Apartment List reports in their May 2025 National Rent Report that the national median rent rose 0.5% month-over-month in April to $1,392, while remaining down 0.3% year-over-year. Vacancy rates hit a record high of 7%, driven by a historic surge in multifamily supply, with over 600,000 new units completed in 2024. Despite the recent cooldown, national rents remain 21% higher than in January 2021, though 3.5% below their August 2022 peak.

Source: Apartment List (April 2025)

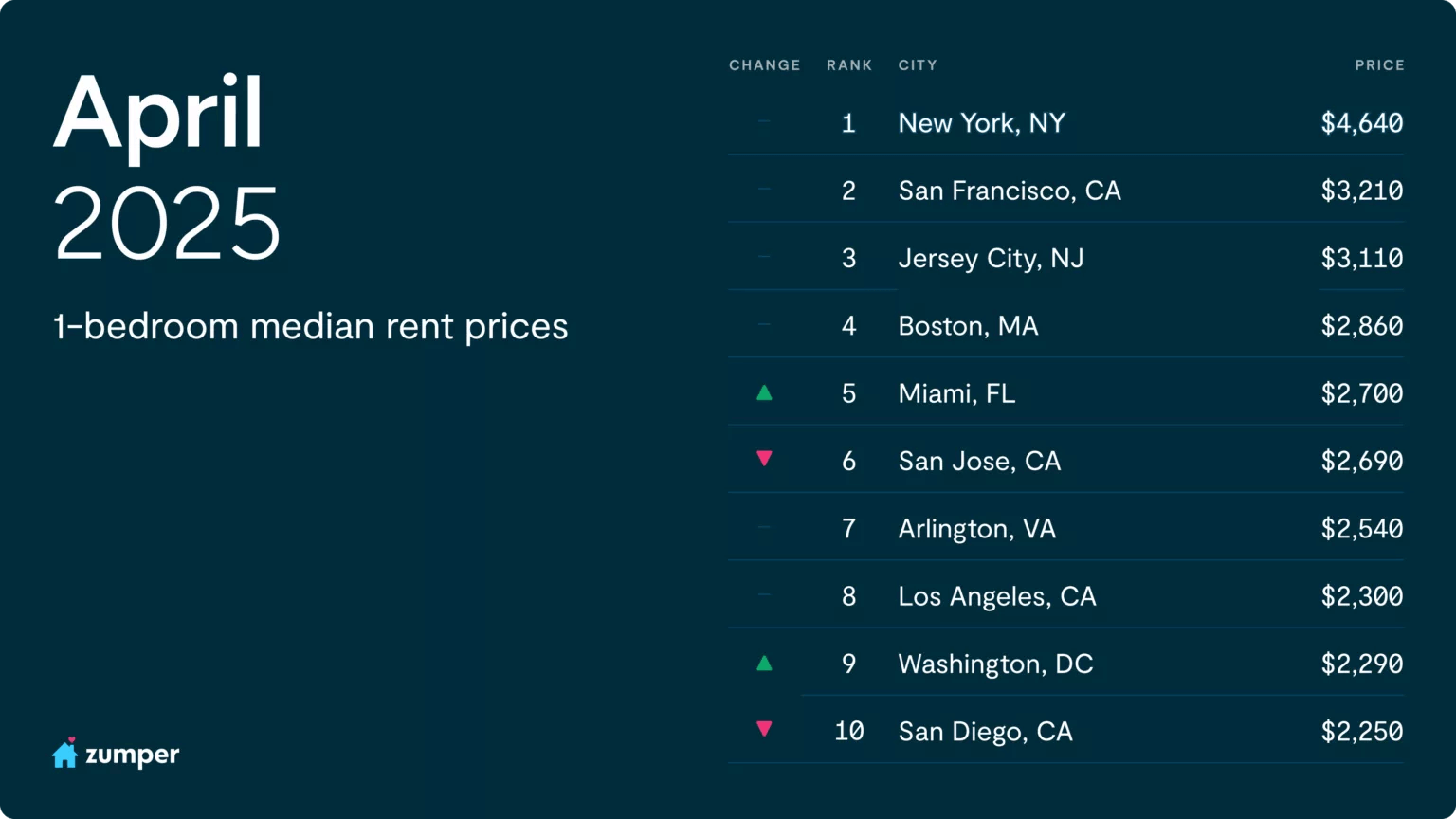

Crystal Chen of Zumper reports that the national median rent fell 0.5% month-over-month in April 2025 to $1,517 for one-bedrooms and 0.2% to $1,901 for two-bedrooms, marking the third straight month of flat or declining prices. Year-over-year, rents are still up 2.1% and 3.1% respectively, but growth is decelerating as a historic wave of new apartment supply softens the market. New York City rents hit record highs, with one-bedrooms at $4,640 (+8.4% YoY) and two-bedrooms at $5,920 (+19.6%).

Source: Zumper (April 2025)

Alecia Pirulis of Apartments.com reports on its data showing that the national average rent in March 2025 was $1,575, up 1.1% year-over-year, with vacancy steady at 8.1%. Omaha stands out with a 3.6% annual rent rise and expected 4.1% growth by year-end, while markets like Austin (-4.5%) and Denver (-3.6%) continue to decline due to oversupply. Shifting job growth toward the Midwest and Northeast is tightening those rental markets, with New York City rents up 0.9% to $3,926 and a low 2.8% vacancy rate.

Skylar Olsen of Zillow reports that U.S. asking rents hit $2,005 in March 2025, up 0.6% month-over-month and 3.5% year-over-year, pushing the median rent burden to 29.4% of household income, just shy of the 30% affordability threshold. Single-family rentals, now averaging $2,223, are becoming less affordable, with households spending 32.6% of their income on them, while multifamily rents, averaging $1,849, remain relatively more accessible at 27.1%. Rent concessions are slipping as competition intensifies, signaling that incentives like free months may soon disappear.

Finally, Jiayi Xu and Danielle Hale of Realtor.com report that March 2025 marked the 20th straight month of year-over-year rent declines, with the median rent for 0–2 bedroom properties down 1.2% to $1,694, still 20.2% higher than pre-pandemic levels. Larger units saw the steepest annual declines, with two-bedroom rents falling 1.4%. However, new 25% tariffs on imported steel and aluminum threaten to slow multifamily construction, particularly in fast-growing markets like Milwaukee and Oklahoma City, potentially pushing rents back up later this year.

Affordability

Anushna Prakash of Zillow reports that housing affordability has worsened, with 233 U.S. cities now seeing typical starter homes priced above $1 million — up from just 85 cities five years ago. Although the national median starter home value remains a more accessible $192,514, pandemic-era price growth has pushed young households into renting longer, raising the median renter age to 42. California leads with 113 cities over the $1 million mark, but half of the states now have at least one city where first-time buyers face a seven-figure hurdle.

Joel Berner of Realtor.com highlights that while affordability remains a major hurdle nationwide, Southern and Midwestern states have stronger affordability scores and more active homebuilding. No state earned an A+ in Realtor.com’s housing report card, and only three states — South Carolina (A), Iowa (A-), and Texas (A-) — stood out by balancing current affordability with future supply growth. Meanwhile, the West and Northeast lag, burdened by stricter regulations and escalating housing costs.

Source: Realtor.com (April 2025)

“There were no A+’s given, which says a lot about how far we still have to go to make homeownership truly attainable. South Carolina scored the highest of any state with an A, primarily due to top-notch homebuilding scores, and despite a middle-of-the-pack affordability score. Iowa and Texas both got A-’s, but in very different ways. Iowa dominated our affordability criteria but had a weaker showing in terms of new construction, while Texas’ strong permit-to-population ratio and Iowa’s new-construction premium helped it to overcome some current affordability issues.”

Falen Taylor of the Mortgage Bankers Association (MBA) reports that homebuyer affordability improved slightly in March 2025, with the national median mortgage payment dropping 1.4% month-over-month to $2,173. Thanks to a 4.8% annual rise in median earnings and easing mortgage rates, the Purchase Applications Payment Index (PAPI) fell 5.8% year-over-year, signaling better affordability. FHA borrowers saw median payments dip to $1,872, while conventional loan applicants averaged $2,200, though concerns remain as market volatility and declining consumer confidence could reverse these gains.

Edward Seiler, MBA’s Associate Vice President, comments:

“Homebuyer affordability conditions improved slightly in March as lower mortgage rates spurred renewed activity in the housing market…Despite improving conditions in March, the outlook in the upcoming months is cloudier. Ongoing affordability concerns, declining consumer confidence, and volatility in the financial markets could all put downward pressure on homebuyer demand.”

Existing home sales

Troy Green of the National Association of Realtors (NAR) reports that existing-home sales fell 5.9% in March 2025 to an annualized rate of 4.02 million, down 2.4% from a year earlier. Despite sluggish sales driven by high mortgage rates, the median home price hit a record $403,700 for March, marking the 21st consecutive month of year-over-year price increases. Meanwhile, housing inventory rose 8.1% month-over-month to 1.33 million units, offering 4.0 months’ supply at the current sales pace.

Nicole Friedman of The Wall Street Journal reports that this was the steepest monthly drop since 2022 as rising economic uncertainty spooked buyers during the critical spring season. Despite inventory climbing nearly 20% year-over-year and mortgage rates easing slightly, many buyers remained sidelined, driving the slowest March sales pace since 2009. Widespread price cuts and growing seller concessions reflect a market where buyers now hold more negotiating power amid affordability pressures and shaken confidence.

Source: WSJ (April 2024)

NAR Chief Economist Lawrence Yun, comments: “In a stark contrast to the stock and bond markets, household wealth in residential real estate continues to reach new heights…With mortgage delinquencies at near-historical lows, the housing market is on solid footing. A small deceleration in home price gains, which was slightly below wage-growth increases in March, would be a welcome improvement for affordability.”

Treh Manhertz of Zillow reports on the same data, highlighting a deepening buyer hesitancy. While inventory jumped 19.8% year-over-year, many buyers are holding out for meaningful price cuts, a shift underscored by new homebuilders slashing prices (median down 7.5% year-over-year). Without greater price flexibility or sharper rate drops, the existing home market will likely remain sluggish and uneven through spring.

Keith Griffith of Realtor.com reports that while U.S. existing-home sales plunged, their survey shows sellers remain highly optimistic. “Despite those challenges, sellers appear to be entering the spring season with supreme confidence. A recent Realtor.com survey found that 81% of potential sellers think they will get their asking price or more this year, and 63% think they won’t have to make significant or unexpected concessions.” This is setting up a tense standoff between confident sellers and cautious buyers.