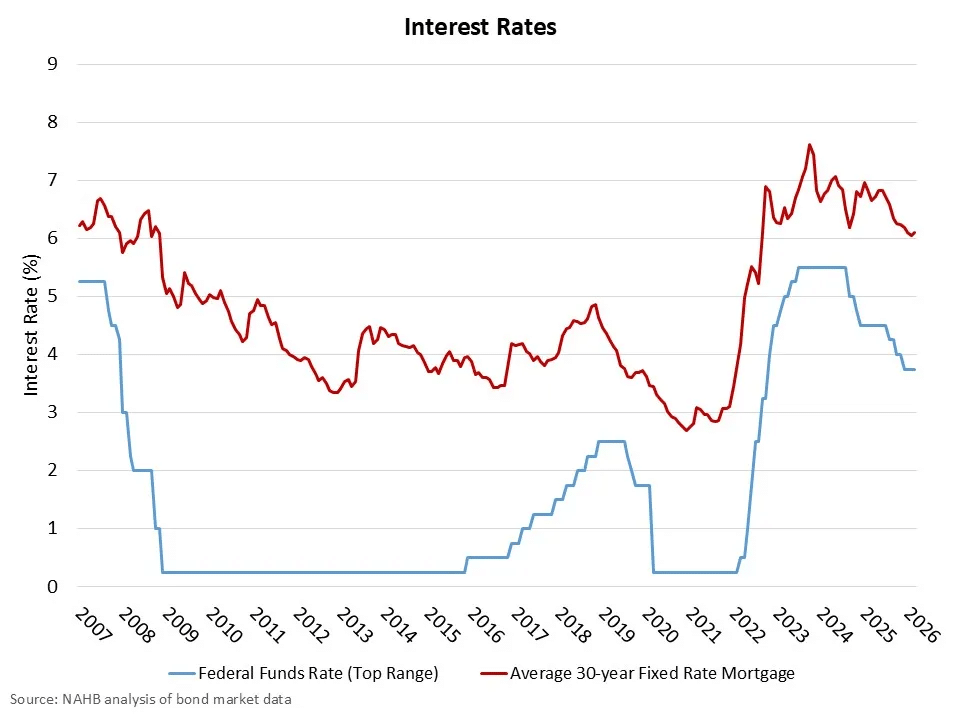

Jessica Dickler of CNBC reported that the Federal Reserve held interest rates steady at 3.50–3.75% at its March meeting, marking its second consecutive pause. The 30-year fixed mortgage rate has climbed to 6.29%, up from 5.99% at the end of February, while the 10-year Treasury yield rose to 4.208%. Rising gas prices and inflation above the Fed’s 2% target continue to weigh on any prospect of near-term cuts.

Robert Dietz of the National Association of Home Builders (NAHB) noted that the Fed’s updated Summary of Economic Projections revised core PCE inflation upward to 2.7% from 2.4% in December, with the dot plot signaling just one rate cut in 2026 and one in 2027. Chair Powell described the housing sector as “weak,” and NAHB has revised its own forecast to just one cut this year due to oil-driven inflation from the Iran conflict. Governor Miran was the lone dissenter, voting for a quarter-point cut.

Source: NAHB (March 2026)

“NAHB had forecasted two additional rate cuts for 2026, based on the expectation of modest easing of inflation and a cool labor market. However, consistent with market expectations, our forecast will reduce this to just one rate cut for 2026 due to higher inflation pressure related to headline issues, including increased oil prices due to the Iran war. A longer conflict will have a relatively greater impact on the delay for future Fed rate cuts.”

Jake Angelo of Fortune reports that the conflict in Iran has fundamentally shifted the Fed’s trajectory, with the Market Probability Tracker showing rate cut odds plunging from 60% in February to just 16% as of Tuesday. This energy crisis has pushed oil prices beyond $100 a barrel, fueling fears of 1970s-style stagflation and prompting Yardeni Research to raise the probability of a market meltdown to 35%. While February consumer prices sat at 2.4% before the latest military strikes, the sudden spike in commodity costs has forced the market to price in a 15% chance of a rate hike, a scenario previously dismissed by most experts.

Matthew Kazin and Eric Revell of Fox Business reported that Fed Vice Chair Bowman has penciled in three rate cuts before year-end, citing labor-market concerns—a notably dovish stance from a typically hawkish member. “I’m still concerned about the job market,” Bowman said, “I want to see a little bit of recovery there. But, of course, I’ve written three cuts in for before the end of 2026 to hopefully support the labor market.” The FOMC voted 11-1 to hold, with the SEP median projecting just one 25-basis-point cut. Meanwhile, Powell said he will remain at the Fed until the DOJ’s investigation into the Fed headquarters renovation is “well and truly over.”

FinCen

Luc Cohen of Reuters reported that U.S. District Judge Jeremy Kernodle in Tyler, Texas, struck down FinCEN’s nationwide anti-money laundering rule for real estate on March 20. The 2024 regulation had required disclosure of the beneficial owners of companies making all-cash property purchases, expanding geographic targeting orders previously limited to cities like New York and Miami. Former Treasury Secretary Janet Yellen had estimated roughly $2 billion was laundered through U.S. real estate from 2015 to 2020.

Jonathan Delozier of HousingWire noted that Judge Kernodle ruled FinCEN exceeded its statutory authority under the Administrative Procedure Act, finding that non-financed real estate transfers to entities or trusts are not “categorically suspicious.” The plaintiff, Flowers Title Companies, was represented by the Pacific Legal Foundation. By FinCEN’s own estimates, the rule would have covered 800,000 to 850,000 transfers annually at a compliance cost of up to $690 million.

Delozier also highlighted that the judge vacated the rule entirely, restoring the status quo before its March 1 effective date. However, a separate challenge in a Florida federal court previously upheld the rule, and the FACT Coalition noted that two other federal courts have also found it lawful and constitutional. The government is widely expected to appeal.

Emily Stabile of the American Banker highlights a critical bottleneck at FinCEN, noting that while the agency serves as a primary defender against global terror and drug financing, its failure to finalize whistleblower rules authorized in 2022 is stalling vital intelligence. Despite its small size of only a few hundred full-time employees, the bureau has successfully levied billions in civil penalties for Bank Secrecy Act violations; however, the lack of a formal program undermines the confidence of potential informants. Stabile argues that for FinCEN to maintain its heavy-hitting enforcement streak, the Treasury Department must urgently prioritize staffing and clear regulatory frameworks to transform the program from a theoretical tool into an active shield for the U.S. financial system.

According to legal experts: “Effective immediately, the Rule is vacated and no longer in effect. Reporting persons, including title companies, settlement agents, and closing attorneys, are therefore not currently required to file Real Estate Reports under 31 C.F.R. § 1031.320. The practical effect is a return to the pre-December 2025 operating environment, in which FinCEN’s GTO program, with its geographic limitations and price thresholds, remains the primary governance tool for non-financed real estate transaction reporting. Title insurance underwriters and other related companies operating in major U.S. metropolitan markets can expect FinCEN to resume issuing GTOs to close the anticipated AML reporting gaps.”

Rentals

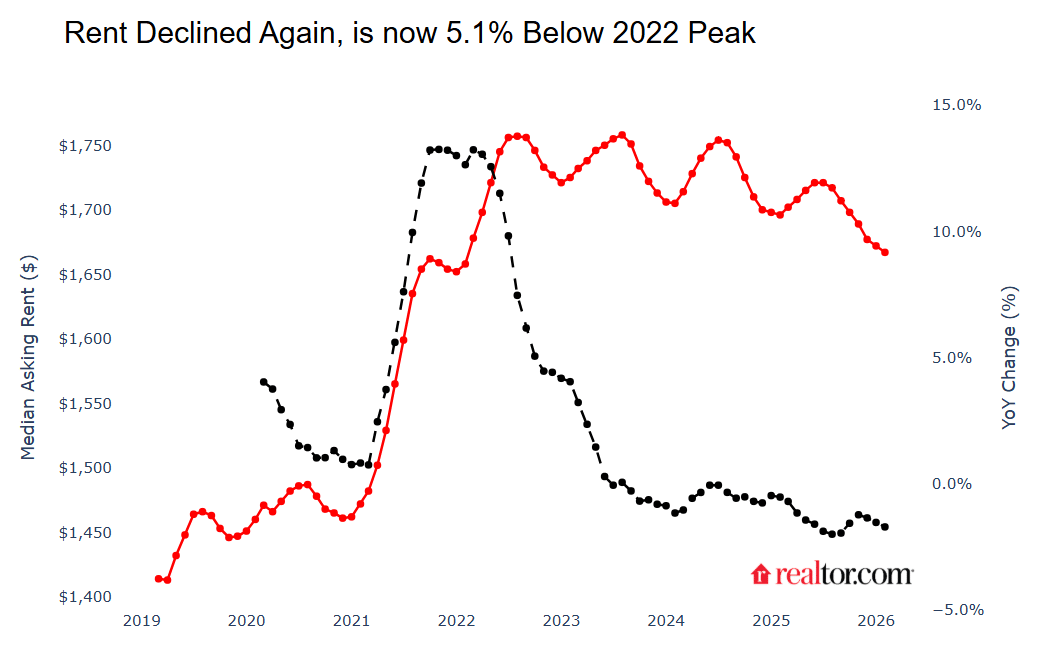

Jiayi Xu and Danielle Hale of Realtor.com report that February 2026 marked a significant milestone for the housing market as national median asking rents hit a four-year low of $1,667, marking the 30th consecutive month of year-over-year declines. This downward trend has been most pronounced in two-bedroom units, which saw the sharpest drop at 1.9%, while overall rents have now receded 5.1% from their 2022 peak.

Source: Realtor.com (March 2026)

While the rental landscape is currently the most budget-friendly it has been since March 2022, the authors note a stark geographic divide: cities like Austin have seen massive cumulative relief of 18.2%, yet markets like Virginia Beach and Kansas City remain within 3% of their all-time highs. This suggests that while national averages are cooling, a potential spring rebound could soon end the streak of monthly price drops.

Eric Revell of Fox Business reports that American renters finally found some breathing room in February as the national median asking rent hit a four-year low of $1,667. While this figure remains 14.2% above pre-pandemic levels, it marks a significant 5.1% drop from the 2022 peak, with 15 major metro areas recording double-digit percentage declines. Austin leads the downward trend with a staggering 18.2% drop from its record high, followed closely by Birmingham at 17.1% and Memphis at 16.1%. These shifts suggest a cooling trend in markets that had been overheated, offering a reprieve to tenants even as overall housing costs remain elevated relative to historical norms.

Marcus Lu of the Visual Capitalist breaks down the long-term impact of the pandemic migration wave, revealing that average rents across major U.S. cities have surged 36% since 2020. Leading the pack is Miami, where prices skyrocketed 53% to a monthly average of $2,645, a figure that now eclipses those of traditionally expensive hubs like Seattle. The data underscores a massive shift toward the Sun Belt, with Tampa following closely at 50% growth and Riverside at 48%, driven by an influx of nearly half a million new residents in some regions. Interestingly, while the national trend shows heavy inflation, formerly booming markets like San Francisco and Austin have seen much more subdued growth at 13% and 14%, respectively, highlighting a significant rebalancing of where Americans are choosing to call home.

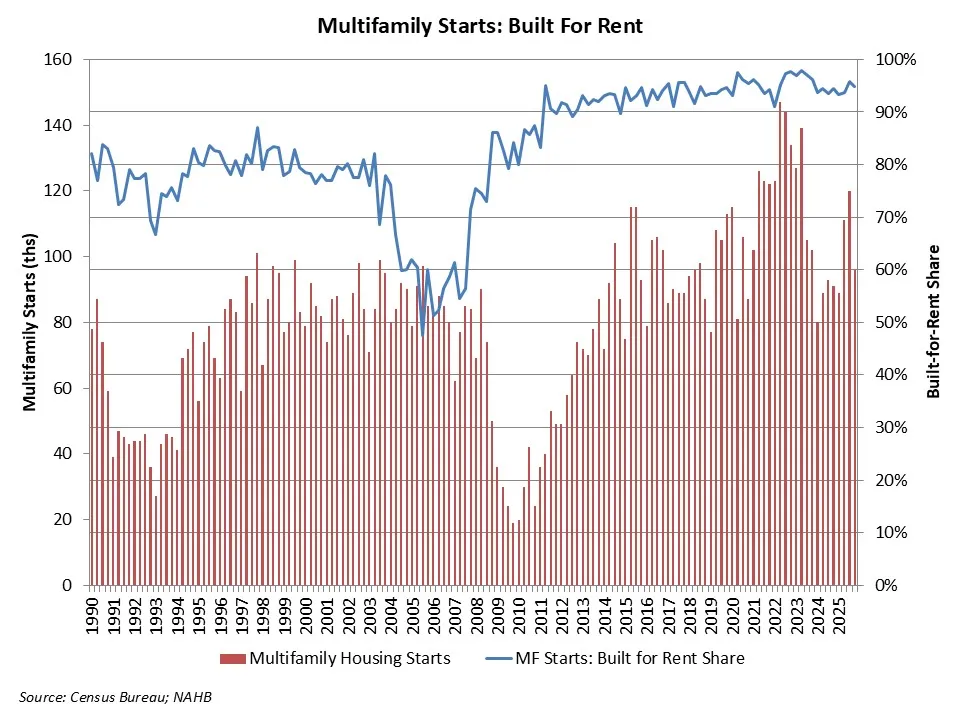

Robert Dietz of NAHB reports a surprising surge in the housing pipeline, noting that 96,000 multifamily residences broke ground in the final quarter of 2025. This activity was almost entirely driven by the rental sector, which accounted for a massive 95% market share, a stark contrast to the 47% low seen during the 2005 condo boom. With 91,000 built-for-rent units entering the mix, construction starts jumped 18% compared to the previous year, though Dietz cautions that these figures may face downward revisions in future Census updates. While the rental market is seeing this aggressive expansion, the condo segment remains stagnant, with only 6,000 starts, signaling that developers are still heavily betting on a “renter nation” rather than traditional homeownership.

Source: NAHB (March 2026)

Finally, Orphe Divounguy of Zillow points out that a persistent supply glut is finally handing the steering wheel back to renters, with national asking rents easing to a 1.9% annual growth rate, the slowest pace seen since 2020. This shift is fueled not just by a boom in apartment construction, but also by “accidental landlords” who, unable to sell in a cooling housing market, have pivoted to renting out their single-family homes. While the typical rent now sits at $1,895, nearly 40% of Zillow listings are sweetening the deal with concessions like free rent to attract tenants. Despite this newfound leverage, the financial bar remains high: a household now needs an annual income of $76,000 to comfortably afford a home, a staggering 35% increase from the pre-pandemic requirement.