Sarah Wheeler of HousingWire reports that President Trump has nominated Kevin Warsh to replace Jerome Powell as chair of the Federal Reserve, setting up what could be a contentious confirmation process. Warsh’s path may be complicated by the broader political backdrop, including a Justice Department investigation involving Powell, which adds tension to an already sensitive leadership transition at the central bank. The nomination signals a potential shift in tone and direction at the Fed, but the outcome will depend on Senate approval and how markets interpret the political pressure surrounding the institution’s independence.

Sydney Ember and Colby Smith of the New York Times report that Warsh faces the delicate task of steering the central bank through political pressure for ultra-low interest rates while preserving its independence. Warsh reportedly has a pattern of stepping into tense environments that require calm negotiation, suggesting those same skills will now be tested on a far bigger stage as he seeks to balance economic stewardship with White House expectations.

Jake Krimmel of Realtor.com argues that Warsh’s nomination could create more uncertainty than relief for housing, even if he favors rate cuts. Because mortgage rates track long-term Treasury yields rather than the Fed’s short-term policy rate, a more politicized environment and a divided Federal Open Market Committee may lead investors to demand higher yields to compensate for murkier policy signals. That dynamic can push up the 10-year Treasury yield (and therefore mortgage rates) even during a cutting cycle, muting any direct benefit to homebuyers. Krimmel’s core point is that housing affordability depends less on quick rate cuts and more on the Fed maintaining credibility, keeping inflation low and stable, and fostering solid job growth.

The Mortgage Bankers Association’s (MBA) President and CEO Bob Broeksmit, comments:

“MBA congratulates Kevin Warsh on his nomination to serve as Chairman of the Federal Reserve. His prior service on the Federal Reserve Board, where he developed a reputation as a prudent, thoughtful voice on monetary policy, paired with his private sector experience, will be invaluable as he leads the Federal Reserve in what has become an increasingly challenging and complicated mission…A balanced regulatory approach and a safe, resilient bank capital framework are essential to a healthy banking system that supports economic growth, job creation, and access to credit for consumers and businesses. MBA will continue pressing for targeted regulatory improvements.”

Sam Sutton of Politico reports that economists view Warsh as a potentially more forward-looking and quicker-acting leader for the Fed. While Warsh has at times aligned with President Donald Trump’s desire for lower borrowing costs, economists suggest he is not reflexively pro-stimulus; he has previously criticized excessive market interventions and an oversized Fed balance sheet. Warsh’s biggest shift could be a stronger, forward-looking strategic framework for policy, moving the Fed away from a heavy reliance on backward-looking data.

Jason Ma of Fortune writes that Warsh’s nomination may disappoint the White House’s hopes for rapid rate cuts, because the chair is only one vote on a divided Federal Open Market Committee and could be overruled if economic data stay firm. Analysts from firms like JPMorgan and Capital Economics warn Warsh may struggle to win over skeptical colleagues, especially if inflation remains elevated and unemployment is low, potentially leaving him caught between White House pressure and internal resistance.

Rents

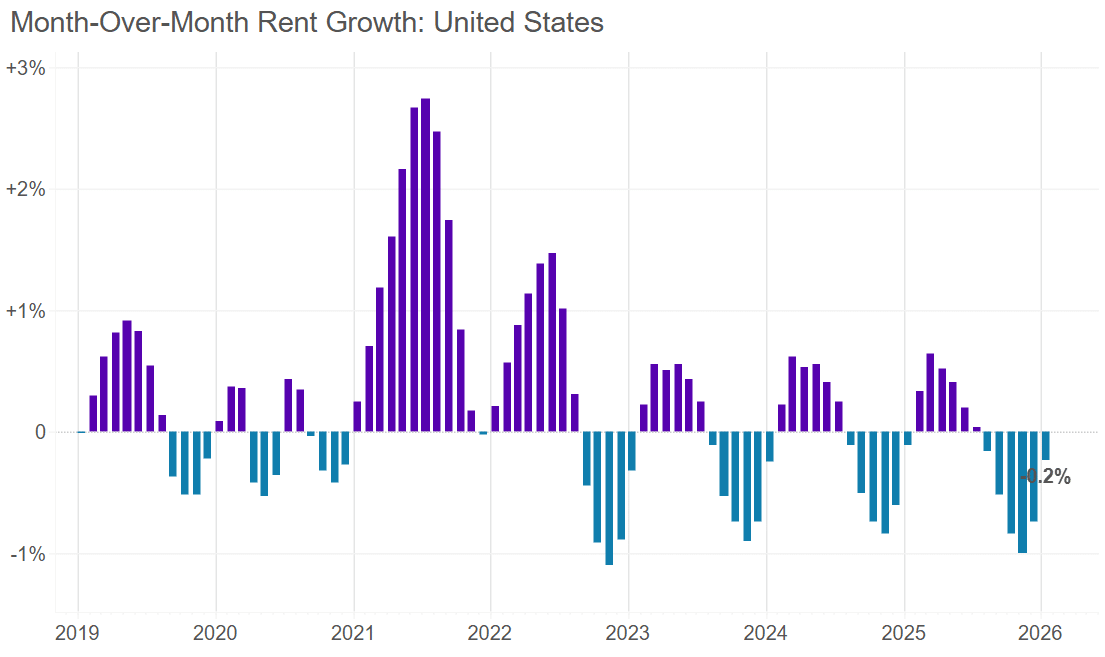

Apartment List reports that the national rental market remains in a cooling phase, with the median rent slipping 0.2% in January to $1,353 (the sixth straight monthly decline) and down 1.4% year over year, leaving rents 6.2% below their 2022 peak. A record-high multifamily vacancy rate of 7.3%, driven by the tail end of a construction boom colliding with soft demand, is keeping pressure on landlords, while units now take an average of 41 days to lease, another record. Seasonal slowdowns have grown more pronounced and shifted earlier in the year, and although modest spring tightening may return, the market is still digesting excess supply.

Source: Apartment List (February 2026)

Conditions vary widely by metro: Austin remains one of the softest large markets with rents down 6.3% annually, while Virginia Beach leads in rent growth at +5%, underscoring a nationally soft but locally uneven rental landscape.

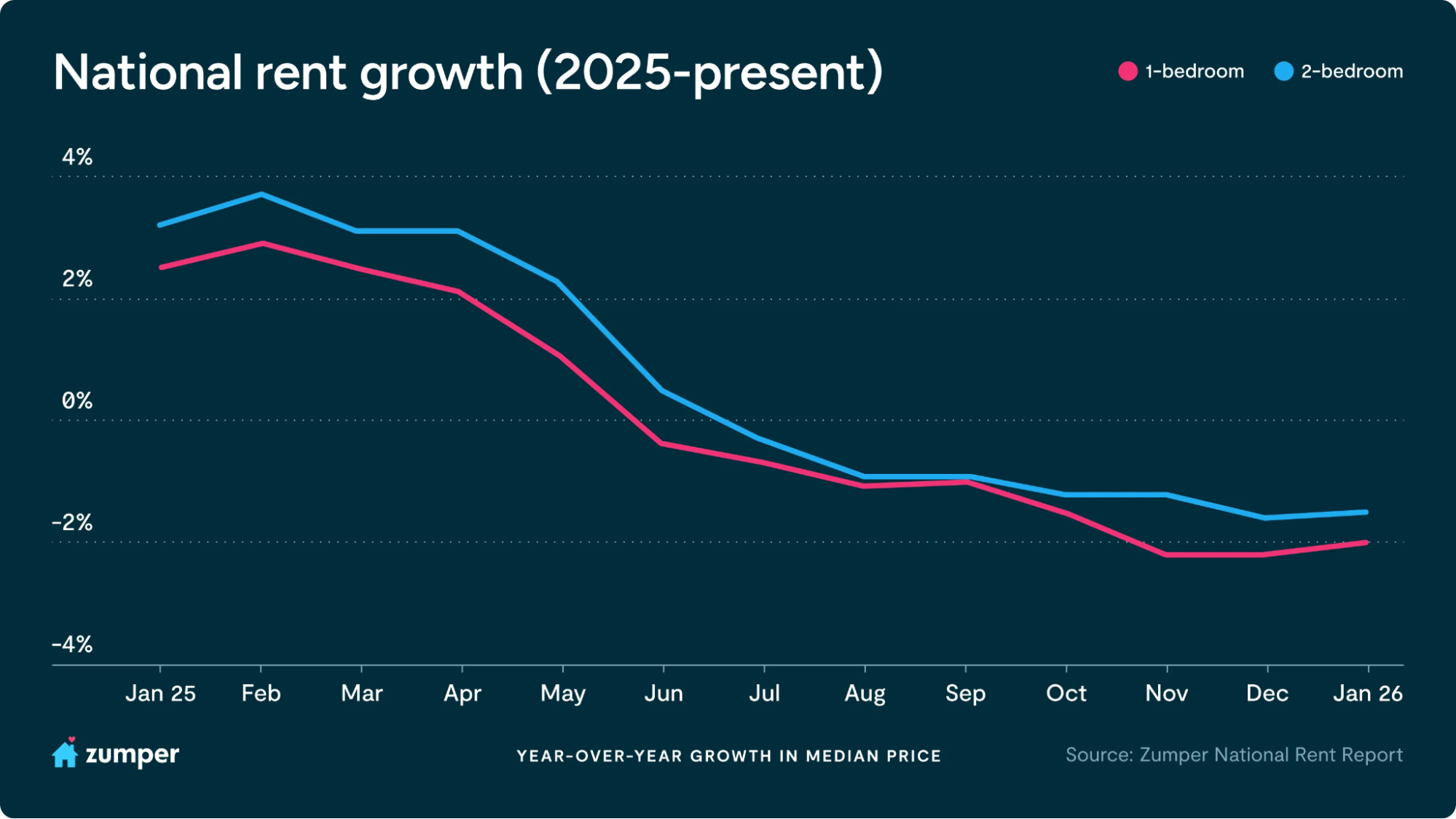

Crystal Chen and Quentin Proctor of Zumper report that the national rental market has been soft, with one-bedroom rents dipping 0.1% month over month to $1,503 and two-bedroom rents edging up 0.2% to $1,879, while both remain down year over year. Despite this broader cooling, San Francisco stands out for explosive growth, posting its fastest rent increases on record and rapidly closing the price gap with New York City, the nation’s most expensive market. In contrast, Los Angeles continues to see notable annual declines, while market rankings shift at the high end, with Washington, D.C. re-entering the top 10 and Honolulu slipping out.

Source: Zumper (February 2026)

Anthemos Georgiades, CEO of Zumper, comments:

“The U.S. rental market is largely frozen right now, caught between elevated economic uncertainty and the normal seasonal slowdown we see in the winter months…While new supply deliveries are set to ease in 2026, any rebound in rents is unlikely to be uniform. Markets that have already worked through excess inventory may see a faster snapback than what national averages suggest. The spring leasing season will offer a clearer signal of where the market is headed.”

In commenting on the above data, Diana Olick of CNBC reports that the rental market has quietly shifted from a landlord-driven cycle to a renter-negotiation cycle. With national median rent down, vacancies at a record 7.3%, and apartments sitting on the market for an average of 41 days, property owners are no longer just competing on price; they’re competing on concessions, flexibility, and lease terms. The significance isn’t just lower asking rents; it’s weaker pricing power across the multifamily sector, which squeezes operating income and slows rent-driven property appreciation, especially in once-booming Sun Belt markets like Austin, now the softest major market.

Evan Brassell of the U.S. Census Bureau reports that renters bore the brunt of recent housing cost pressures, with median monthly rent rising about $100 to $1,413 in 2020–2024 compared to the prior five-year period, while homeowner costs stayed largely flat in inflation-adjusted terms. Rents increased in 626 counties (nearly twice as many as those that fell), highlighting how affordability pressures spread widely across both urban and rural areas, though trends were uneven, with some higher-cost regions around Washington seeing localized declines even as much of the country experienced rent growth.

Local markets update

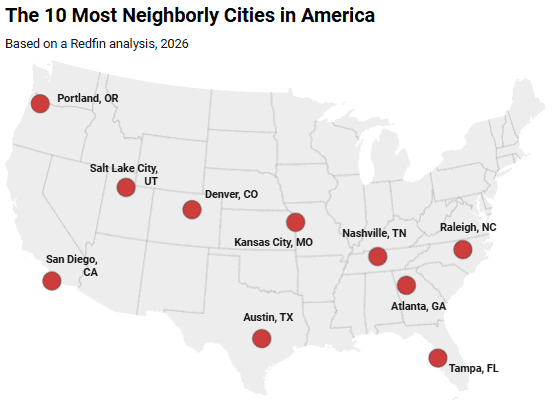

Dana Anderson of Redfin reports that Salt Lake City, Portland, and Kansas City are the most “neighborly” U.S. cities, highlighting a quality-of-life factor that goes beyond housing costs: social connection. The ranking emphasizes volunteerism, civic engagement, and how often residents help one another, suggesting that strong community ties can offset affordability pressures by improving daily well-being and neighborhood stability. While home prices vary widely (from higher-cost Western metros to more affordable Midwestern ones), the common thread is active local involvement, walkable neighborhoods, and shared public spaces that make casual interaction easier.

Source: Redfin (February 2026)

Orphe Divounguy of Zillow reports on a shift toward markets where buyers finally have negotiating power and longer-term upside, with Indianapolis topping the list, followed by Atlanta, Charlotte, Jacksonville, and Oklahoma City. Rather than simply spotlighting cheap markets, Zillow’s methodology focuses on places where prices have cooled recently but are forecast to rise, where monthly payments take up a smaller share of local incomes, and where lower competition gives buyers room to negotiate. The takeaway is that opportunity in 2026 isn’t about chasing the hottest metros, but targeting balanced markets where softer conditions today may translate into both less stress during the purchase and stronger financial gains over time.

Source: Zillow (February 2026)

ATTOM reports that while U.S. home prices hit a record median of $360,000 in 2025, gains varied sharply by market. The biggest price jumps came in Birmingham, Syracuse, Toledo, Rochester, and Dayton, while prices fell most in North Port, Deltona, Stockton, Huntsville, and Cape Coral. Investor buying remained elevated in the South and Midwest, with especially high shares in Memphis, Huntsville, Fayetteville, Birmingham, and Dallas. At the same time, profit margins shrank in most metros, with Florida markets like Tampa, Jacksonville, and Miami seeing some of the steepest drops, signaling that while prices remain high, seller windfalls are cooling in many once-booming regions.

ATTOM also reported that homeowners are holding onto their properties longer than at any point in at least 25 years, with sellers in late 2025 owning their homes for an average of 8.55 years, reflecting the continued “lock-in” effect from earlier low mortgage rates. Tenure is especially long in Massachusetts (13.29 years) and Connecticut (13.02 years), followed by California and Rhode Island, all of which are well above the national average. At the same time, all-cash purchases remain historically elevated at roughly 39% of sales nationwide, underscoring the outsized role of equity-rich owners and investors in a housing market where many typical owners are staying put rather than listing.

Joel Berner of Realtor.com reports that homeowners’ associations are becoming more common and more expensive across the U.S., with especially heavy concentrations in the West and South. Nevada has the highest share of listings with HOA fees (68.3%), while South Dakota has the lowest (12.3%). The steepest HOA cost burdens relative to mortgage payments are concentrated in Florida metros, led by Miami, Naples, Cape Coral, Port St. Lucie, and North Port, where HOA dues can consume a sizable share of monthly housing costs. Outside Florida, high HOA burdens also show up in Hilo and Minneapolis, but the overall pattern points to Sun Belt metros (especially condo-heavy coastal markets) as the epicenter of rising HOA prevalence and fees.