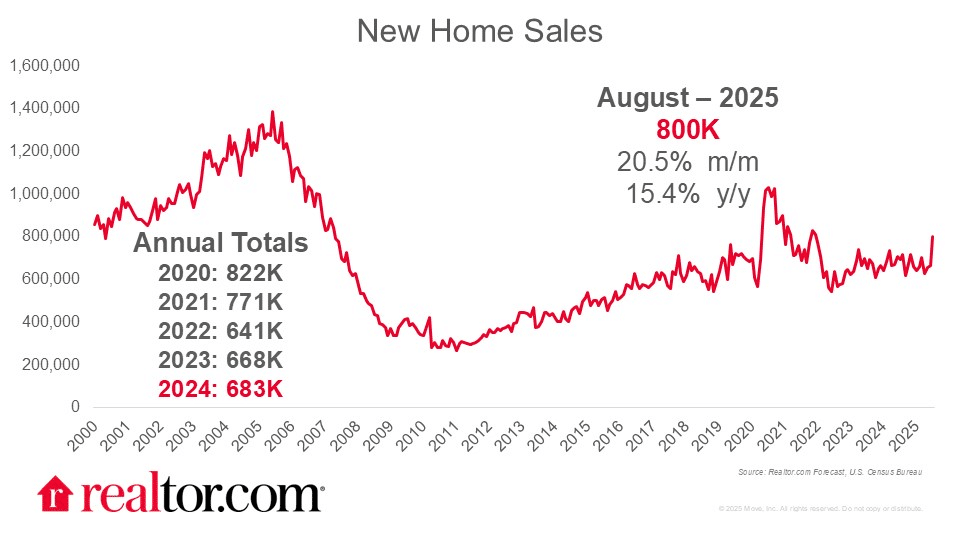

Orphe Divounguy of Zillow reports that new single-family home sales surged by 20.5% in August, reaching 800,000 (SAAR), surpassing expectations and marking a 15.4% increase from August 2024. The median price of new homes rose by 1.9% year-over-year to $413,500. The supply of new homes for sale dropped to 490,000, equating to 7.4 months of inventory, down from 9.0 months in July. This uptick in sales was driven by falling mortgage rates and increased builder incentives, with 66% of builders using incentives in August.

Anthony Smith of Realtor.com reports that the new-home sales surge is the strongest sales pace in 2025. This increase was driven by gains across all regions, with the Northeast leading at 72.2%. As noted, the median price for a new home rose as more sales occurred in higher price ranges, narrowing the gap between new and resale homes. Builders are focusing on maintaining a lean stock of unsold homes, aware of ongoing affordability challenges, but remain cautiously optimistic heading into the fall.

Source: Realtor.com (September 2025)

Diana Olick of CNBC highlights that the surge in new home sales was the largest gain since August 2022, marking a significant rebound in the housing market. Despite mortgage rates hovering at 6.63% throughout the month, builders have offered more substantial incentives, with 39% reporting price cuts in September, the highest since the pandemic’s end. The strong sales, particularly in the Northeast and South, are attributed to builders’ incentives and the tight inventory in certain regions.

The National Association of Home Builders (NAHB) reported that builder confidence in newly built single-family homes remained low in August, with the Housing Market Index (HMI) holding steady at 32, which has persisted for 16 months. Despite slight gains in some regions, elevated mortgage rates, weak buyer traffic, and supply-side challenges continue to drag on sentiment. Affordability remains a key concern, with many buyers waiting for mortgage rates to drop before moving forward. In response, 37% of builders reported price cuts, and 66% used sales incentives—both of which have been consistent for the past few months.

Compass-Anywhere

Keith Griffith of Realtor.com reports that Compass Real Estate has announced a $1.6 billion acquisition of Anywhere, which will make it the world’s largest residential real estate brokerage. The all-stock deal, valued at $10 billion, will bring Compass under its umbrella brands like Century 21, Sotheby’s, and Coldwell Banker. The merger aims to expand Compass’ global reach, now covering 120 countries and employing 340,000 real estate professionals. Compass has seen growth despite a weak U.S. housing market, reporting a 21% increase in transactions and $2.06 billion in revenue for Q2.

In a press release, Compass CEO & Founder Robert Reffkin comments on the merger:

“Today marks a monumental step towards our mission to empower real estate professionals with everything they need to grow their business and better serve their clients…I have deep respect for Anywhere’s leadership, agents, employees, culture, and brands. By bringing together two of the best companies in our industry, while preserving the unique independence of Anywhere’s leading brands, we now have the resources to build a place where real estate professionals can thrive for decades to come.”

Tracey Velt of HousingWire reports that the merger between Compass and Anywhere transforms the real estate landscape, with 340,000 agents and 15% to 20% of U.S. sales volume. While the focus has been on the companies’ expanded market share, industry experts believe the real challenge lies in managing internal dynamics. The merger brings together two companies that have long competed for talent and market share, raising concerns about cultural integration, agent retention, and whether agents will see more opportunities or face increased uncertainty in the newly consolidated organization.

Brooklee Han, also of HousingWire, reports that Compass’s acquisition of Anywhere is reshaping the MLS (Multiple Listing Service) industry, signaling a shift towards innovation for MLSs to stay competitive. The merger combines the nation’s largest brokerage by sales volume with the second-largest by transaction sides, creating a robust global network of 340,000 agents. This acquisition positions Compass to potentially build an exclusive listing platform that could challenge the traditional MLS system. As Compass grows its exclusive listings, MLS leaders must adapt, evolving beyond just listing data to maintain relevance and competitiveness in the changing real estate landscape.

Finally, Matt Carter on Inman reports that the acquisition is now under scrutiny by antitrust regulators, with the deal expected to give the merged companies a combined market share of 18%. The merger has raised concerns about reduced competition, particularly regarding the potential for Compass to leverage its new size to disadvantage smaller competitors and limit consumer choice. Critics fear that this merger could erode market transparency. The deal is also subject to shareholder approval and regulatory review, with Compass expected to assume $2.6 billion in Anywhere’s debt.

Rent update

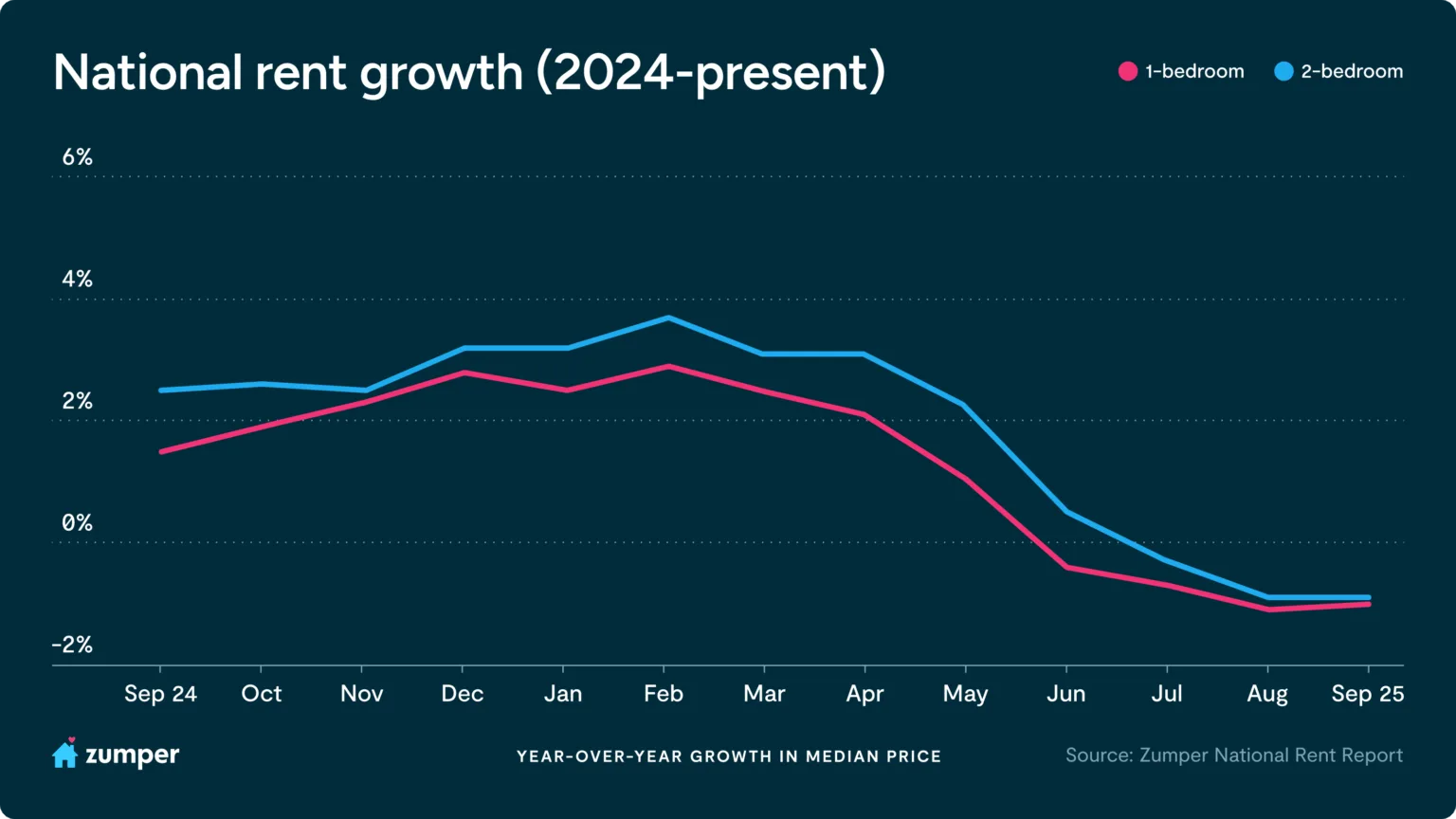

Crystal Chen and Quentin Proctor report that Zumper’s National Rent Index shows a third month of flat or declining rent prices. In September, one-bedroom rents remained steady at $1,517, while two-bedroom rents decreased by 0.2% to $1,894. Both unit types are down 1% year-over-year. San Francisco saw significant rent growth, with one-bedroom rents surpassing $3,500 for the first time since the pandemic, while two-bedroom rents exceeded $5,000. Major cities in the Mountain Region, like Salt Lake City, experienced notable annual declines, with one-bedroom rents dropping 11.1%. New York City remains the most expensive market, with slight rent increases, while most other top markets saw annual declines, including Jersey City, Miami, and Los Angeles.

Source: Zumper (September 2025)

Anthemos Georgiades, CEO of Zumper, comments:

“National rent prices have cooled over the past few months as the rental market continues to recalibrate…A combination of cautious renter demand amid economic headwinds, ample inventory on the market, and a labor market that’s losing momentum have eased the pressure on rents we saw earlier this year.”

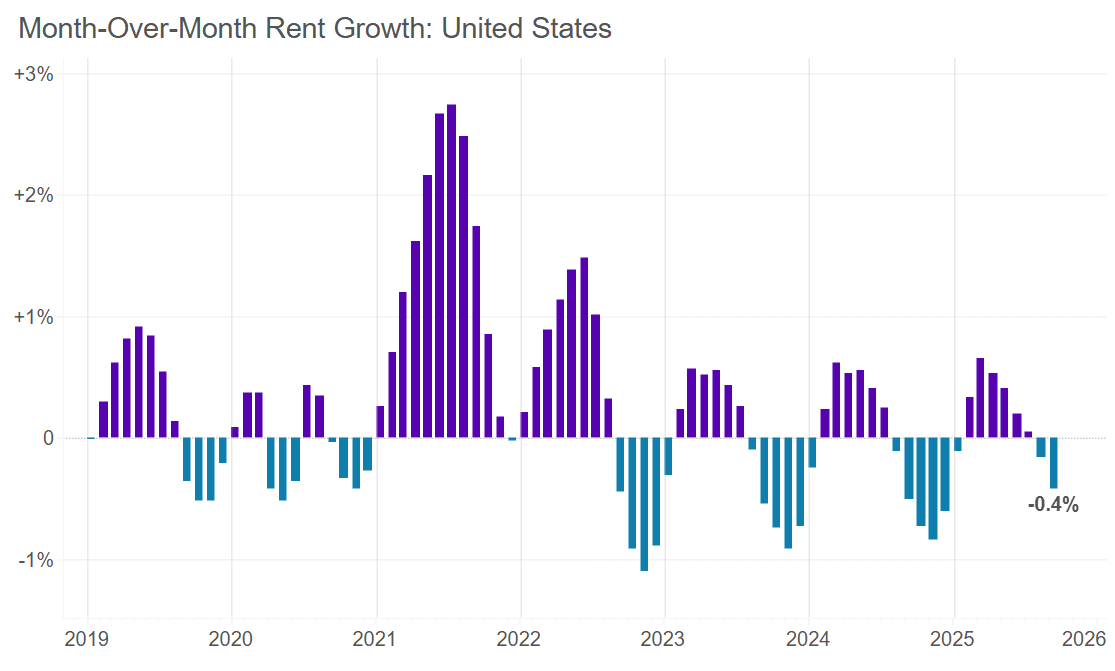

Apartment List reports that national median rent fell by 0.4% in September, marking the second consecutive monthly decline as the rental market enters off-season. Year-over-year, rent prices are down 0.8%, but there was a slight uptick in growth compared to previous months. The national multifamily vacancy rate has risen to 7.1%, the highest recorded in the index, as a surge in multifamily construction slows and more units hit the market.

Source: Apartment List (September 2025)

On average, units take 31 days to lease, a two-day increase from last month. Austin is experiencing the softest rental market, with rents down 6.5% year-over-year, while San Francisco has seen the highest rent growth at 4.9%. With the seasonal slowdown, rent prices are expected to continue declining through the end of the year.

“As more vacant units have come onto the market, those units have also been sitting vacant for somewhat longer. Our time on market index tells us how long it takes for units to get leased after they are first listed on our platform. The typical “list-to-lease” time peaked at 37 days nationally in January, an all-time high going back to the start of the data series in 2019. We have since come down from that peak, but September saw time on market tick up for the third consecutive month, increasing from 29 days in August to 31 days this month.”

Jiayi Xu and Danielle Hale of Realtor.com report on the ongoing rent declines across the U.S., with a slight dip in asking rents for 0-2 bedroom properties, marking two years of rent decreases. However, renters remain active, with a notable rebound in mobility and optimism about future homeownership. Here are some additional highlights:

- August 2025 marked the 25th consecutive month of year-over-year rent declines for 0-2 bedroom properties.

- Asking rents dipped by $38 (-2.2%) year-over-year, with the median asking rent in the 50 largest metros at $1,713.

- The median rent for studios, 1-bedroom, and 2-bedroom properties all declined: studio rents at $1,430 (-1.7%), 1-bedroom at $1,593 (-2.1%), and 2-bedroom at $1,897 (-2.2%).

- Renters are increasingly looking for more space, affordability, and a change in neighborhood, with a significant rebound in renter mobility in 2023 and 2024.

- Nearly 60% of renters are optimistic about homeownership, with over half planning to purchase within the next 1-2 years.