Last Updated on December 23, 2024

To calculate a loan to value (LTV) ratio, divide the current balance of the loan by the current market value of the asset securing the loan. If you own the property outright with no debt, then you don’t have an LTV at all!

Here’s the basic formula:

Debt Balance / Current Value = LTV Ratio

Why is LTV ratio one of the top metrics every investor should know?

The loan to value ratio can be used for many different purposes. Investors often use the LTV ratio when making key decisions about when to sell or refinance. A low LTV is a clear signal that a lot of equity has accumulated in a property. When this happens, investors often look to re-deploy some of that equity into new investments. They typically accomplish this one of two ways: 1) sell the asset, 2) cash-out refinance.

Lender’s often use the LTV to assess the relative strength of their position and the potential risk of a borrower default. When an LTV is low, lenders know that the borrower has a lot of equity in the deal and is less likely to walk away. As an LTV rises towards 100%, the loan is increasingly at risk of default since the borrower has less remaining equity to lose.

On the front end of an acquisition, lenders typically assess how much of the total purchase price they’re willing to finance based on a loan to value ratio. Some lenders are comfortable with higher LTVs while others are more choosy and prefer to work with borrowers who bring more skin to the table.

Example: Assume you want to buy a property for $100,000. You have $20,000 available for a down payment, so you’ll need to borrow $80,000. $80,000 (loan amount)/$100,000 (purchase price) = 0.80 (LTV). Your LTV ratio will be 80% because the dollar amount of the loan is 80% of the value of the property.

The difference between the total amount the lender will finance and the purchase price plus closing costs is the amount of cash that you will have to put into the deal. If the lender will loan up to an 80% LTV, you’ll need a 20% down payment to secure the mortgage and move forward.

The difference between the total amount the lender will finance and the purchase price plus closing costs is the amount of cash that you will have to put into the deal. If the lender will loan up to an 80% LTV, you’ll need a 20% down payment to secure the mortgage and move forward.

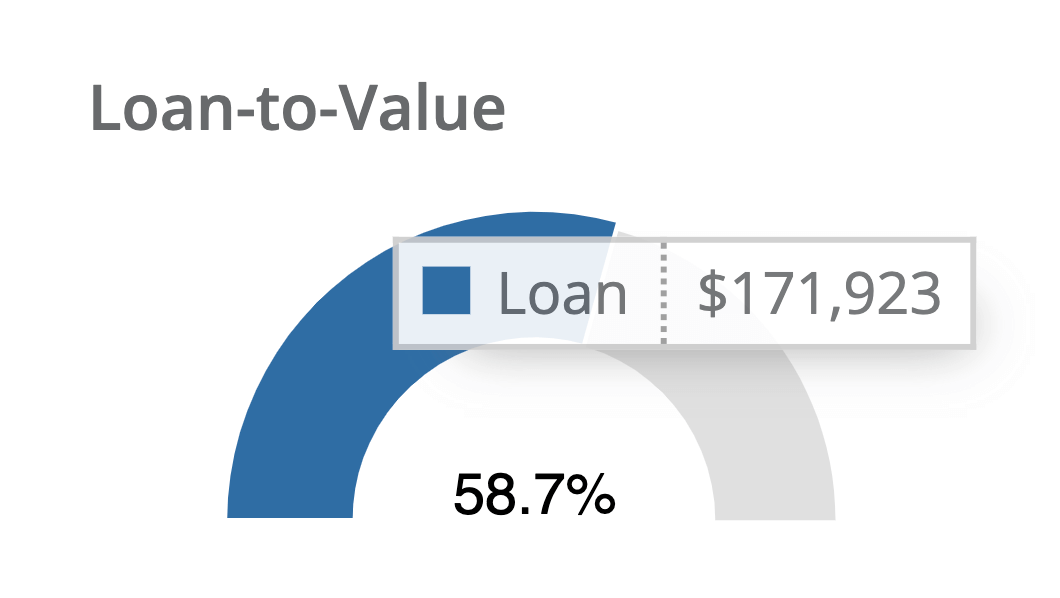

And now for a case study.

Let’s imagine Chris is a Stessa investor and owns a single-family rental house in Kansas. The property has a current market value of $292,857 and the current debt balance is $171,923. So his LTV ratio is:

$171,923 (Loan) / $292,857 (Value) = .587 or 58.7% LTV Ratio

You can calculate this metric manually, or let Stessa do it for you. Learn about other important metrics every real estate investor should know on our blog or YouTube channel.