Jody Godoy of Reuters reports that the Federal Trade Commission (FTC) has accused Zillow of paying Redfin $100 million to exit the online rental listings market for up to nine years, alleging the deal unlawfully reduces competition in an already concentrated sector. According to the FTC’s lawsuit, the agreement will likely raise advertising costs for landlords of buildings with more than 25 units and lessen incentives for the companies to improve their platforms for renters. Zillow defends the partnership as beneficial to both renters and property managers.

Luke Fountain of CNBC reports that according to the FTC complaint, Redfin agreed to terminate contracts with advertisers, exit the rental advertising market for up to nine years, and instead syndicate Zillow’s listings. These moves allegedly resulted in hundreds of Redfin layoffs and subsequent rehires by Zillow. The FTC argues that the arrangement eliminates Redfin as an independent competitor in a concentrated sector vital to renters and property managers. At the same time, both companies defend the deal as pro-consumer and efficiency-driven.

According to reports, the FTC is seeking “structural relief … to cure any anticompetitive harm, prevent any future harm, and undo the continuing effects of past harm, including but not limited to, divestiture of assets, divestiture or reconstruction of businesses, and such other relief sufficient to restore the competition that would exist absent the anticompetitive conduct.”

Ramishah Maruf of CNN highlights that the FTC’s lawsuit zeroes in on Zillow’s February 2025 deal with Redfin, which allegedly turned Redfin into an “exclusive syndicator” of Zillow’s listings while forcing it to exit the multifamily advertising market for up to nine years. The agency argues this effectively insulated Zillow from head-to-head competition, driving up costs and worsening terms for property managers and renters alike. Beyond this case, Zillow faces broader scrutiny, including a June 2025 lawsuit from Compass accusing it of anticompetitive practices in digital home listings. All these actions underscore the mounting regulatory and industry challenges for the real estate giant.

Mortgage rates

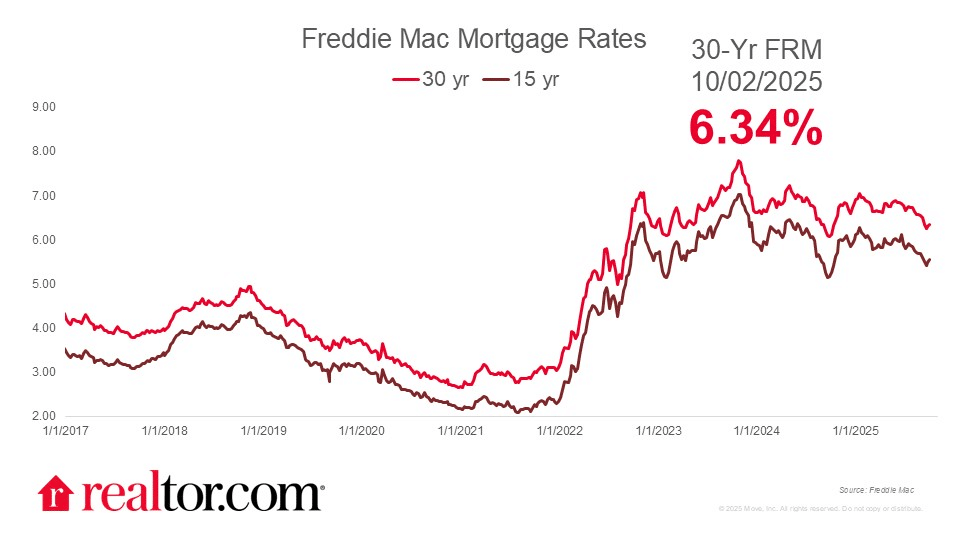

Jiayi Xu of Realtor.com reports that the Freddie Mac 30-year mortgage rate ticked up 4 basis points to 6.34% this week as markets reacted to the federal government shutdown. The timing is significant, coming right after the Fed’s first rate cut in nine months, with key economic data releases (jobs and inflation) now likely to be delayed. While the Fed’s independence means its meetings won’t be postponed, prolonged disruption could sway policy decisions and market sentiment.

Source: Realtor.com (October 2025)

Claire Boston of Yahoo! Finance reports that mortgage rates increased for the second consecutive week, with the 30-year fixed averaging 6.34% and the 15-year at 5.55%. Despite still being near their lowest levels of 2025, the uptick has effectively stalled a short-lived refinancing boom, which saw applications plunge 21% last week, while purchase applications dipped just 1%. Rates have tracked choppy moves in the 10-year Treasury yield, now around 4.1%, as investors weigh the impact of the government shutdown and delayed economic data, including Friday’s postponed jobs report.

Mortgage Bankers Association (MBA) president and CEO Bob Broeksmit comments:

“An increase in mortgage rates cooled borrower demand during the last full week of September…Although purchase applications continue to track above year-ago levels because of lower rates, economic uncertainty and affordability challenges continue to hold back home sales.”

Kara Ng of Zillow reports that mortgage rates have held steady near the mid-6% range after the Fed’s September rate cut, with markets still digesting slower-than-expected easing signals. Despite a report showing a surprise 32,000 private-sector job loss in September (and potential delays to official BLS data due to the government shutdown) rates have barely moved, underscoring investor caution. For housing, this stability creates a window of opportunity for qualified buyers: while affordability challenges persist, homes are sitting longer on the market, giving buyers more leverage.

Home sales and price cuts

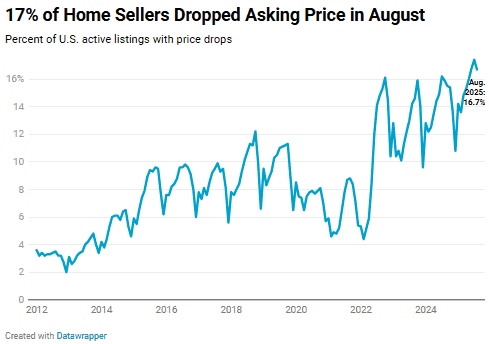

Dana Anderson of Redfin reports that home sellers are slashing prices at record rates. In August, 16.7% of listings posted price cuts, the highest share for that month since 2012. Further, the typical home is now selling for 3.8% below asking, the steepest August discount since 2019. Sellers outnumbered buyers by over 500,000, the second-largest gap on record, giving buyers leverage in a cooling market shaped by high housing costs, economic uncertainty, and rising inventory.

Source: Redfin (October 2025)

Redfin Senior Economist Asad Khan comments:

“While some home sellers have come to terms with the realities of today’s housing market, many are still hoping to cash in on the pandemic-era housing market, when high demand was pushing many sale prices way over asking…Price drops can signal weakness to buyers and lead to further cuts, so home sellers should consult a local agent to set a realistic price from the beginning. It’s also wise for sellers to be patient, understand that it may take a few weeks or even a few months to offload their home in today’s slower-than-usual market, and be open to making concessions.”

In a second report, Dana Anderson of Redfin also writes that pending home sales slipped 1% year over year in late September, the sharpest drop in nearly five months as rising mortgage rates, higher prices, and economic uncertainty sidelined buyers. Rates ticked back up to 6.3% after nine straight weeks of declines, pushing the typical monthly housing payment to $2,590, while pending sales fell hardest in metros like Houston (-15.4%), Denver (-12.3%), and Las Vegas (-11.2%).

That said, Anderson reports that the market has bright spots: starter-home sales rose 4% in August, buyers enjoy leverage with about half a million more sellers than buyers, and soft labor market signals could ease rate pressure ahead—offering some relief for those still in the market.

The Fannie Mae Home Price Expectations Survey, conducted with over 100 housing experts, projects home price growth will cool from 5.3% in 2024 to 2.4% in 2025 and 2.1% in 2026, down from prior forecasts of 2.9% and 2.8%. The survey attributes this moderation to affordability challenges, slowing demand, and broader economic uncertainty. Panelists also weighed in on generational housing trends, noting shifting age dynamics among first-time buyers, the mortgage rate thresholds likely to spark more vigorous sales activity, and the enduring importance of homeownership for younger households despite affordability headwinds.

Jake Krimmel of Realtor.com reports that September’s housing data shows a market cooling unevenly across the country: active listings rose 17% yearly, marking 23 straight months of gains. However, inventory remains 13.9% below pre-pandemic levels, and growth is slowing. The regional split is widening, with the South and West now above pre-2020 inventory while the Northeast and Midwest stay undersupplied. Homes are taking longer to sell, averaging 62 days on market, up a week from last year, with the slowest sales in Florida and Las Vegas. Prices flattened nationally at $425,000, but fell 3.6% in the West. In comparison, nearly 20% of listings cut prices, especially in the $350K–$500K range, highlighting how leverage is shifting to buyers at the lower end even as luxury sellers hold firmer.