Silicon Valley Bank (SVB) went into receivership late last week as concerns over the bank’s ability to service depositor withdrawal requests grew. The Federal Deposit Insurance Corporation (FDIC) stepped in to take over the bank and plans to sell its assets. This was the second-largest bank failure in U.S. history.

Meanwhile, various federal regulation authorities stated on Monday that uninsured deposits (the vast majority of deposits at SVB) above $250,000 would be guaranteed. Although this story is still unraveling, and another bank is now under receivership, there are some key points for the real estate industry to consider.

According to Insider.com, 15% of the loans disbursed by SVB were secured by residential mortgages and commercial real estate. The Real Deal comments on this, reporting that:

“SVB held about $8.3 billion worth of loans secured by personal residence mortgages at the end of last year, and another $138 million linked to home equity credit lines…The bank also held about $2.6 billion in commercial real estate loans. Some 35 percent of its commercial-backed loans were on multifamily properties. Office properties accounted for 21 percent.”

The Guardian and others now speculate that the Federal Reserve may slow down its planned interest rate hike, perhaps even hitting pause amid the current turmoil in the banking sector and financial markets. Paul Davidson of USA TODAY notes that, in light of the SVB failure, “Goldman Sachs, Barclays and NatWest are among research firms that are predicting the Fed will keep rates unchanged or are at least leaning toward that forecast.”

Indeed, Aarthi Swaminathan of MarketWatch reports that the collapse of SVB will likely put strong downward momentum on interest rates, boosting the cooling housing market nationwide. A material reduction in interest rates could lead to a more active spring housing market.

“While the housing markets in the West — such as in San Francisco and the Bay Area — are struggling with home prices, the bank failures aren’t going to lead to a meltdown in housing, such as in 2008, experts said. Back then, the recession was sparked by subprime lending and a foreclosure crisis.”

Fannie Mae

Fannie Mae last week released its Home Purchase Sentiment Index (HPSI), highlighting an ongoing decrease in sentiment among homebuyers, particularly as it relates to job security. The index decreased by 3.6 points in February to 58, breaking a 3-month streak of increases.

Source: Fannie Mae (March 2023)

“The percentage of respondents who say mortgage rates will go down in the next 12 months increased from 13% to 15%, while the percentage who expect mortgage rates to go up increased from 52% to 55%.”

Michael Bates of MortgageOrb reports on Fannie Mae’s report, highlighting that consumer confidence is at record lows due to sticky home prices and high interest rates. Bates quotes Doug Duncan, Fannie Mae’s chief economist, as commenting that the sentiment is felt by both buyers and sellers:

“With home-selling sentiment now lower than it was pre-pandemic – and homebuying sentiment remaining near its all-time low – consumers on both sides of the transaction appear to be feeling cautious about the housing market.”

Brooklee Han of HousingWire reports that Fannie Mae is rumored to be looking closer at giving a waiver on title insurance for certain lenders. Fannie Mae “is looking at piloting a program that would bypass traditional title insurance and AOLs [attorney opinion letters] all together. The program would grant certain mortgage lenders a waiver on title insurance requirements for loans sold to Fannie Mae and will be rolled out this spring.”

Also of note, the FDIC has now named the former head of Fannie Mae, Tim Mayopoulos, as CEO of SVB.

Zoning update

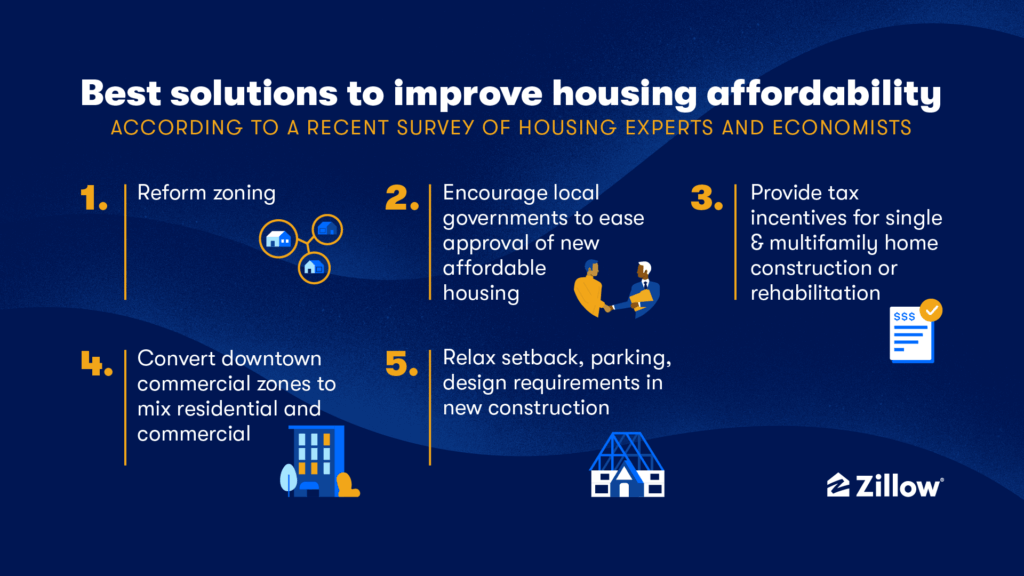

Zillow released an expert panel report last week on affordability, where an overwhelming number of economists and housing experts agree that zoning reform is one of the best pathways to affordability. In short, local jurisdictions should streamline and ease the approval process for new housing.

“Relaxing zoning rules is one of the best ways to address the nation’s ongoing housing affordability crisis, according to an independent panel of economists and housing experts polled in Zillow’s Home Price Expectations (ZHPE) Survey. Zoning reform, which would allow more housing within existing neighborhoods and growing communities, was ranked as one of the most effective means to address affordability by 73% of those surveyed.”

Source: Zillow (March 2023)

Nolan Gray of Bloomberg’s City Labs recently reported on the growing popularity of YIMBYism (Yes In My Backyard) whereby local jurisdictions relax zoning restrictions to encourage development. In Arizona, for instance, Senate Bill 1117 seeks to scrap minimum parking requirements, ease mandatory setbacks, and legalize accessory dwelling units, duplexes, and triplexes.

The signs of a latent YIMBY renaissance were there before the pandemic: Back in 2019, Utah passed SB 34, requiring that local governments adopt at least three policies from a long list of zoning reforms, including legalizing single-room occupancies (SROs) and reducing impact fees. And neighboring West Coast states like California and Oregon had already marked milestones like legalizing accessory dwelling units (ADUs) and abolishing single-family zoning.

Further, the Center of New Urbanism (CNU) recently reported on Vermont, where the state provided 41 municipalities across the state a Bylaw Modernization Grant (BMG), a one-time payment of $500,000 to “update zoning for needed homes in great neighborhoods.”