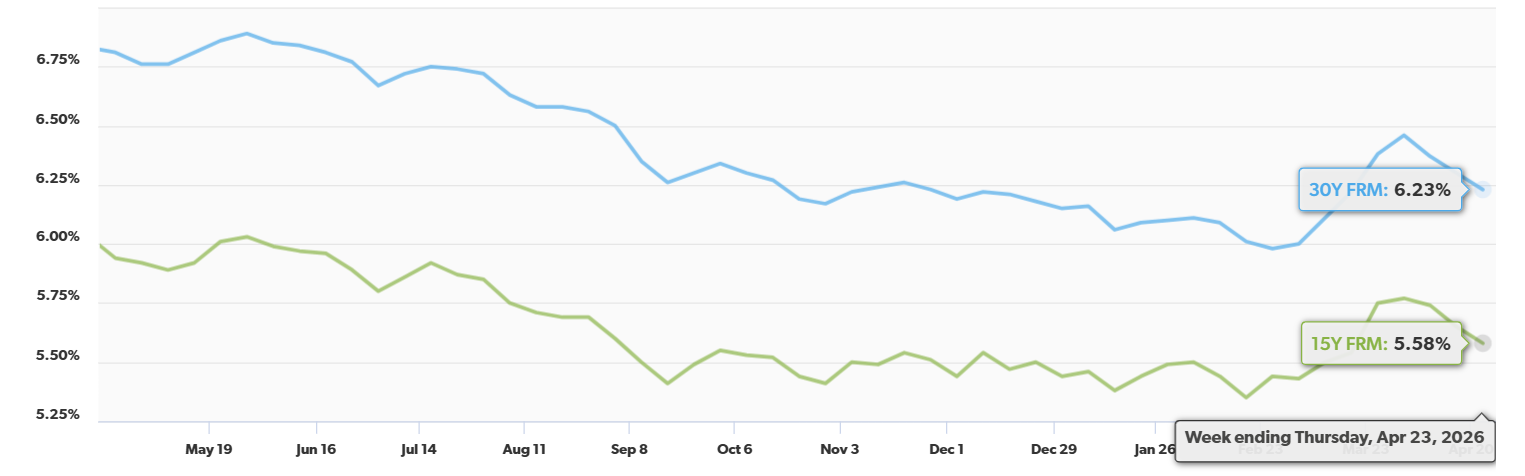

Freddie Mac reported that the 30-year fixed-rate mortgage averaged 6.23% for the week ending April 23, down from 6.30% the prior week and below the 6.81% recorded one year ago. The 15-year fixed rate fell to 5.58%, down from 5.65%. Rates now sit at their lowest level in the last three spring homebuying seasons.

Source: Freddie Mac (April 2026)

“The 30-year fixed-rate mortgage declined again this week to 6.23%. Rates currently stand at their lowest level in the last three spring homebuying seasons. This improvement, coupled with a pickup in purchase applications and refinance activity, as well as an increase in monthly pending home sales, underscores signs of improving momentum in the market.”

Prashant Gopal of Bloomberg noted that the drop marks the third consecutive week of declines, easing pressure on homebuyers as the spring selling season gets underway. Rates stood at 6.81% one year earlier, putting the current reading roughly 58 basis points below the prior spring.

Further, the Mortgage Bankers Association (MBA) reported that applications increased 7.9% on a seasonally adjusted basis for the week ending April 17. The Refinance Index rose 6% week-over-week and was 52% higher than the same week a year ago. The Purchase Index jumped 10% for the week and ran 14% above year-ago levels, led by an 11% gain in conventional purchase loans.

Mike Fratantoni, SVP and Chief Economist, MBA, comments:

“Mortgage rates declined last week as financial markets responded positively to the Middle East ceasefire and the lower trend in oil prices, with the 30-year fixed rate decreasing to 6.35%. Refinance application volume increased by 6%, while purchase application volume increased an even stronger 10% and was up 14% compared to last year’s pace. Despite the geopolitical uncertainty, housing demand is being supported by a still resilient job market, and homebuyers are experiencing a buyer’s market in most of the country given the higher levels of inventory relative to last year.”

Sarah Wolak of HousingWire tracked a parallel signal from the Xactus Mortgage Intent Index, which climbed to 146.0, up 3.99% week-over-week and 5.04% year-over-year. The index had been running below year-ago levels for four straight weeks before this reading flipped it positive. The 30-year fixed conforming rate fell to 6.35% from 6.42%, and the 15-year fixed rate dropped to 5.75% from 5.85%.

Jiayi Xu of Realtor.com found that new listings surpassed 120,000 during the week of April 16, a volume not seen in nearly a year. Active inventory climbed 4.3% year-over-year, and year-to-date totals are up 7.2%, giving buyers the widest selection of the post-pandemic era. Median listing prices were down 1.2% YoY, marking the 25th consecutive week of flat or negative price growth.

Finally, Nathan Knottingham of HousingWire argued that the industry may finally be near the bottom of the current mortgage market cycle. He points to NMLS Q3 2025 data showing that, while total licensed individuals are still down, state-specific licensing activity is rising as surviving originators add states to follow referrals and as population shifts occur. That expansion, he writes, is a vote of confidence from people putting real dollars behind where they believe demand will return.

“Mortgage is cyclical. It always has been. This industry breathes. It inhales and exhales. And eventually, after holding that breath for long enough, we all start asking the same question: When does the next inhale begin? I think we may finally be getting close. I do think we are close to the bottom of the exhale. So double down on the fundamentals, invest in your team, and the next inhale will be wind in your sails.”

Home sales

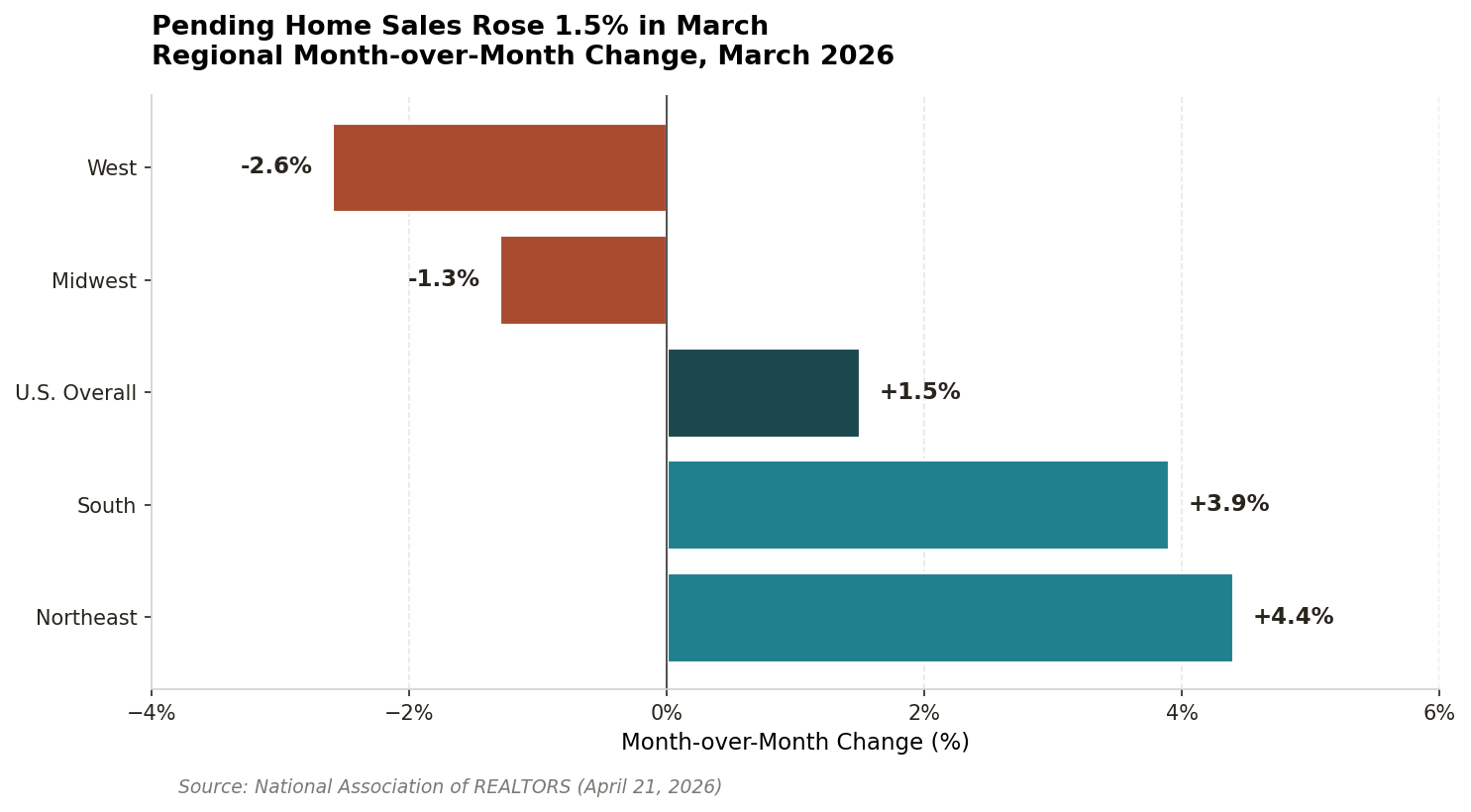

The National Association of Realtors (NAR) reported that pending home sales rose 1.5% month-over-month in March, the second consecutive monthly gain. Year-over-year, pending sales slipped 1.1%. The Northeast led all regions at +4.4% MoM, followed by the South at +3.9% MoM (and +2.3% YoY). The Midwest fell 1.3%, and the West declined 2.6% on the month.

Source: NAR (April 2026)

“Contract signings rose in March despite higher mortgage rates, pointing to pent-up housing demand. A greater supply of inventory will help translate that demand into more home sales. A good number of markets in the South experienced price cuts over the past year but recorded the strongest job growth. That combination should lead to stronger housing market activity in the South this year.”

Mark Niquette of Bloomberg noted that the reading beat the median economist forecast of a 0.5% gain, with the index climbing to a four-month high of 73.7. Improving inventory appears to be helping mitigate higher borrowing costs, and the South posted the strongest regional gains.

Further, NAR’s Existing-Home Sales report showed sales fell 3.6% month-over-month in March to a seasonally adjusted annual rate of 3.98 million, down 1.0% year-over-year. The median existing-home price reached $408,800, up 1.4% YoY and a record high for March. Inventory rose to 1.36 million units (4.1 months supply), and homes spent a median of 41 days on the market.

Julie Taylor of Realtor.com reported that NAR has sharply cut its 2026 existing-home sales forecast from +14% to +4%. The new-home sales outlook was also revised from +5% growth to flat, while the median home price forecast held at +4%. NAR lifted its 2026 average mortgage rate assumption to 6.5%, up from roughly 6%.

Lawrence Yun, Chief Economist, NAR, comments:

“Rather than a double-digit percentage increase, which I thought would occur in 2026, I think it is going to be in the low single-digit percentage gain this year. Now that the mortgage rate has increased and is likely to stay elevated at least above 6% in the upcoming months, I had to reduce the forecast outlook.”

Finally, Melissa Dittmann Tracey, also of NAR, contextualized the slowdown by noting that 18% of homes sold above list price in March and that listings received an average of 2.2 offers. All-cash buyers made up 27% of transactions, and first-time buyers accounted for 32%. Yun estimates the typical homeowner has accumulated $128,100 in housing wealth over the past six years, and he said an additional 300,000 to 500,000 homes for sale would be needed to bring supply closer to historical norms.

Rentals

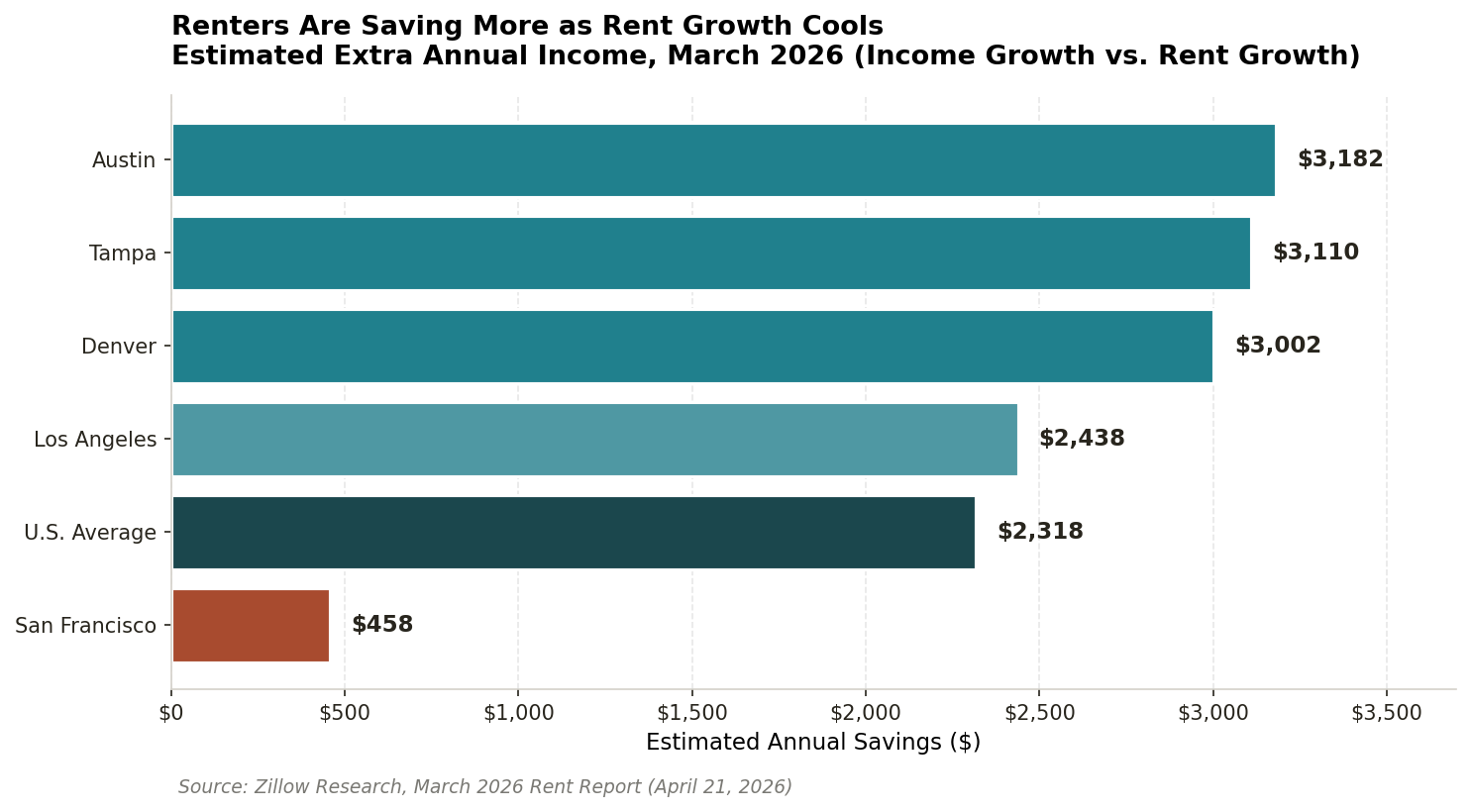

Kara Ng of Zillow Research reported that the typical U.S. asking rent reached $1,910 in March, up 1.8% year-over-year – the slowest annual growth rate since 2020. Single-family asking rents rose 2.5% YoY to $2,225, the slowest growth ever recorded in Zillow’s series, while multifamily rents climbed just 1.3% YoY to $1,757. Some 39.8% of Zillow rental listings offered concessions in March, tying 2025 for the highest share ever for the month.

Source: Zillow (April 2026)

“For the first time in years, income growth is outpacing rent increases. The typical household has an extra $2,318 a year, enough to cover months of groceries, a full year of phone and internet bills, or make meaningful progress on savings.”

That said, Zillow argued that those savings can become a down payment runway for would-be buyers. A single free month of rent can put roughly $2,000 back in a renter’s pocket, and more than half of prospective buyers have paused or delayed a home search at least once to save for a down payment. Only 48% of prospective buyers say they have saved enough today.

Further, Yahoo Finance highlighted where renters are pocketing the biggest savings: Austin leads at $3,182 per year, followed by Tampa at $3,110 and Denver at $3,002. Los Angeles renters are saving $2,438 annually, while San Francisco renters save just $458, as rents there continue to climb. Nationally, rent now eats 26.5% of median household income, approaching the pre-pandemic norm of 25.8%.

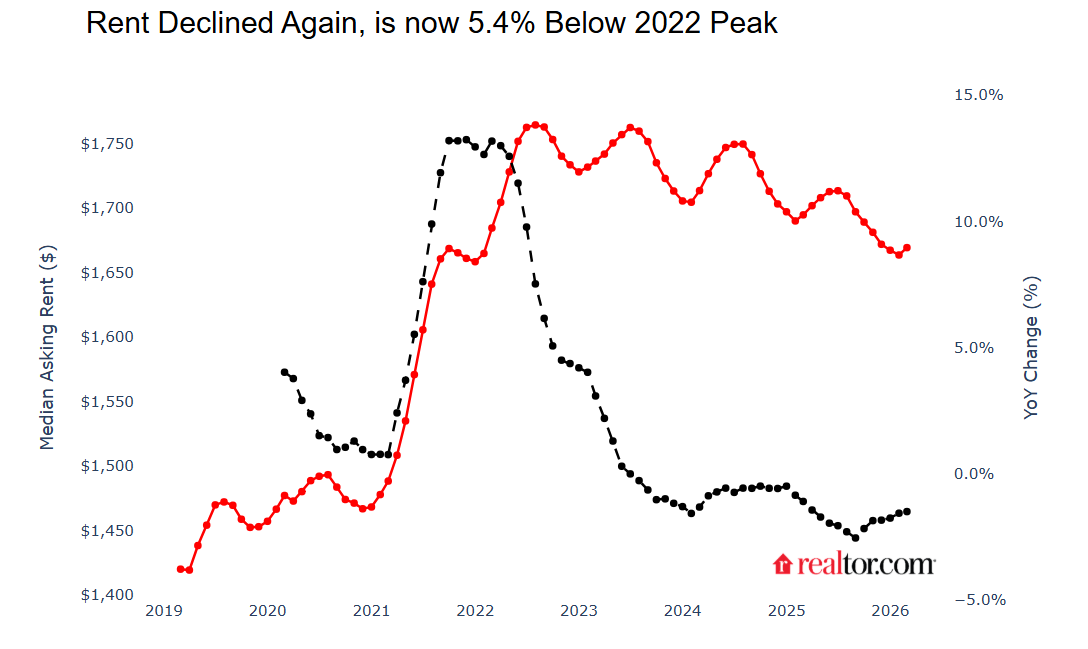

Finally, Jiayi Xu of Realtor.com Research reported that the national median asking rent across the 50 largest metros dropped to $1,669 in March, down 1.5% year-over-year and marking the 32nd consecutive month of annual decline. Two-bedroom units averaged $1,859 (-1.7%), one-bedrooms $1,563 (-1.1%), and studios $1,410 (-0.7%). Renting a starter home remains cheaper than buying in all 50 major metros, with an average monthly savings of $920 versus ownership.

Source: Realtor.com (April 2026)

“Renting is not a barrier to homeownership; it is an opportunity to build toward it. The monthly savings renters enjoy relative to buying can be put directly toward a down payment, creating a faster path to ownership and a lower monthly mortgage payment when the time comes.”