Logan Mohtashami of HousingWire reports that mortgage rates fell to a year-to-date low of 6.50%, despite political turbulence, including President Trump’s attempt to fire Fed Governor Lisa Cook. The decline reflects improving mortgage spreads, which have narrowed compared to the peak of 2023 when rates would have been 0.84% higher under those conditions. With the 10-year Treasury yield at 4.28%, spreads remain the key driver. If they normalized, today’s rates could be as low as 5.86%–6.06%.

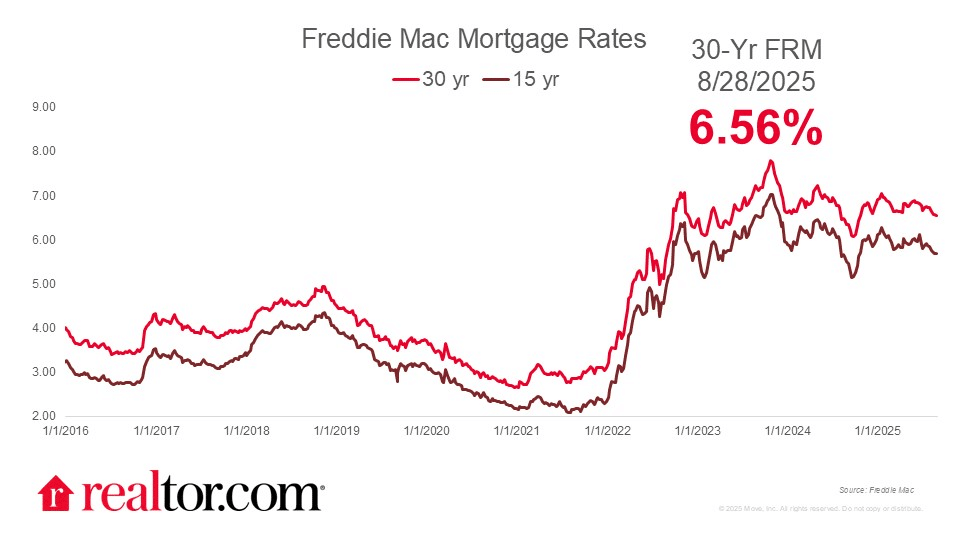

Danielle Hale of Realtor.com reports that the Freddie Mac 30-year fixed mortgage rate dipped to 6.56% on August 28, 2025, marking a 10-month low after peaking in May. While lower rates have modestly boosted existing-home sales in July, new-home and pending sales remain weak. Compared with 2019, the typical U.S. family has lost nearly $30,000 in homebuying power due to higher rates, making this a “cruel summer” for many buyers. Looking ahead, Fed Chair Jerome Powell has signaled a likely September rate cut, which could push mortgage rates lower through mid-September.

Source: Realtor.com (September 2025)

Catherine Koh of the National Association of Home Builders (NAHB) comments on the ongoing drama between the Fed and the Trump administration:

“Recently, President Trump sought to fire Federal Reserve Governor Lisa Cook, alleging she submitted fraudulent information on mortgage applications. Cook has since filed a lawsuit to block her dismissal, arguing that the president lacks authority to remove a Fed governor without cause. The case underscores ongoing concerns about the central bank’s independence from political influence. Separately, former Federal Reserve Governor Adriana Kugler resigned earlier this month to return to academia, creating a vacancy on the Board of Governors for the President to fill. Both Cook and Kugler were nominated by President Joe Biden.”

Indeed, Stuart Lau and Peter Hoskins of the BBC reported that Cook would sue President Trump for the attempt to fire her, arguing that there is no legal authority under the Federal Reserve Act. Trump claims Cook made false mortgage statements and cites constitutional powers for her removal, but the Fed emphasized that governors can only be dismissed “for cause” to protect their independence. Cook, the first Black woman on the Fed board, plays a key role in setting U.S. interest rates, and her ouster attempt has already rattled bond markets, raising concerns over the Fed’s credibility and potential global impacts on borrowing costs.

Jasper Goodman and Jordain Carney of Politico report that President Trump’s escalating battle with the Fed is about to hit Capitol Hill, as the Senate Banking Committee prepares to hold a hearing on Stephen Miran’s nomination to a Fed board seat next week. The clash follows Trump’s controversial attempt to fire Fed Governor Lisa Cook, a move widely expected to spark a landmark legal fight and intensify partisan divisions over the Fed’s independence. Republicans face pressure to either back Trump’s push or defend the Fed’s autonomy, while Democrats plan to make central bank independence the centerpiece of their opposition.

Rent data

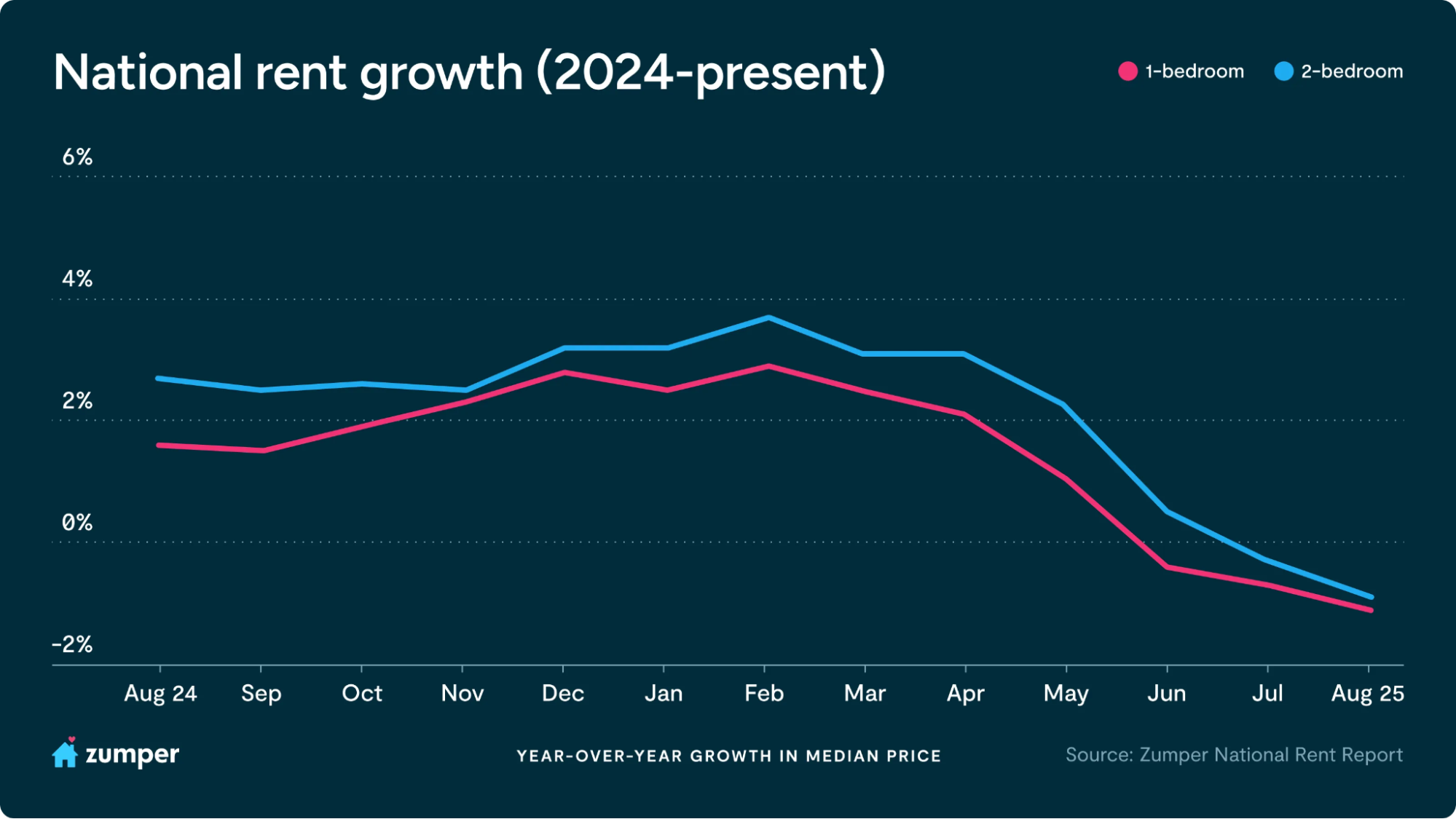

Crystal Chen reports on Zumper’s National Rent Index, which turned negative for the first time, with median one-bedroom rents down 0.2% to $1,517 and two-bedrooms down 0.4% to $1,897 in August, both off about 1% annually. It marks the fourth month of slowing growth as new supply and migration trends pressure landlords to cut prices. Regionally, San Francisco leads rent growth with two-bedrooms up 16.4% year-over-year, while Jersey City saw the steepest declines, over 20%. New York City remains the priciest market, nearly $1,000 above San Francisco for a one-bedroom.

Source: Zumper (September 2025)

Anthemos Georgiades, CEO of Zumper, comments:

“This month’s report marks a key turning point. For the first time, our National Rent Index has dipped into negative territory across the board, both monthly and annually, with one and two-bedroom rents now firmly on the decline…Renters today have more choices than they’ve seen in years, which applies downward pressure on pricing. Compounding the slowdown is weaker consumer confidence, which affects both sides of the market: renters hesitant to commit in an uncertain economy, and property owners strategically prioritizing occupancy and cash flow over rent growth.”

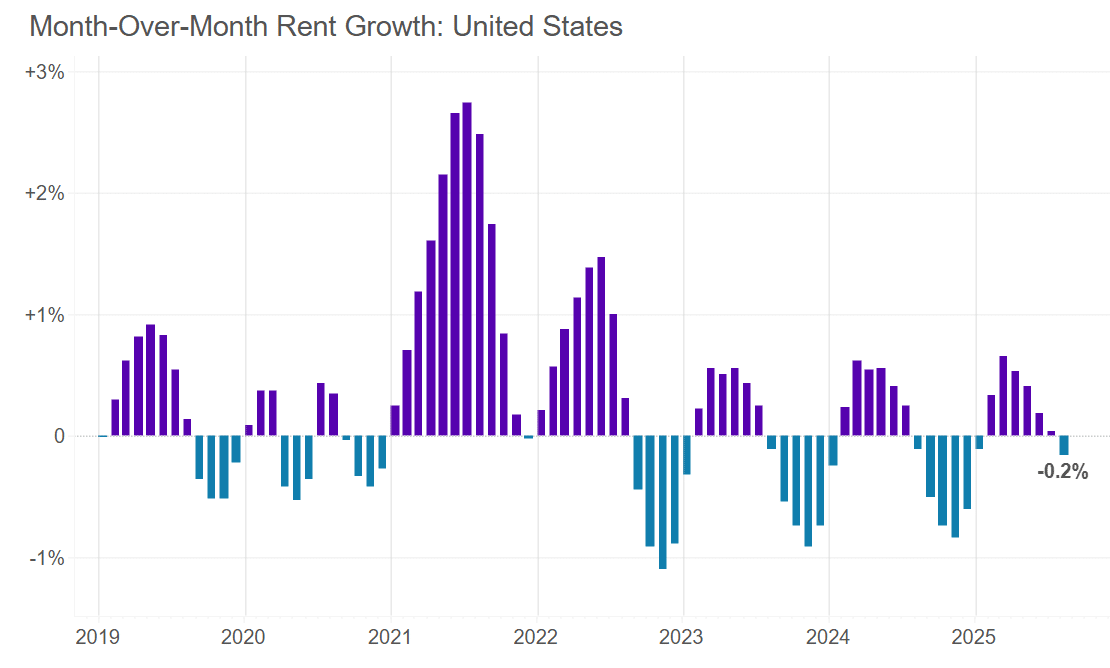

The Apartment List Research Team reports that the national median rent fell 0.2% in August to $1,400, the first monthly decline since January and a signal that the market is entering its off-season. Rents are now 0.9% lower than a year ago, with year-over-year growth negative for four months and at its weakest since late 2023. The multifamily vacancy rate hit a record 7.1%, as new supply continues to enter the market, pushing listings to take an average of 29 days to lease. Regionally, Austin leads declines with rents down 6.6% year-over-year, while San Francisco tops growth with a 4.7% increase.

Source: Apartment List (September 2025)

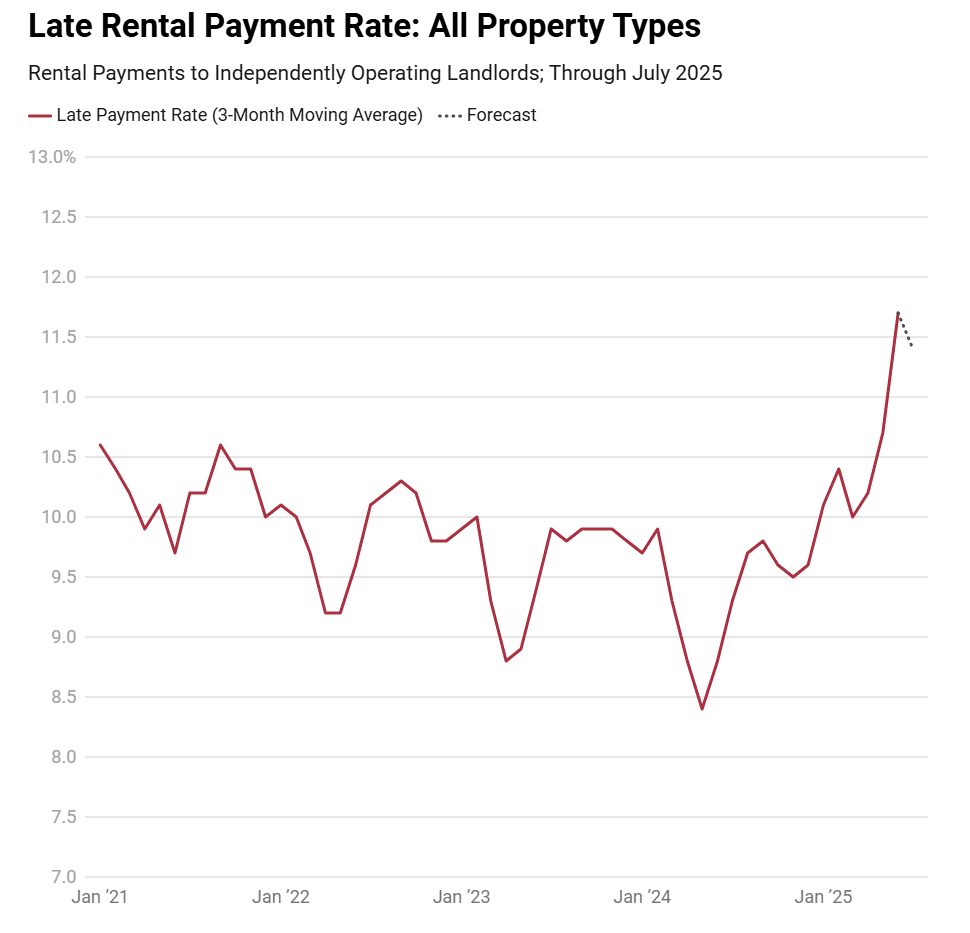

Finally, Jason M. Davis of Chandan reports that on-time rent payments have steadily declined since April 2023, highlighting renter financial stress as expenses outpace income growth. By June 2025, the three-month average of late payments rose to 11.7%, up from 8.8% in mid-2024, even as most renters eventually pay in full. The gap between on-time (-502 bps) and total rent collections (-428 bps) underscores rising delays, linked to household debt climbing $40 billion in Q2 and higher delinquency rates.

Source: Chandan (September 2025)

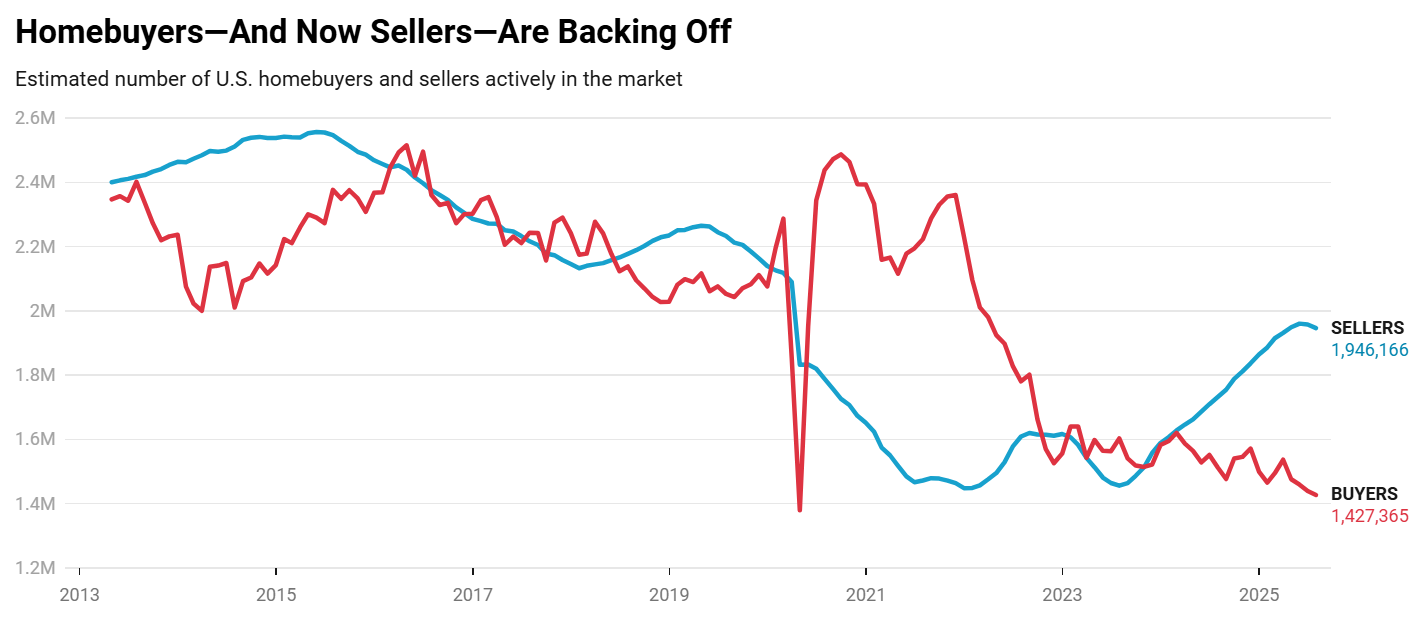

Buyers and sellers

Anushna Prakash of Zillow reports that buyers are finally seeing more options, with 439,000 homes affordable to a median-income household in July 2025—the highest level since August 2022 and up 20% year-over-year thanks to an 18% inventory surge. This means more leverage and choices for first-time buyers, especially in markets like Buffalo, St. Louis, and Pittsburgh, where over half of listings are affordable. However, steep affordability hurdles remain: the typical mortgage payment has doubled in five years, keeping many renters sidelined. For sellers, the shift is clear: Homes are sitting longer, and a record 27.4% of listings had price cuts in July.

Lily Katz and Asad Khan of Redfin report that the housing market is cooling on both sides, with the number of homebuyers dropping to just 1.43 million in July, the lowest since 2013 outside of the pandemic, and sellers retreating as well, down about 14,000 since May. Even with that dip, there are still 36 percent more sellers than buyers, the widest gap on record, leaving buyers firmly in control in most markets, particularly in Texas and Florida. Homes are lingering on the market longer, stale listings are piling up, and only five seller’s markets remain. Falling mortgage rates could entice both buyers and sellers back, but for now, leverage rests with buyers.

Source: Redfin (September)

“Homebuyers are spooked by high home prices, high mortgage rates and economic uncertainty, and now sellers are spooked because buyers are spooked…Some sellers are delisting their homes or choosing not to list at all after seeing other houses sit on the market for weeks or months, only to fetch less than the asking price.”

Dana Anderson, also of Redfin, reports that falling mortgage rates, now averaging 6.58%—a 10-month low—have nudged demand higher, with pending home sales up 2% in late August and Redfin’s Homebuyer Demand Index up 3% from a month earlier. For buyers, lower monthly payments of $2,616 are luring some back into the market, though many are still waiting for further rate cuts. Sellers, meanwhile, face more pressure to negotiate as agents note that it remains a buyer’s market. If rates drop further, competition could heat up quickly, but buyers hold most of the leverage for now.

Diana Olick of CNBC reports that pending home sales slipped 0.4% in July as buyers increasingly backed out of deals, with 15% of contracts canceled; the highest rate since at least 2017. For buyers, rising July mortgage rates and broader economic uncertainty fueled hesitation and “cold feet,” particularly in markets like San Antonio, Fort Lauderdale, and Tampa. Sellers, meanwhile, are facing stalled traffic and more arduous negotiations, with just 16% of Realtors expecting buyer activity to improve over the next three months.