Ana Teresa Solá of CNBC reports that Fed Chair Jerome Powell signaled possible rate cuts during his Jackson Hole speech, a shift that could lower homeowners’ borrowing costs. Mortgage rates, which closely follow 10-year Treasury yields, already sit at 6.58% for a 30-year fixed loan as of Aug. 21. Experts like Jessica Lautz of the National Association of Realtors (NAR) note that a September cut could create strong refinancing opportunities, with savings kicking in once rates fall at least 50 basis points below a homeowner’s current loan.

Logan Mohtashami of HousingWire reports that mortgage rates dipped after Powell, in his Jackson Hole speech, admitted the Fed is now prioritizing labor concerns over inflation amid signs of a weakening job market. The July employment report showed payroll growth slowing to just 35,000 per month over the past three months, down sharply from 168,000 in 2024, with revisions further worsening the trend. Unemployment edged up to 4.2%, labor force growth has slowed due to reduced immigration, and both manufacturing and residential construction jobs are being lost.

Nick Timiraos of the Wall Street Journal reports that Jerome Powell used his Jackson Hole speech to signal that softening labor market conditions and tariff-driven inflation could justify a Fed rate cut as soon as September. While Powell acknowledged rising risks of layoffs and unemployment, he tempered expectations of aggressive cuts, stressing vigilance on inflation, which remains above 2%, and noting the Fed’s benchmark rate sits at 4.3%. Here are a few takeaways from Powell’s speech:

- Labor Concerns: Payroll revisions and slowing worker demand raise fears of rising unemployment.

- Tariff Inflation: Tariffs are visibly pushing consumer prices higher, though Powell expects most effects to be temporary.

- Political Pressure: Trump continues to pressure the Fed with threats, investigations, and floated successors to Powell.

- Policy Balance: Powell emphasized caution, balancing inflation risks against labor market weakness, and reaffirmed the Fed’s independence from politics.

Jake Krimmel of Realtor.com comments on the implications for housing:

“The Fed’s pivot could matter in two ways. In the short run, mortgage rates remaining at 10-month lows are already offering a boost to affordability and, potentially, to buyer sentiment. That relief is welcome after several years of high borrowing costs eroded consumers’ purchasing power, leaving this summer especially frustrating for buyers, sellers, and builders as both existing– and new-home sales stayed sluggish. But there’s also a longer-run shift in play: If Powell’s new framework signals a steadier commitment to balancing inflation and employment risks, it could reduce uncertainty and stabilize rate expectations.”

In more Fed news, Elisabeth Buchwald of CNN reports that former St. Louis Fed president James Bullard, now dean at Purdue’s business school, confirmed he is in talks with Treasury Secretary Scott Bessent about potentially succeeding Jerome Powell as Fed chair when his term ends in May. Bullard said he would accept the role only if the Fed’s independence from political interference is preserved, noting Trump has repeatedly pushed for direct influence over rate decisions. He also argued current rates are “somewhat” too high and suggested cutting them by a full percentage point over the next year could be appropriate.

Housing trends

Fannie Mae’s Economic and Strategic Research Group projects total home sales will hold steady at 4.74 million units in 2025, down slightly from last month’s 4.85 million forecast. Existing home sales are expected to reach 4.09 million, just above 2024’s 4.06 million, while mortgage rates are forecast to end 2025 at 6.5% and 2026 at 6.1%, modestly higher than prior estimates.

Similarly, Zillow published its Home Value and Home Sales Forecast, predicting that home values will end 2025 down 0.9%, with existing home sales at 4.09 million. This is just 0.6% above 2024 but a downgrade from prior estimates as high costs and a weaker labor market weigh on buyers. Inventory is expected to rise as new listings outpace sales, especially in the West and South. At the same time, rent growth slows to multi-year lows, with single-family rents up only 2.5% and multifamily rents just 1%, the weakest gains since 2018 and 2020, respectively.

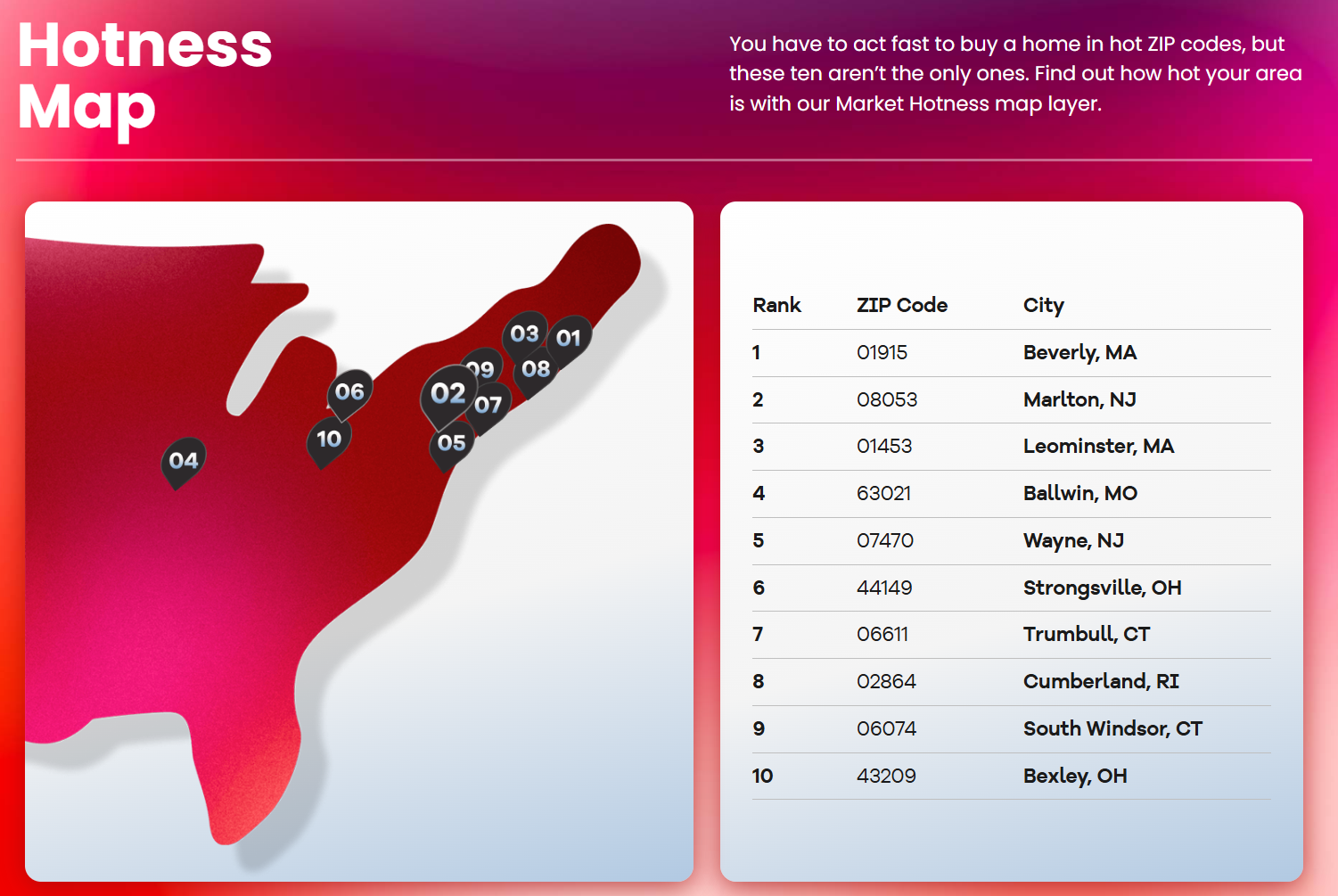

Realtor.com’s 2025 Hottest ZIP Codes report ranks Beverly, MA (01915) as the nation’s top housing market, with other hot spots including Marlton, NJ, Leominster, MA, and Ballwin, MO. Homes in these ZIPs attracted 3.6 times more views than the U.S. average and sold 30–42 days faster, despite listings being nearly 59% below pre-pandemic levels. The list is dominated by older, wealthier Northeast and Midwest suburbs, reflecting buyers’ search for relative value near major metros, while the South and West are absent for a third straight year.

Source: Realtor.com (August 2025)

“All of the top ZIPs in 2025 share a common formula of suburban environments with strong ties to major metros. These neighborhoods offer more space and greater lifestyle flexibility while maintaining commuting access. This reflects a broader shift as today’s buyers are more likely to be high-earning, and not as narrowly focused on affordability, but on a blend of amenities, space, accessibility, and value. ZIPs like 06611 (Trumbull, CT) and 06074 (South Windsor, CT) exemplify this shift, attracting urban escapees who want suburban tranquility without losing job access or infrastructure.”

Home sales

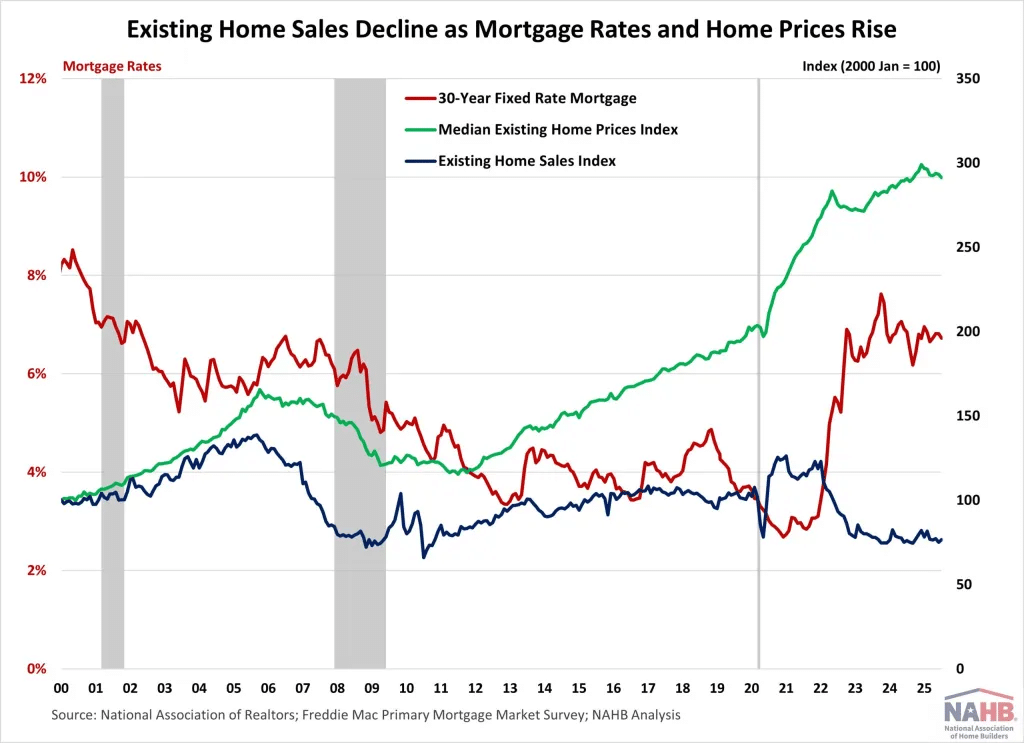

Fan-Yu Kuo of the National Association of Home Builders (NAHB) reports that existing home sales rose 2% in July to a 4.01 million annual rate, up 0.8% year-over-year, as mortgage rates eased from their May peak of 6.89% and inventory climbed to its highest level since May 2020 at 1.55 million units, a 15.7% annual increase. Despite these gains, affordability remains strained, with rates above 6% and prices increasing. The median home price hit $422,400, its 25th straight annual increase, while the first-time buyer share slipped to 28% and all-cash purchases grew to 31%.

Source: NAHB (August 2025)

Laurel Wamsley of NPR comments on rising sales, noting that we are still well below pre-pandemic levels, buoyed by increasing inventory, now at 1.55 million units. This is the highest since 2020 and up nearly 16% year-over-year. More listings are giving buyers leverage, with homes taking longer to sell and prices softening in many markets, particularly in the South and West, even as the national median price increased to $422,400. Mortgage rates, averaging 6.6%, have slipped to their lowest level since October 2024, sparking a surge in refinancing.

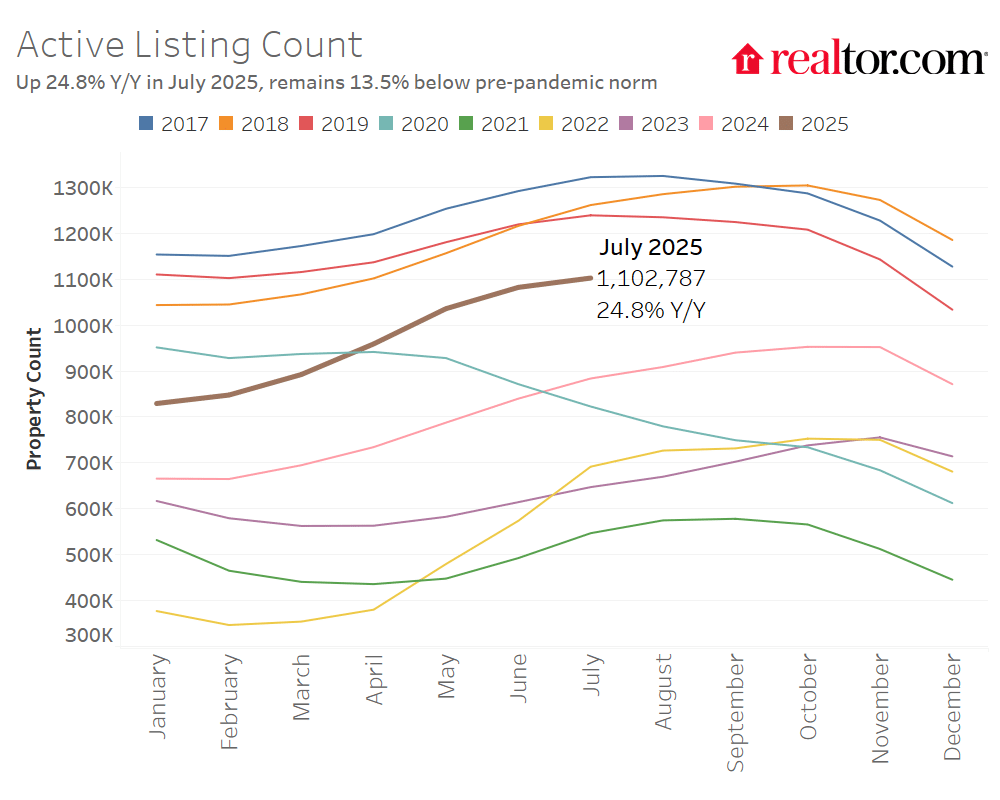

Jake Krimmel of Realtor.com reports that housing inventory also rose 24.8% year over year in July 2025, marking the 21st straight month of growth and topping 1 million active listings, though still 13.4% below pre-pandemic levels. Pending sales fell 3% while homes lingered on the market a median of 58 days, up a week from last year, pushing time on market above pre-pandemic norms. The national median list price was $439,450, up just 0.5%, while price cuts appeared on 20.6% of listings. Regional divides remain stark, with the South and West seeing the biggest slowdowns, and list prices now below 2022 peaks in 19 of the 33 major metros reporting annual declines.

Source: Realtor.com (August 2025)

“The national market is cooling overall, but the pace and severity of the slowdown vary widely across regions. On the inventory side, metros in the Northeast and Midwest remain relatively tight, while those in the South and West are tilting in a more buyer-friendly direction with longer time on the market and an increasing number of sellers cutting prices.”

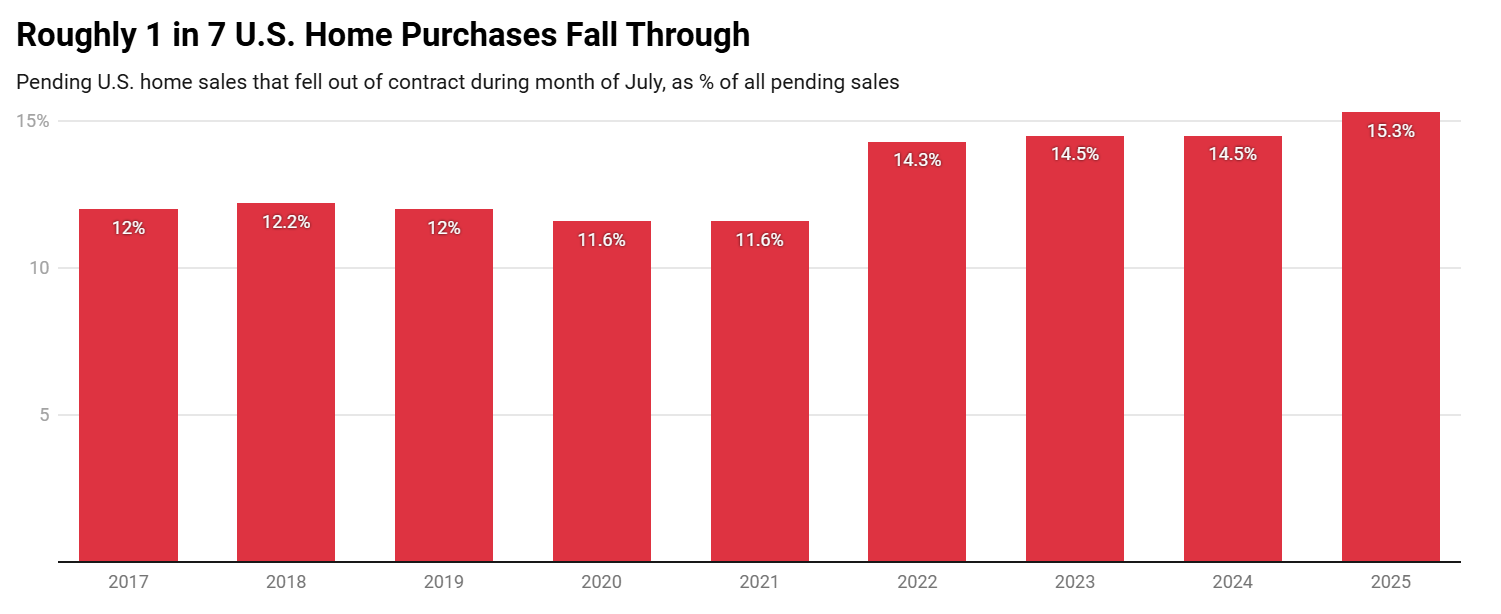

Lily Katz of Redfin reports that 15.3% of home-purchase agreements (58,000 deals) fell through in July, the highest July cancellation rate on record since 2017. Buyers, facing high prices, mortgage rates, and growing economic uncertainty, are increasingly walking away.

Source: Redfin (2025)

Cancellations are particularly pronounced in Texas and Florida, topping 20% in metros like San Antonio and Fort Lauderdale. With more inventory, buyers hold more leverage, often backing out over inspections or finding better options. However, easing mortgage rates and tightening supply could shift dynamics in the coming months.