Flávia Furlan Nunes of HousingWire reports that the Senate passed the 21st Century ROAD to Housing Act in an 89-10 vote, sending the most comprehensive federal housing package in over a decade to the House. The bill combines H.R. 6644 with S. 2651, spanning at least 26 sections from prior bipartisan bills. While industry groups praised provisions to boost supply and expand small-dollar mortgage lending, the Mortgage Bankers Association’s (MBA) Bob Broeksmit warned that restrictions on institutional investment would limit financing for build-to-rent communities, and the NMHC and NAA called the BTR disposition requirement “plainly not feasible.”

Indeed, Bob Broeksmit of the MBA issued a statement on the Senate’s passage of the 21st Century ROAD to Housing Act, noting that while the bill includes positive provisions on supply and small-dollar lending, the MBA has “significant concerns” with restrictions on institutional investment that would limit build-to-rent financing and FHA multifamily provisions that would reduce loan limits. He urged leaders to address these before the legislation advances, stating the goal should be “more housing, not less.”

Neil Pierson, also of HousingWire, reports that President Trump signed two executive orders targeting housing supply and mortgage credit. The first directs HUD and FHFA to review permitting and construction regulations, with HUD given 60 days to develop best practices for streamlined permitting and scaled-back green energy requirements. The second directs the CFPB to expand the qualified mortgage definition, broaden safe harbors for portfolio loans, and exempt small-balance mortgages from QM points-and-fees caps, while banking regulators are to tailor capital requirements and expand AI-driven automated valuation models.

Bob Broeksmit of the MBA released a second statement praising Trump’s housing executive orders, endorsing the focus on costly mortgage regulations that have limited credit access. Broeksmit emphasized that benefits should reach every consumer regardless of lender type and advocated for revising rules across banks, credit unions, and independent mortgage banks serving FHA, VA, and Rural Housing borrowers. MBA expressed strong support for reforming appraisals, easing construction regulations, and encouraging homebuilding.

John McManus of HousingWire details the operational implications of Trump’s homebuilding executive order, noting it directs the Army Corps of Engineers and EPA to review stormwater rules and Section 404 wetlands permitting, while the Council on Environmental Quality is to expand categorical exclusions under NEPA. HUD is directed to develop best practices, including capping permitting timelines, allowing by-right single-family development, and removing restrictions on manufactured housing. Industry estimates peg the regulatory burden at over $90,000 per new single-family home, though McManus cautions that the directives require agency rulemaking and face legal challenges.

Caroline Spivack of The Real Deal reports that a five-judge appellate panel in Albany unanimously struck down New York state’s 2019 source-of-income anti-discrimination law as unconstitutional, ruling it violates landlords’ Fourth Amendment rights in the context of federal Section 8 vouchers. The ruling does not directly affect city vouchers like CityFHEPS, but implications for NYC are murky: attorney Adam Leitman Bailey argues the decision applies statewide, while the AG’s office contends NYC’s separate 2008 law remains in effect. Deputy Mayor Leila Bozorg acknowledged the ruling “theoretically has an impact on local law,” and the AG’s office is considering an appeal.

Flávia Furlan Nunes of HousingWire reports that a federal judge, James Boasberg, blocked DOJ grand jury subpoenas to the Federal Reserve, ruling they appeared designed to “harass and pressure” Fed Chair Jerome Powell to lower rates or resign. The subpoenas arose from a November 2025 DOJ investigation into alleged discrepancies in Powell’s Senate testimony regarding cost overruns on the Fed’s D.C. headquarters renovation. Boasberg wrote that the government “offered no evidence whatsoever that Powell committed any crime other than displeasing the President.” U.S. Attorney Jeanine Pirro called it an “activist judge” ruling and announced an appeal.

Investors

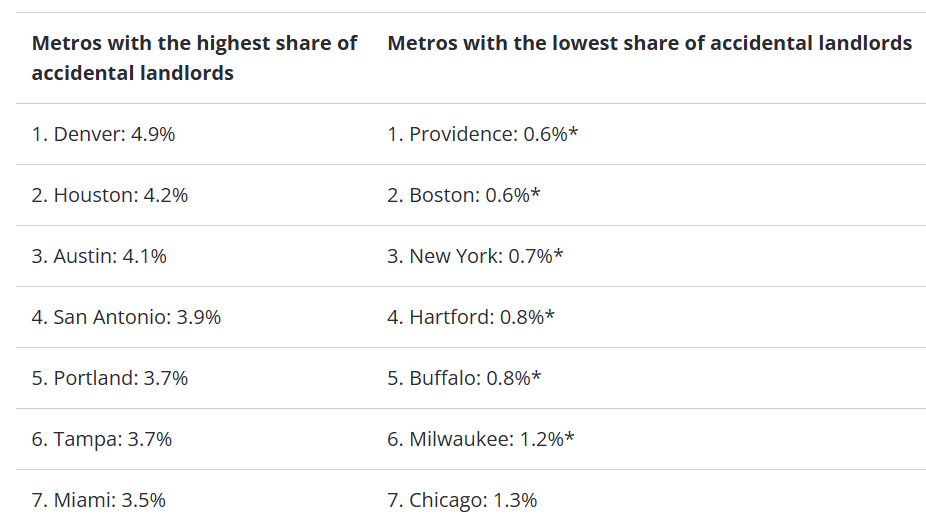

Kara Ng of Zillow reports that 2.3% of homes currently listed for rent on Zillow were previously listed for sale, putting the share of so-called “accidental landlords” at its second-highest level in nearly six years of tracking. The only time the figure was higher was November 2022, when it hit 2.4% during the rate shock that saw mortgages jump from 3.11% to 7.08% in under a year. What separates today’s trend from that moment is motivation: back then, sellers were scrambling to react to a market they didn’t see coming, while today’s pivot to renting is largely a calculated choice.

Source: Zillow (March 2026)

“The rise of would-be sellers turning into accidental landlords rather than selling for a loss — or at least a lower price than they are willing to accept — is a good indication that homeowners aren’t selling out of necessity or because they are at risk of foreclosure. Recent Zillow research found that while more than half of homes lost value over the previous year, the vast majority of homeowners are ahead on their investment. Only 3.4% of new listings were priced below their previous sale price, as of October 2025.”

Jonathan Delozier of HousingWire reported that independent local investors delivered 120,193 starter homes in 2025, outperforming builders by 217%. Just 11% of new construction fell in the starter-home price band of $261,000 or less. Investors supplied 83.75% of the new inventory below $215,000, with 72% of their purchases coming from off-market properties requiring significant repairs.

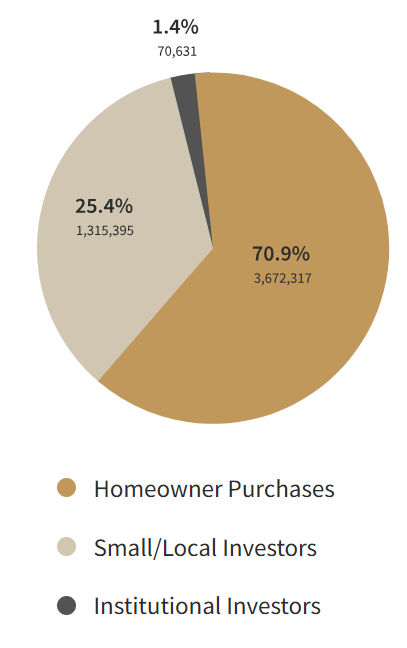

Published by New Western in partnership with the National Association for Housing Revitalization, the 2026 Flip Side Report argues that America’s housing crisis is not a unit shortage but a usable home shortage, with the U.S. carrying a 4.5 million home deficit despite 15 million vacant properties. The sub-$261,000 starter segment made up 29% of 2025 purchases but faces the sharpest affordability pressure, and contrary to popular blame, institutional investors accounted for just 1.4% of transactions. The real workhorse in that segment is small local investors, typically buying one to five properties a year, rehabilitating distressed homes that builders won’t touch.

Source: New Western (March 2026)

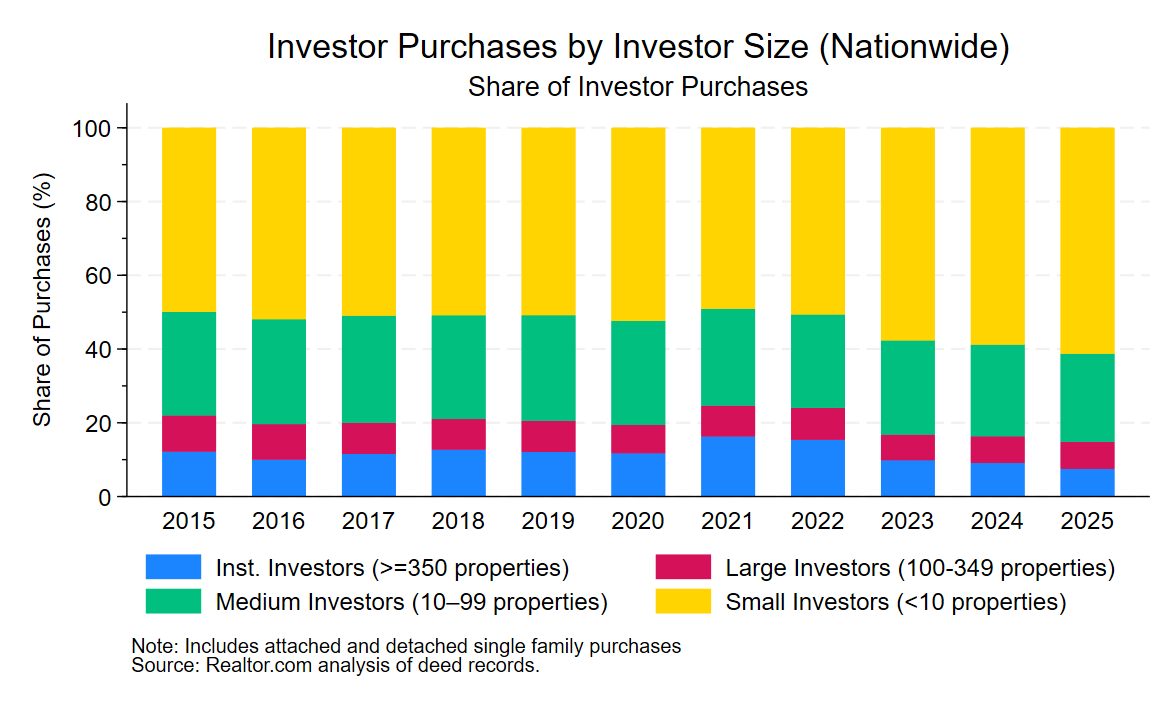

Similarly, Jake Krimmel and Hannah Jones of Realtor.com report that institutional investors, defined as those with more than 350 single-family purchases since 2015, account for just 1% of all single-family home purchases nationally, and even at their peak represented only 16% of total investor activity. Small mom-and-pop investors, those with fewer than 10 purchases, now drive over 60% of all investor transactions, up from 50% in 2021-22.

Source: Realtor.com (March 2026)

Institutional activity is geographically concentrated, with the top 25 metros accounting for 75% of purchases, yet even in Memphis, the highest-penetration market in the country, institutional buyers captured just 4.4% of sales over the past decade. The authors caution that proposed bans like the Senate-passed ROAD to Housing Act should weigh the modest near-term inventory benefit against the longer-term risk of adding new barriers to housing supply.

ATTOM Data Solutions reports that single-family rental yields declined in 54.8% of U.S. counties between 2025 and 2026, even as rents outpaced home price growth in 55% of markets. Midwestern counties led returns, with Saint Clair County, IL, posting the highest yield at 14.5%. ATTOM CEO Rob Barber noted that record-high home prices are compressing yields, pushing investors to be more selective.

Refinancing

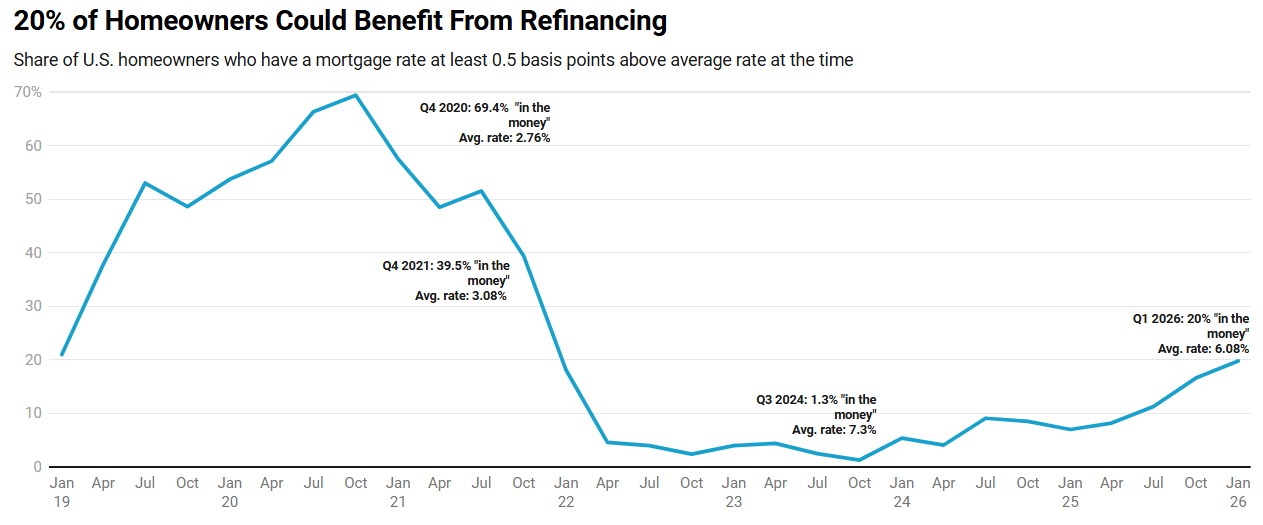

Dana Anderson and Yingqi Xu of Redfin report that nearly one in five U.S. homeowners with a mortgage, 19.8%, could now save money by refinancing, the highest share in over four years and up sharply from just 7% a year ago. The shift is driven by rates dipping to around 6.08%, the lowest in three and a half years, combined with the fact that 21.2% of borrowers are sitting on rates above 6%, the highest share in a decade.

Source: Redfin (March 2026)

To put it in dollar terms, a homeowner who bought at the 2023 peak rate of 7.8% could save roughly $500 a month by refinancing today, breaking even on a $10,000 closing cost in under two years. Despite the math, fewer than one in ten eligible homeowners have pulled the trigger.

That said, Diana Olick of CNBC notes that the 30-year fixed mortgage rate surged to 6.41%, its highest since September, driven by rising bond yields tied to the war in Iran. The move is particularly painful for the refinance window: just two weeks earlier, rates had briefly touched 5.99%, a multi-year low that had put nearly one in five homeowners in striking distance of meaningful savings. That window has largely closed, with a buyer on a $400,000 home now paying roughly $115 more per month than they would have two weeks ago.

Liezel Once of MPA reports that while nearly one in five were technically eligible to refinance this quarter per Redfin’s data, only about 9% actually did, the weakest take-up rate since early 2020. The math was compelling: a borrower who bought at the 2023 peak rate of 7.8% could have trimmed $500 a month off their payment by refinancing at 6%, breaking even on closing costs in under two years. Yet of an estimated $2.24 trillion in refinanceable mortgage debt, only $223 billion was actually refinanced in Q1. Hesitation, not opportunity, is the defining feature of this refi window.

The MBA’s weekly survey for the week ending March 6, showed total mortgage applications up 3.2%, with purchase applications jumping 7.8% week over week and sitting 11% above the same period last year. Refinance activity was more modest, up just 0.5% on the week, though still running 81% higher than a year ago, a reminder of how suppressed refi demand was when rates were peaking in early 2025.

Mike Fratantoni, MBA’s SVP and Chief Economist, comments:

“Financial markets were volatile last week amid the ongoing turmoil in the Middle East. Mortgage rates increased on net over the week, while refinance volume was roughly flat. Borrowers in recent weeks were able to get 30-year conforming rates below 6 percent, but with the current volatility, longer-term rates have moved up, pushing up the 30-year fixed rate to 6.19 percent…Purchase activity increased last week, particularly for FHA loans, which moved up more than 11 percent. The pace of homebuying continues to track ahead of last year’s pace, with overall purchase volume up 10 percent. More inventory on the market is supporting more transactions.”