Giulia Carbonaro of Newsweek reports that President Donald Trump’s newly passed One Big Beautiful Bill Act promises benefits for high-income homeowners and real estate investors. The bill quadruples the SALT deduction cap to $40,000, where homeowners could see up to $10,500 in annual tax savings. The legislation also reinstates 100% bonus depreciation. It makes the qualified business income deduction permanent, moves hailed by the real estate industry as a significant win, but seen by others as deepening inequality in a fragile housing market.

The Mortgage Bankers Association (MBA) commented on the bill following its passage:

“MBA is pleased that the final tax package preserves or strengthens – and makes permanent – numerous pro-housing and pro-economic growth tax provisions that were identified by our Board-level Tax Task Force, led by 2025 Chair-Elect Christine Chandler and Vice Chair Owen Lee. We believe these provisions will benefit homeowners and renters, increase housing production, and improve the financial outcomes of our single-family and commercial/multifamily members’ businesses.”

The National Mortgage Professional released a report on the bill, commenting on several aspects of the implications on real estate and housing, including:

- PMI Deduction Made Permanent: Borrowers can now permanently deduct mortgage insurance premiums (PMI, FHA MIP, VA funding fees), reducing the cost of low-down-payment loans and offering a new long-term savings tool for buyers.

- Boost to Affordable Housing via LIHTC: The bill expands the Low-Income Housing Tax Credit by 12.5% and reduces bond financing requirements, which could accelerate the supply of affordable rental housing and ease entry-level homebuyer competition.

- SALT Deduction Temporarily Quadrupled: The SALT cap increases from $10,000 to $40,000 (2025–2029), benefiting upper-middle-income homeowners in high-tax states, such as New York, California, and New Jersey, with larger deductions and potentially stronger housing demand.

- Investor Wins on QBI & 1031: Real estate investors retain key advantages, including the permanent 20% qualified business income (QBI) deduction, preserved 1031 exchanges, and maintained interest deductibility, all of which support tax-efficient portfolio growth.

- No New Help for First-Time Buyers: The bill includes no federal down-payment assistance or buyer tax credits and even rescinds some HUD programs, leaving state and local resources as the main tools to support first-time and low-income buyers.

Allen Buchanan of the Orange County Register writes that the bill could have far-reaching implications for commercial real estate, especially in high-tax states like California. The return of 100% bonus depreciation stands out, allowing property owners to fully expense upgrades, such as HVAC systems and tenant improvements, in the year they’re made, a significant boost for repositioning aging assets.

Buchanan also reports that the bill enhances the QBI deduction and temporarily lifts the SALT cap for earners with incomes under $500,000, freeing up capital for reinvestment. However, the proposal’s rollback of green energy incentives and the now-scrapped “revenge tax” targeting foreign investors highlight potential headwinds for ESG-focused projects and cross-border capital.

Rents

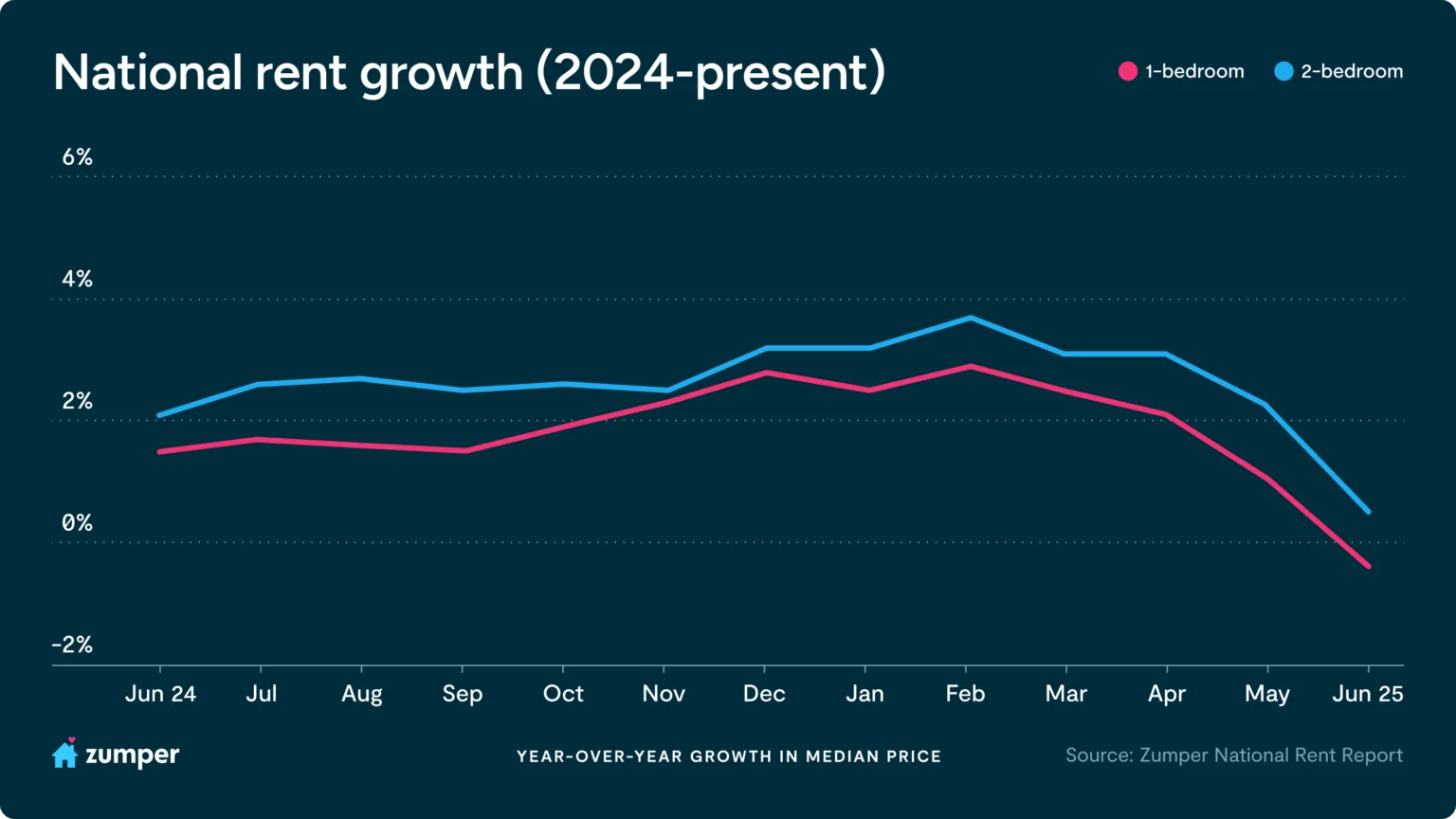

Crystal Chen reports on Zumper’s June 2025 National Rent Index, showing that national rent growth has flattened during what is typically the busiest moving season, with one-bedroom rents holding steady at $1,520 and two-bedrooms nudging up just 0.2% to $1,910. One-bedroom rents declined 0.4% year-over-year, the first annual drop in 14 months, while two-bedroom rents rose a modest 0.5%. San Francisco saw a striking 12.5% yearly rent increase, the second-highest nationally. At the same time, high-supply Sun Belt cities like Austin and Phoenix continued to post negative rent growth, albeit at a slowing rate.

Source: Zumper (July 2025)

Anthemos Georgiades, CEO of Zumper, comments: “The current plateau seen in our national rent prices likely reflects a more deliberate and strategic approach by property owners…This isn’t a sign of weak demand, renters are still out there, but with so much new inventory on the market, landlords are prioritizing occupancy and staying competitive in an increasingly crowded landscape.”

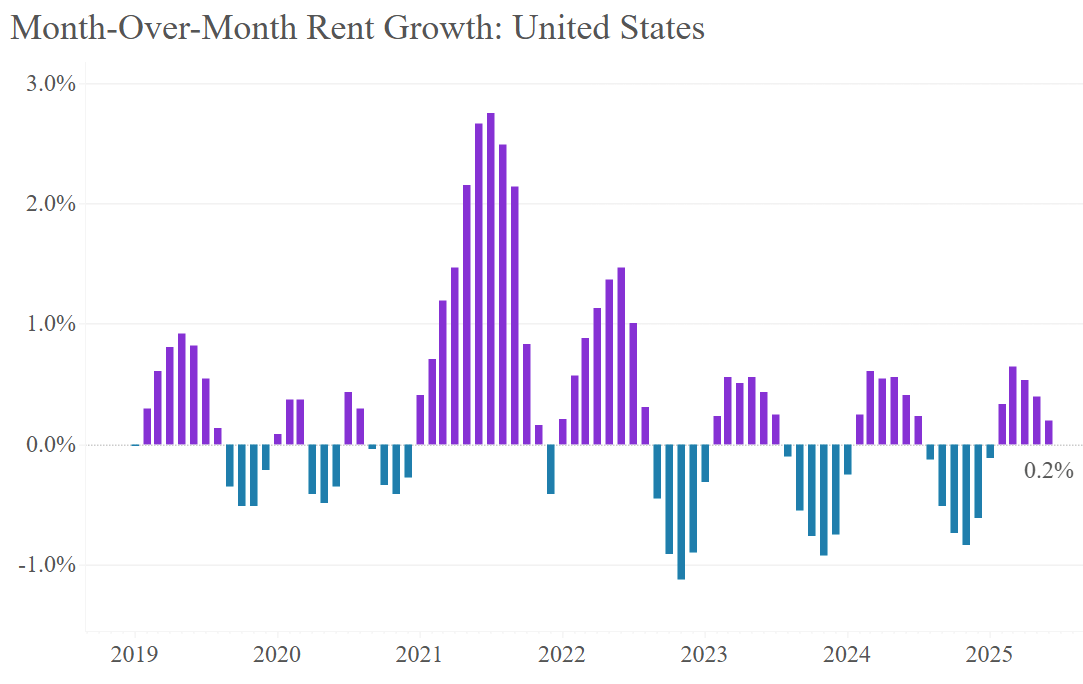

Similarly, The Apartment List released its data showing that the national median rent rose by 0.2% in June to $1,401, marking the fifth straight month of increases. That said, rent growth is slowing at a time when it typically peaks. Year-over-year, rents are down 0.7%, a reversal from the upward trend seen earlier in 2025. The national multifamily vacancy rate has climbed to 7%, the highest on record, as the market continues to absorb a wave of new supply.

Source: Apartment List (July 2025)

On average, Apartment List reports that rental units now take 27 days to lease, improving from 37 days in January. Regionally, Austin leads as the softest rental market with a 6.4% annual decline, while San Francisco posted the strongest growth at 4.9%, highlighting continued geographic divergence amid national market softness.

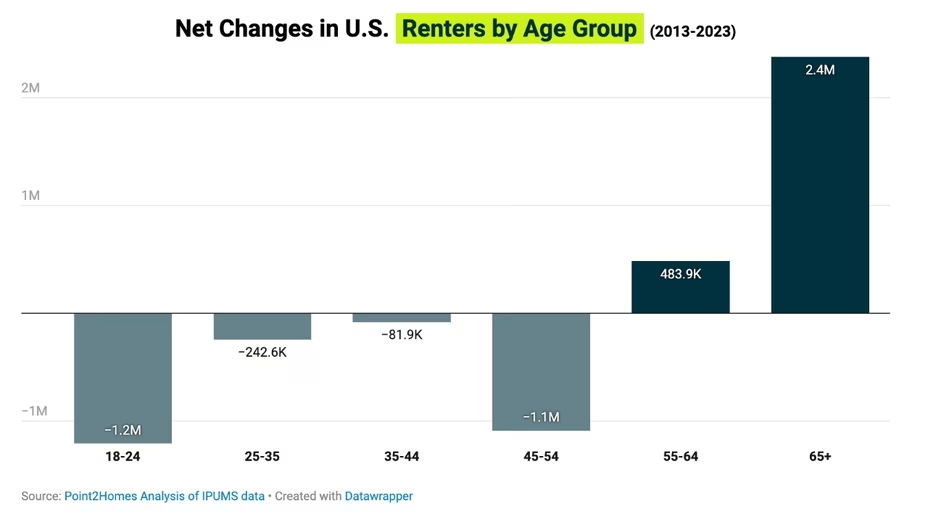

Julie Taylor of Realtor.com reports that from 2013 to 2023, the number of senior renters (age 65+) surged by 2.4 million, a 30% increase, outpacing all other age groups. This shift is driven by fixed incomes, rising homeownership costs, and the growing appeal of senior-friendly rental communities offering low-maintenance living and social amenities. While Florida remains popular, the fastest-growing senior rental markets are Baton Rouge (+80%), Jacksonville, and Austin.

Source: Realtor.com (July 2025)

Lowering rates

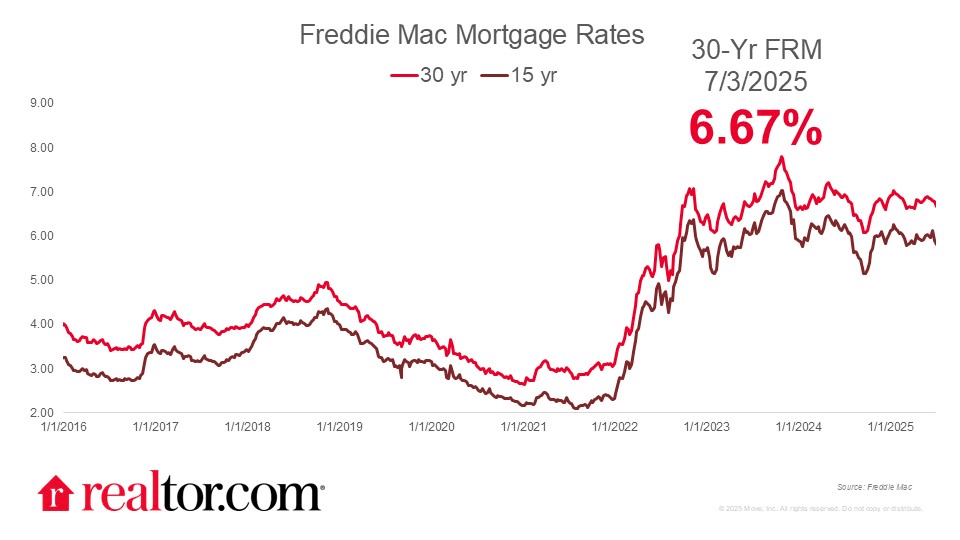

Matt Richardson of CBS News reports that mortgage rates have now declined for five consecutive weeks, with the average 30-year fixed rate dropping to 6.67%, down over 20 basis points since late May. This sustained dip has sparked optimism that rates may fall further, but the Fed isn’t expected to act in July. That said, history shows that even anticipated cuts can prompt lenders to lower rates in advance. For homebuyers, this easing trend could open a window of opportunity before competition intensifies later in the year.

Source: Realtor.com (July 2025)

Kara Ng of Zillow reports that mortgage rates dipped slightly this week, returning to April levels, as softer economic data reinforced signs of a cooling economy. Despite the decline, rates remain stuck in the 6%–7% range, where they’ve hovered for the past year, caught between weakening labor indicators and lingering inflation concerns. With the 90-day tariff pause set to expire on July 9, inflationary pressures could re-emerge, but Zillow still forecasts rates ending the year around the mid-6% range.

Dana Anderson of Redfin reports that lower mortgage rates give buyers on a $3,000 monthly budget an extra $16,000 in purchasing power. That budget now stretches to afford a $455,000 home, compared to just $439,000 five weeks ago. The typical monthly payment on a median-priced $441,000 home has dropped nearly $100 during that time, from $2,795 to $2,705. While rates remain at double pandemic-era lows, the recent decline offers welcome relief for buyers who have long been sidelined by affordability constraints.

Redfin Chief Economist Daryl Fairweather comments:

“Homebuyers have a window of opportunity today–and it could be short…We expect mortgage rates to remain in the high-6% or low-7% range for the rest of the year, as the Fed has made it clear it doesn’t plan to cut interest rates. That makes now a good time for house hunters to lock in mortgage rates, as they’re unlikely to dip much lower in the near term–and they could bounce back up. Economic uncertainty surrounding President Trump’s signature policy bill, which is moving through Congress now, could drive rates up.”