As a lead-up to Super Bowl 2026, many real estate outlets released reports on housing markets in Seattle and Boston. Anthony Smith of Realtor.com compared Boston and Seattle’s luxury housing markets and finds similar mid-field pricing but sharply different high-end dynamics: median listing prices sit close at $760K in Boston and $730K in Seattle (vs. a $399.9K U.S. median), and both markets have deep seven-figure inventory with million-dollar listings comprising 33.9% of Boston’s and 28.4% of Seattle’s stock (U.S.: 12.0%), roughly 2,400 listings each per month. The divergence shows up at the luxury entry point, where Seattle’s 90th-percentile threshold is $1.70M (43% above the U.S. luxury benchmark of $1.19M) while Boston’s jumps to $2.57M, about 51% higher than Seattle and more than double the national mark.

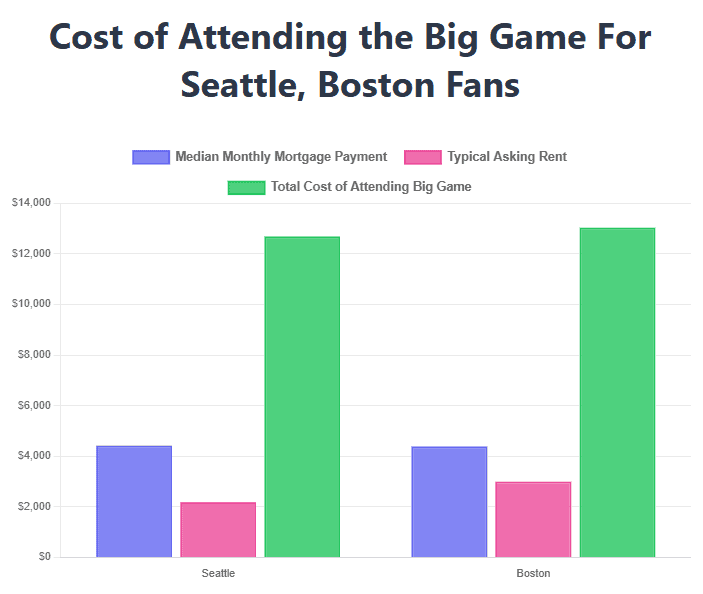

Dana Anderson of Redfin reports that attending this weekend’s big game would cost Seattle and Boston fans roughly the equivalent of three monthly mortgage payments, underscoring the gap between housing costs and major-event travel. For two people, the all-in trip totals $12,681 from Seattle and $13,031 from Boston (covering tickets, airfare, and lodging near Levi’s Stadium) versus median monthly mortgage payments of about $4,500 in Seattle and $4,200 in Boston.

Source: Redfin (February 2026)

Sarah Wolak of HousingWire reports that Rocket Companies and Redfin launched their first-ever joint national Super Bowl ad (also Redfin’s first Super Bowl appearance in its 20-year history), spotlighting community, neighborliness, and the emotional realities of moving. The 60-second spot, titled “America Needs Neighbors Like You,” aired in the second quarter of Super Bowl LX and anchors the second season of Rocket’s “Own the Dream” campaign. Set to a reimagined version of “Won’t You Be My Neighbor?” by Lady Gaga (originally popularized by Fred Rogers), the ad follows two teenage girls from different backgrounds whose lives intersect after major family transitions, reinforcing the brands’ shared message that housing decisions are about people and support systems, not just transactions.

Lillian Dickerson of Inman reports that Redfin is leveraging Super Bowl buzz with “The Great American Home Search,” a Super Bowl LX–adjacent, app-exclusive game that gives users a chance to win a furnished home valued at more than $1 million. Launched on Sunday, Feb. 8 (immediately after a joint ad with Rocket Companies airs during Super Bowl LX), the 48-hour experience releases six clues that players must solve using Redfin’s search tools to identify the featured home. The first eligible participant to crack all clues wins the property, plus additional cash to help cover taxes and insurance.

Zillow Research translates Super Bowl–level salaries into housing power and finds that even the lowest-paid players in the matchup between the Seattle Seahawks and the New England Patriots can shop in the multimillion-dollar range. Using the standard affordability rule of spending up to 30% of income on housing with a 20% down payment, Zillow estimates the highest-paid player (a New England offensive lineman earning $12M) could afford a $47.1M home, while Seattle’s top earner (a $5.35M cornerback) lands near $21.6M. At quarterback, the contrast is stark: New England’s starter at $960K maps to ~$3.8M homes, versus Seattle’s $5.3M starter at ~$21.4M. Even at the lower end, players earning ~$600K–$840K can still afford homes priced at $2.3M–$ 3.3 M.

Mortgages

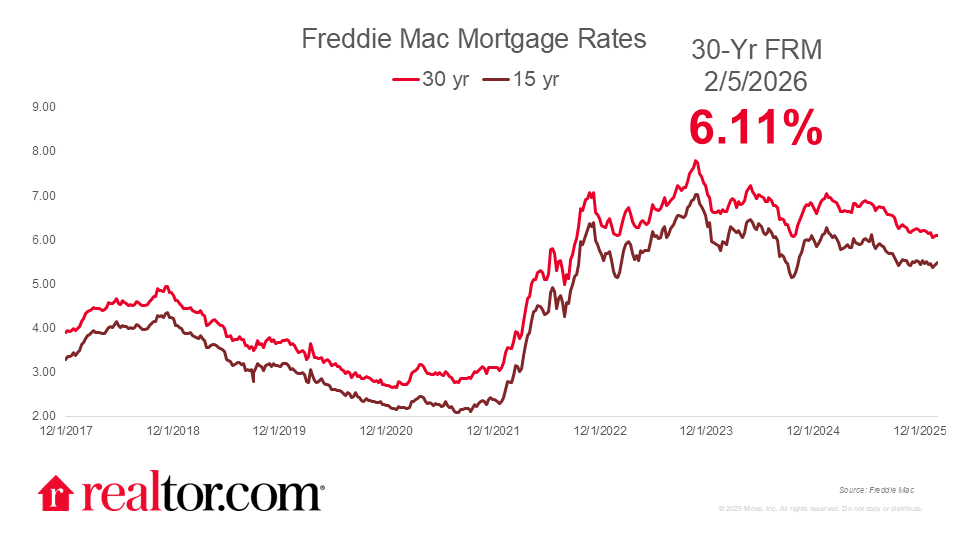

Anthony Smith of Realtor.com reports that the Freddie Mac 30-year fixed mortgage rate held steady at 6.11% this week, essentially unchanged (up 1 basis point) despite the Federal Reserve holding policy rates flat at its January meeting. Attention shifted to policy credibility following the nomination of Kevin Warsh as the next Fed chair, underscoring that mortgage rates are driven by long-term yields and investor expectations rather than solely by the Fed. Smith notes that if markets question the Fed’s independence or inflation-fighting resolve, long-term yields (and thus mortgage rates) can rise even during a rate-cutting cycle, meaning calls for aggressive cuts won’t translate into cheaper mortgages unless confidence in monetary policy remains intact.

Source: Realtor.com (February 2026)

Kara Ng of Zillow reports that after brief mid-January volatility, 30-year fixed mortgage rates have settled back near their 2025 lows, largely unmoved even by the January 28 Federal Reserve policy meeting, where Chair Jerome Powell left rates unchanged amid signs of stabilizing unemployment. Market expectations for no near-term changes increased, while the 10-year Treasury yield (closely tracked by mortgage rates) remained little changed; the next potential catalyst, the Bureau of Labor Statistics jobs report, was delayed due to a partial government shutdown. Looking ahead, Zillow forecasts a gradual glide path toward ~6% mortgage rates by the end of 2026, with risks from policy shocks.

Diana Olick of CNBC reports that harsh winter weather sharply cooled mortgage activity, with total application volume falling 8.9% week over week, according to the Mortgage Bankers Association (MBA), even as rates edged slightly lower. The average contract rate for a 30-year fixed conforming mortgage (≤$832,750) dipped to 6.21% from 6.24%, but that modest move failed to spur demand: refinance applications fell 5% on the week (though still 117% higher year over year when rates topped 7%), while purchase applications dropped a steep 14% and were only 4% higher than a year ago.

Joel Kan, MBA’s Vice President and Deputy Chief Economist, comments:

“Application volume was down last week, led by a 14 percent drop in purchase applications. Winter Storm Fern likely had an impact as much of the country was snowed in, hampering homebuying activity…The annual increase in purchase applications was the weakest since April 2025. Refinance activity also decreased over the week, despite mortgage rates moving lower. The 30-year fixed rate averaged 6.21 percent last week, a slight decline, but not significant enough to incentivize more borrowers to refinance. Additionally, this week’s results are being compared to the week that included the MLK Jr. holiday.”

Megan Hunt of ATTOM reports that the share of seriously underwater mortgages (defined as homes where combined loan balances exceed market value by at least 25%) inched higher in Q4 2025, signaling a modest softening after years of improvement. Nationwide, 3.0% of mortgaged homes were seriously underwater, up from 2.8% in Q3 2025 and 2.5% a year earlier, though levels remain historically low thanks to earlier price gains and conservative lending. According to ATTOM, the highest state-level concentrations were in Louisiana (10.7%, down from 11.2% QoQ but up from 9.5% YoY), Mississippi (8.3%, up from 6.6% QoQ and 6.4% YoY), and Kentucky (7.9%, up from 6.0% QoQ and 6.1% YoY).

Policy updates

Spencer Lee of NMN reports that as the U.S. House prepares to vote this week on the Housing for the 21st Century Act, the mortgage industry is coalescing behind the sweeping legislation, with the MBA and major lenders backing the bill. The proposal bundles a broad set of reforms spanning housing finance, federal oversight, and development policy, signaling rare alignment across industry stakeholders who view the package as a comprehensive update to the housing system rather than a narrow regulatory tweak, and positioning it as a consequential vote for the sector in early 2026.

Brad Finkelstein, also of NMN, reports that the Federal Housing Finance Agency is moving forward with its repeal of the Biden administration’s Fair Lending, Fair Housing, and Equitable Housing Finance Plans rule without modification, despite public comments received after the proposal was first issued in July. The decision finalizes the agency’s rollback of a regulation introduced under the Biden administration, signaling a clear policy shift in federal housing oversight and fair-lending compliance expectations for government-sponsored enterprises and the broader mortgage market.

Matthew Goldstein of The New York Times reports that plans to take Fannie Mae and Freddie Mac public remain unsettled six months after Donald Trump urged Wall Street banks to prepare for a rapid I.P.O., underscoring the tension between market ambitions and housing affordability goals. Despite early signals of momentum, there is still no concrete timeline or structure for privatizing the mortgage giants, reflecting unresolved questions about valuation, regulatory oversight, and how an offering would square with the administration’s push to keep mortgage costs low for homebuyers.

Sarah Wolak of HousingWire reports that reverse mortgage borrowers harmed by illegal servicing practices may receive restitution checks following a Consumer Financial Protection Bureau enforcement action that ordered $11.5 million in total compensation tied to widespread failures affecting up to 150,000 accounts. The action targets loans previously serviced by NOVAD Management Consulting, a subcontractor to the U.S. Department of Housing and Urban Development, and Sutherland. The National Reverse Mortgage Lenders Association alerted members that refunds are underway, and the CFPB confirmed that victim compensation has been ongoing since Jan. 30.

Finally, in a separate HousingWire article, Wolak reports that House Republicans scaled back a proposed increase to VA mortgage fees, amending H.R. 6047 (the Sharri Briley and Eric Edmundson Veterans Benefits Expansion Act of 2025) to avoid raising costs on VA home purchase loans while funding expanded veterans benefits through higher fees on refinances and loan assumptions instead. Under the revision, purchase-loan fees through the U.S. Department of Veterans Affairs would remain unchanged, IRRRL refinance fees and assumption fees would rise (details pending), and disabled veterans would remain exempt.