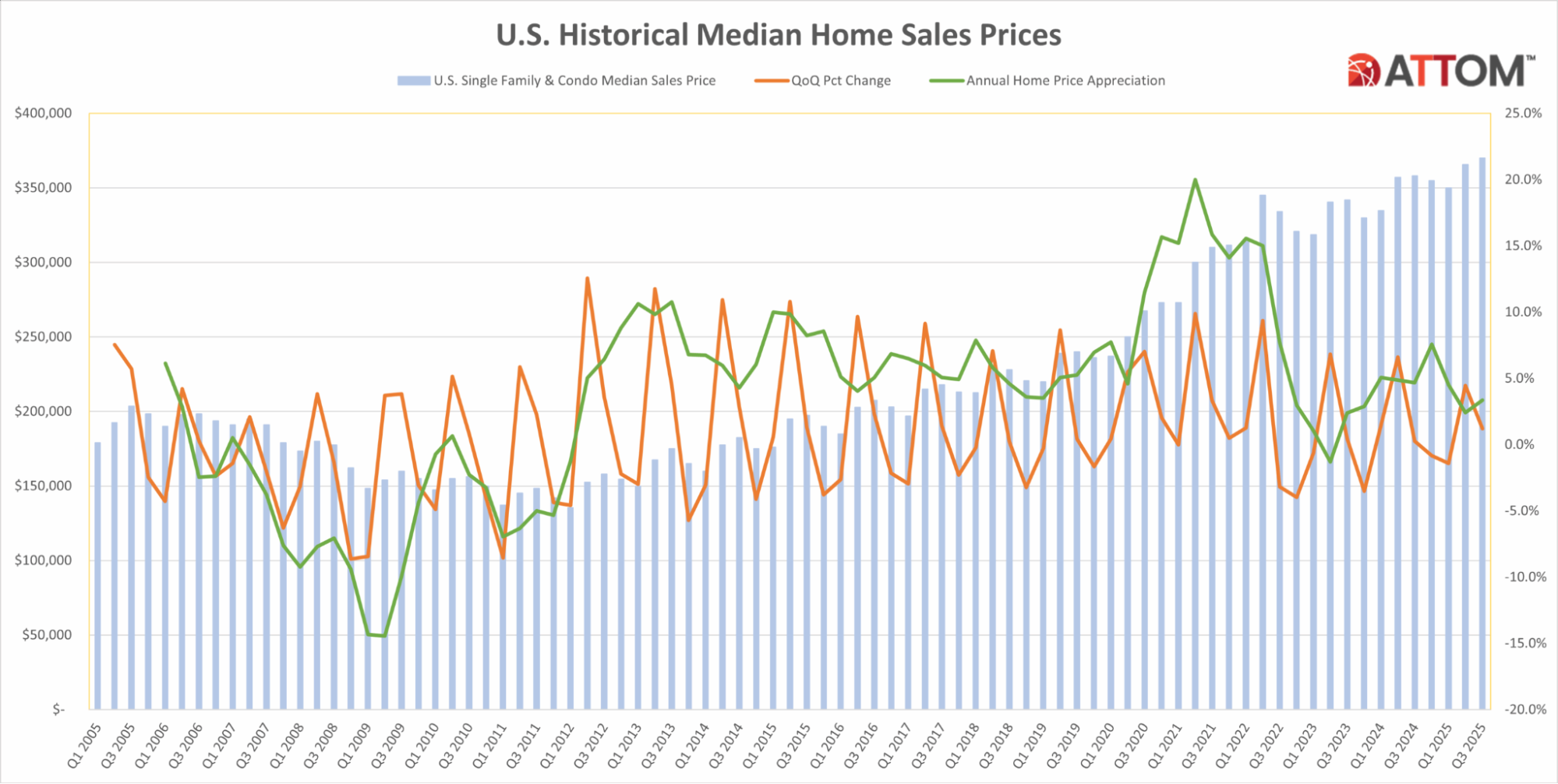

Megan Hunt reports that, according to ATTOM’s Q3 2025 U.S. Home Sales Report, homeowners earned an average profit margin of 49.9% on typical single-family and condo sales, slightly higher than Q2’s 49.3% but below the 55.4% peak in Q3 2024. The median sale price rose to $370,000, up 1.2% quarter-over-quarter and 3.4% year-over-year, while the average profit per home hit $123,100, a 1.9% quarterly increase but 3.5% lower year-over-year. Before 2020, margins hovered near 30%, spiking to over 60% by mid-2022 amid pandemic-era migration trends.

Source: ATTOM (October 2025)

Among the 157 metros analyzed, profit margins declined in 59% quarter-over-quarter and 84% year-over-year, yet ten markets stood out for major gains, led by St. George, UT (+10.9 pts), Gulfport, MS (+9.5), Augusta, GA (+5.9), Lexington, KY (+5.7), and Dayton, OH (+5.6), showing that localized strength persists despite a cooling national trend.

Rob Barber, CEO of ATTOM, comments:

“Profit margins remained steady and high throughout the traditionally busier summer selling season…While continuously rising prices could have chased away buyers and slackened demand, the recent dip in mortgage rates may be helping to keep more people in the market.”

Philippa Maister of Globe St reports that Realtor.com’s September 2025 “hottest markets” list is dominated by the Midwest and Northeast for the second straight year, with 7 of the top 20 in Wisconsin (including Kenosha, Appleton, Wausau, Racine–Mt Pleasant, Janesville–Beloit, Green Bay, and Milwaukee–Waukesha). “Hot” is defined by views per property and days on market; Springfield, MA held No. 1 for the 5th month, drawing 3.1× national views and selling about 30 days faster, with a $370,000 median list price. Wisconsin metros (mostly below the national median price) averaged 2.8× the views and sold 27 days faster.

Kara Ng of Zillow reports that apartments under $1,000 are scarce and concentrated mainly in smaller Midwest and Southern metros. Wichita, Kansas, leads with 54% of listings below $1,000, followed by McAllen, Texas, Little Rock, Arkansas, Toledo, Ohio, and Oklahoma City, Oklahoma. In contrast, Boston, Miami, and Washington, D.C. have fewer than 2% of listings at that price point. When affordability is measured by rent as a share of median income, Ogden, Utah, ranks first with 97% of apartments affordable, trailed by Raleigh, North Carolina, and Colorado Springs, Colorado. In comparison, Miami remains the least affordable with only 31% of units meeting that benchmark.

Source: Zillow (October 2025)

Builders

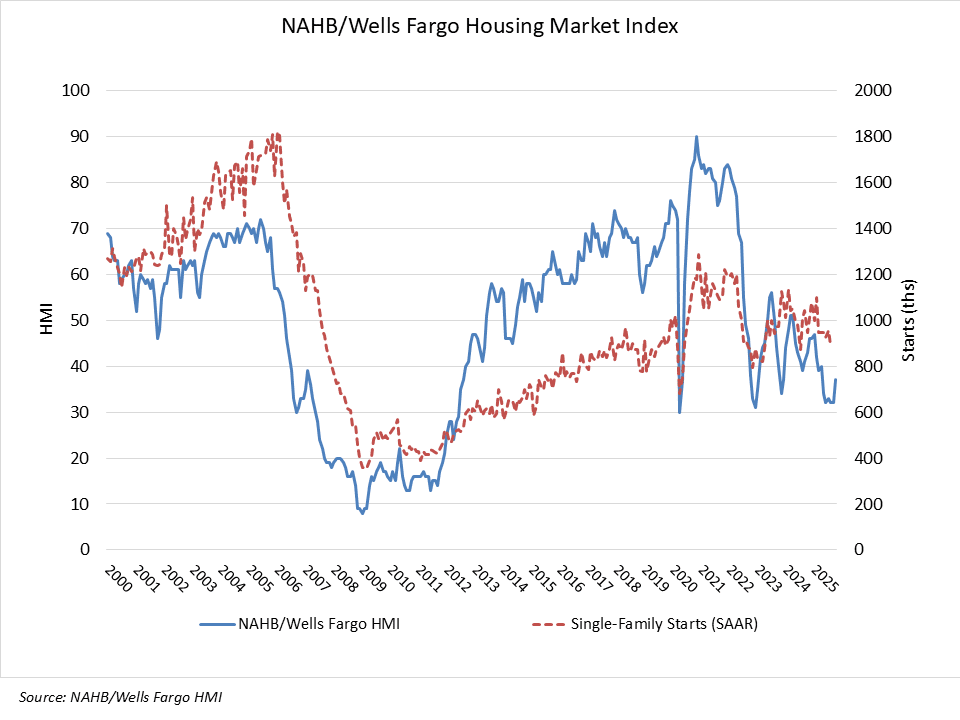

Robert Dietz of the National Association of Home Builders (NAHB) reports that builder sentiment rose sharply in October by five points to 37 (the highest level since April) as future sales expectations crossed the 50-point breakeven mark for the first time since January. The uptick signals optimism heading into 2026, supported by easing mortgage rates, which fell from just above 6.5% in early September to 6.3% in October. Despite lingering supply-side costs and cautious buyers, builders see a slightly improving sales environment, with smaller firms leaning toward remodeling and luxury segments staying strong. NAHB modeling also suggests single-family permits rose about 3% in September, indicating early signs of renewed momentum.

Source: NAHB (October 2025)

Orphe Divounguy of Zillow reports that new construction is finally catching up with renter demand, easing affordability pressures nationwide. Builders completed more multifamily units in 2024 than in any year since 1974, helping rental affordability improve to its best level in four years; now requiring 28.4% of median income. The surge in supply, especially in the South where building restrictions are looser, has driven record concessions on 37.3% of Zillow listings and slowed single-family rent growth to 3.2%, the weakest since 2016.

Danushka Nanayakkara-Skillington of NAHB reports that builders remain cautious as single-family permitting fell for the eighth consecutive month in August, reflecting persistent affordability and economic challenges. Year-to-date single-family permits totaled 637,096, down 7.1% from 685,923 in August 2024, with only the Midwest showing growth at 1%. The South and West saw the steepest drops—7.5% and 11.5%, respectively.

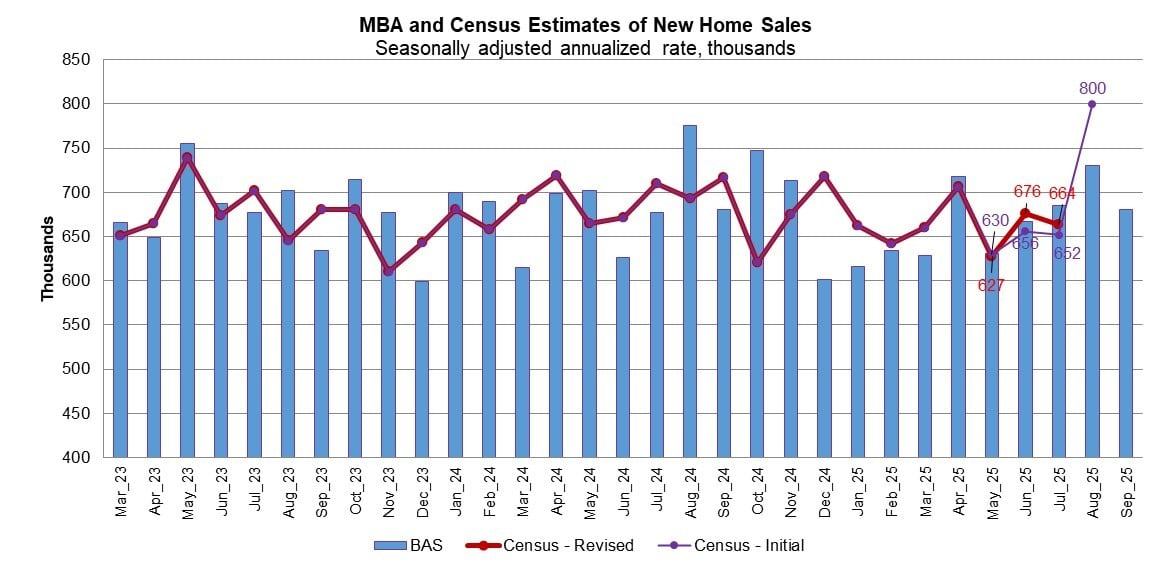

The Mortgage Bankers Association (MBA) reports that mortgage applications for new home purchases rose 2% year over year in September 2025 but fell 5% from August, reflecting typical seasonal trends. MBA estimates new single-family home sales ran at a seasonally adjusted annual rate of 680,000 units (down 6.8% from August’s 730,000) after hitting a 10-month high. Despite slightly lower mortgage rates, increased inventory, and builder incentives, near-term demand softened as the labor market weakened, signaling a modest cooling in new construction activity heading into year-end.

Source: MBA (October 2025)

“MBA’s estimate of new home sales for September showed a 7 percent decline to an annual pace of 680,000 units after reaching a 10-month high in August. Given the current delay of the U.S. Census new home sales release due to the ongoing government shutdown, MBA’s estimate provides a leading indicator of the direction of the new home sales market for September…Purchase activity for new homes continued to run ahead of last year’s pace, showing a 2 percent annual increase. Applications were down over the month, but were consistent with typical seasonal patterns for September. Despite more inventory, builder incentives, and lower mortgage rates, near-term demand is slowing as the labor market weakens.”

Luxury homes

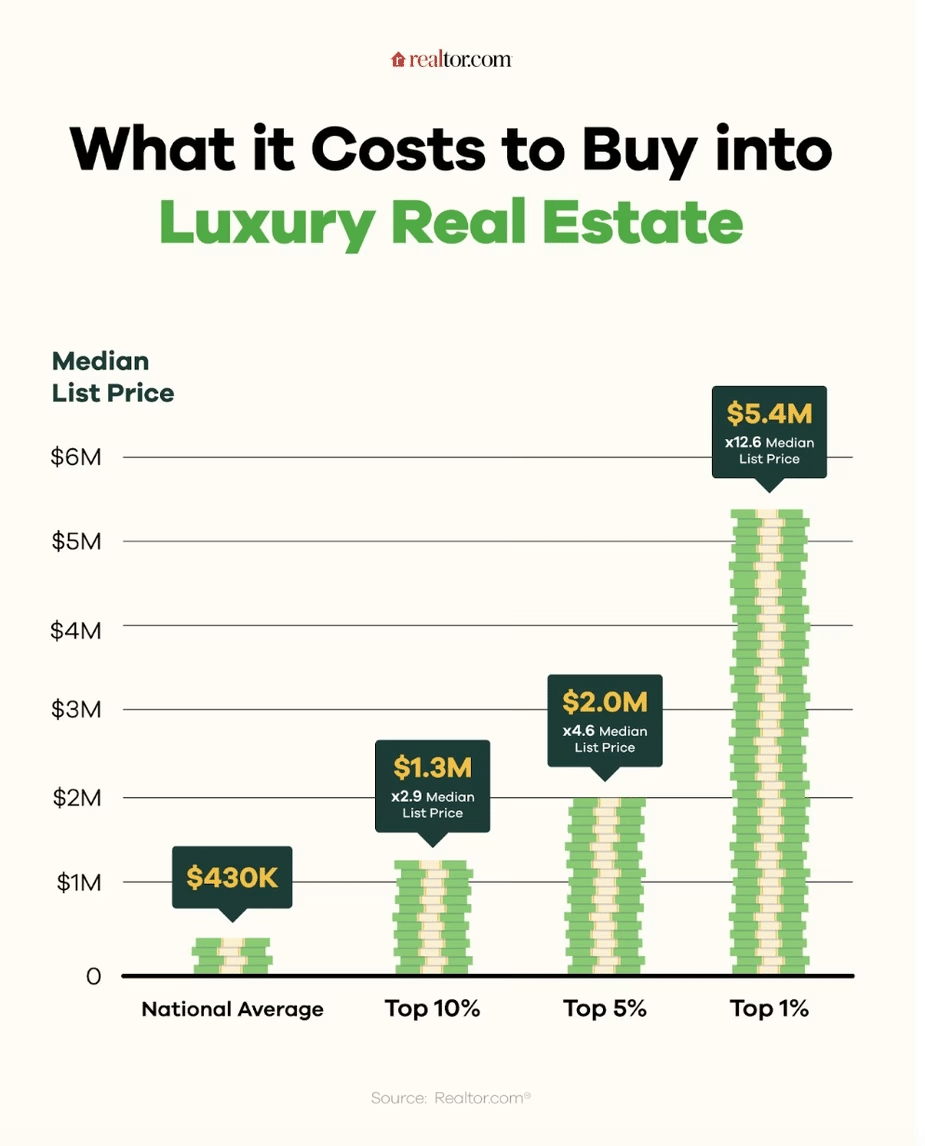

Maddie McGay of USA TODAY reports that the price threshold for luxury homes has surged more than 60% over the past decade, rising from $796,000 in 2016 to $1.3 million in 2025, according to Realtor.com’s “What Is Luxury” report. A $1 million home, once near the top 5% of listings, now falls below the luxury cutoff. Today, the top 5% of homes start at $2 million, while the top 1% begin around $5.4 million, highlighting how sharply luxury real estate prices have escalated nationwide.

Snejana Farberov of Realtor.com reports that the entry point for luxury real estate has soared to about $1.3 million in 2025, nearly triple the national median list price of $430,000. The top 5% of homes now start at $2 million, while the top 1% (the ultraluxury tier) begins near $5.5 million, or 12.6 times the median price. Experts attribute the jump to rapid home price appreciation driven by tight supply, strong demand, and inflation, surprising many buyers at how little $1 million now buys in the high-end market.

Source: Realtor.com (October 2025)

Realtor.com senior economist Anthony Smith comments:

“Before the pandemic-era demand surge and low mortgage rates put home prices on steroids, a million-dollar home was in the nationwide top 10% of homes; and back in 2016, a million-dollar price tag would have landed a home among the top just outside of the top 5%…Put simply, a million-dollar listing still means a seven-figure price tag, but today it takes closer to $1.6 million to snag a home with the same luxury status that a $1 million listing carried in 2016.”

Finally, Casey Farmer of Mansion Global reports that Manhattan’s luxury housing market defied the national slowdown in Q3 2025, with luxury co-op and condo sales rising 13.6% year over year to 318 deals (most paid in cash). Inventory dropped 16.1% from last year, tightening supply to 5.7 months and driving the median luxury price up 2.8% to just over $5.9 million. Analysts credit the surge to substantial Wall Street bonuses, record stock market highs, and mortgage rates falling to an 11-month low. Overall, Manhattan home sales also climbed 13.4% year over year to their highest level in more than two years, underscoring the city’s resilience as the rest of the U.S. luxury market cools.