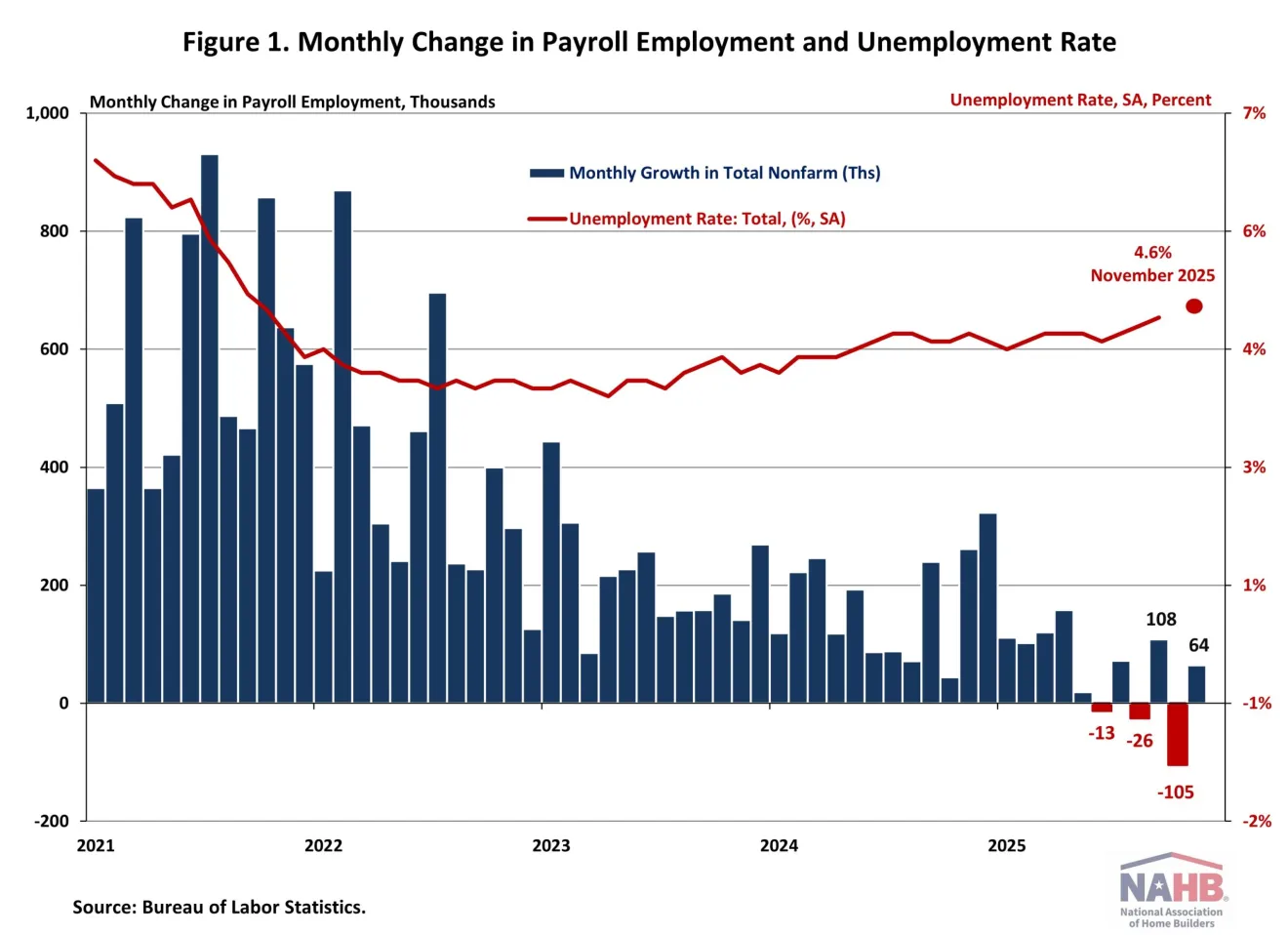

Jing Fu of the National Association of Home Builders (NAHB) reports that the U.S. labor market cooled in November 2025, with nonfarm payrolls rising just 64,000 (down from September’s revised 108,000) and the unemployment rate climbing to 4.6%, the highest in four years (since September 2021). Wage growth slowed to 3.5% year over year, down 0.6 percentage points from a year ago, though it has still outpaced inflation for nearly two years.

Source: NAHB (December 2025)

Prior months were revised lower (August from -4,000 to -26,000 and September from +119,000 to +108,000), resulting in a combined 33,000 job cuts from earlier estimates. Through November, average monthly job growth in 2025 is 11,000, far below 2024’s 168,000 monthly average; meanwhile, the number of unemployed rose by 228,000 since September, the labor force participation rate held at 62.4% (vs. 63.3% pre-pandemic), and prime-age participation ticked up to 83.8%, the highest since September 2024.

Robert Dietz, also of NAHB, reports that construction hiring demand was essentially steady in October: the number of open construction jobs dipped from 231,000 in September to 213,000, a reasonably stable level compared to a year ago (249,000) but notably lower than two years ago, as housing and broader construction activity cooled. Economy-wide job openings were also flat, edging from 7.66 million to 7.67 million, roughly in line with last year (7.62 million). Dietz notes that prior NAHB analysis suggested sustained openings below 8 million could give the Fed room to keep cutting rates, and openings remain below that threshold.

Hannah Jones of Realtor.com reports that Freddie Mac’s 30-year fixed mortgage rate was essentially flat this week, dipping 1 bp to 6.21%, as markets digested a delayed November jobs report showing a cooler labor market with unemployment up 0.2 points to 4.6% (highest since September 2021) but mainly in line with expectations. A softer inflation print also helped the outlook: headline CPI cooled to 2.7% in November, beating expectations, which could ease pressure on mortgage rates and influence the Fed’s following rate-cut decisions.

Yun Li of CNBC reports that New York Fed President John Williams said November’s CPI likely read artificially low due to “technical/practical factors” tied to missing October data collection and limited early-November sampling, which he estimates may have shaved about 0.1 percentage point off the headline print; the delayed BLS report showed CPI at 2.7% annualized versus 3.1% expected (Dow Jones), with Williams pointing to potential distortions from heavy late-November discounting and complications in rent categories, while noting some unaffected categories still look consistent with a broader disinflation trend.

Sean Conlon, also of CNBC, reports that economists are treating the delayed November CPI with skepticism: the BLS showed headline inflation at 2.7% and core CPI at 2.6%, both well below expectations (3.1% and 3.0%, respectively), but the data were complicated by an 8-day delay from the government shutdown and the cancellation of October CPI, forcing the BLS to make unclear methodological assumptions. Analysts, including Morgan Stanley’s Michael Gapen and others, argue the report may be “noisy,” possibly reflecting prices being carried forward as 0% inflation in some categories, with particular concern around owners’ equivalent rent (OER). Some economists argue that OER may have been effectively set to zero in parts of the calculation, creating a downward bias and increasing the likelihood of a rebound as the data normalizes.

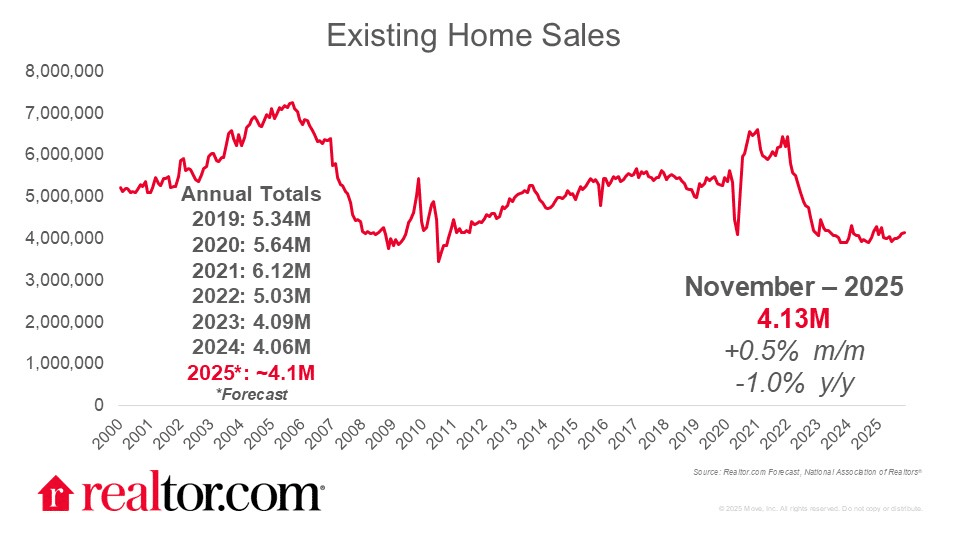

Existing home sales

Danielle Hale of Realtor.com reports that existing-home sales rose 0.5% to 4.13M in November 2025. However, they were down 1.0% year over year, as buyers benefited from mortgage rates that finally eased after staying above 6.5% until mid-September. Price growth cooled, with the median sales price up 1.2% to $409,200 (the slowest pace since mid-2023). Meanwhile, supply tightened modestly to 4.2 months, as inventory slipped to 1.43 million (from 1.52 million in October). Yet, inventory remained 7.5% higher than a year ago, indicating a more balanced market than in 2022.

Source: Realtor.com (December 2025)

Regionally, the Midwest was weakest (-2.0% m/m, -3.0% y/y) but had the fastest price gains (+5.8%), while the Northeast and South saw stronger sales (+4.1% and +1.1% m/m) with modest price increases, and the West was flat on sales with prices down 0.9%.

Diana Olick of CNBC emphasizes how who is buying (and who isn’t) is shaping the market: the median price ($409,200, +1.2% y/y) is being buoyed by stronger activity at the top end, while sales of more affordable homes ($100K–$250K) were down nearly 8% from a year ago and $1M+ homes were up 1.4%. She also notes a seasonal, but stronger-than-usual wave of delistings, as homeowners, sitting on historically low distressed sales and record housing wealth, “are in no rush” to list in winter. This leaves first-time buyers stuck at 30% of sales (vs. ~40% historically), even as wage growth outpaces price gains, and pushes investors’ share up to 18% (from 13%).

Lawrence Yun, Chief Economist of the National Association of Realtors (NAR), comments on the data:

“Existing-home sales increased for the third straight month due to lower mortgage rates this autumn…However, inventory growth is beginning to stall. With distressed property sales at historic lows and housing wealth at an all-time high, homeowners are in no rush to list their properties during the winter months. Wage growth is outpacing home price gains, which improves housing affordability. Still, future affordability could be hampered if housing supply fails to keep pace with demand.”

Dana Anderson of Redfin reports that housing demand weakened sharply heading into mid-December, with pending home sales down 5.8% year over year in the four weeks ending December 14, 2025 (the biggest drop since early 2025) and declines in 44 of the 50 largest metros, led by San Jose (-35.1%), Houston (-20.9%), and Oakland (-17.6%). Homes are also moving more slowly, taking 52 days to go under contract (about a week longer than last year), as buyers balk at mortgage rates above 6% and rising prices amid economic and job-security uncertainty (and tougher comps versus a post-election bump last year).

Housing for the 21st Century Act

The Bipartisan Policy Center reported that the House Financial Services Committee advanced the bipartisan Housing for the 21st Century Act on December 17, 2025, passing it out of committee 50–1 in its first comprehensive bipartisan housing markup in nearly a decade; the package folds in elements of 48 previously introduced bills (31 with bipartisan sponsors) and mixes supply- and affordability-focused reforms. These include:

- HUD best-practice zoning frameworks

- Grants for “pattern book” pre-reviewed designs (with 10%+ reserved for rural areas and a five-year adoption window)

- Streamlined NEPA reviews

- Updated FHA multifamily loan limits

- Reforms to HOME and CDBG (including new reporting on restrictive land-use rules)

- Rural program improvements

- Inspection reciprocity for voucher units

- Manufactured-housing changes (including eliminating the permanent chassis requirement)

- An FHA small-dollar mortgage pilot for loans under $100,000

- Raising the bank public-welfare investment cap from 15% to 20%,

- Added consumer protections/oversight (e.g., eviction helpline, annual HUD secretary testimony, stronger PHA accountability)

That said, Congress must still reconcile it with the Senate’s ROAD to Housing Act of 2025, which cleared the Senate Banking Committee unanimously on July 29, 2025.

Flávia Furlan Nunes of HousingWire reports that the bipartisan Housing for the 21st Century Act cleared the committee after a markup, positioning it for a potential House floor vote in early 2026. Additionally, lawmakers approved a separate measure extending the National Flood Insurance Program through September 30, 2026.

NAR sent a letter to the Committee in support of the new policies, noting:

“The Housing for the 21st Century Act takes meaningful steps to expand housing supply and improve affordability through smart, bipartisan reforms. By modernizing outdated federal programs, streamlining unnecessary regulatory barriers, and expanding financing options for manufactured and affordable housing, this legislation addresses real obstacles our members see every day. We appreciate Chairman Hill and Ranking Member Waters’ leadership on these critical issues and look forward to working with Congress to advance solutions that help more families achieve homeownership,”

Julie Strupp of Multifamily Dive comments that this is coalition-building: the House’s Housing for the 21st Century Act is being co-led by a high-profile bipartisan team (French Hill and Maxine Waters, plus Mike Flood and Emanuel Cleaver) and won backing from 12 major housing groups in a Dec. 16 letter praising provisions that streamline inspections, encourage faster state/local permitting, and raise FHA multifamily loan limits. Strupp also flags a related committee fight: a vote on the Respect State Housing Laws Act, which would repeal the CARES Act requirement that certain federally supported landlords provide 30 days’ notice before initiating eviction for nonpayment.

Finally, Keith Griffith of Realtor.com writes that House Republicans, after stripping the Senate’s ROAD to Housing Act from the National Defense Authorization Act in favor of a stand-alone approach, are now moving a more streamlined House package while still aiming to cut red tape and speed production. Supporters argue that the bill would help builders navigate today’s patchwork of local rules and highlight that major trade groups are applauding the committee action. This includes the NAHB pointing to reduced regulatory burdens and fewer duplicative NEPA reviews, and the MBA citing improvements such as stronger federal coordination and rural program upgrades.